Florida Landlord Briefing: June 2026

The SB 716 five-day eviction notice you were told to prep for? It died in committee. Citizens' insurance change still lands July 1, hurricane season just opened, and mortgage rates climbed again. Four June developments — one of them a myth to ignore.

Florida Landlord Briefing: June 2026

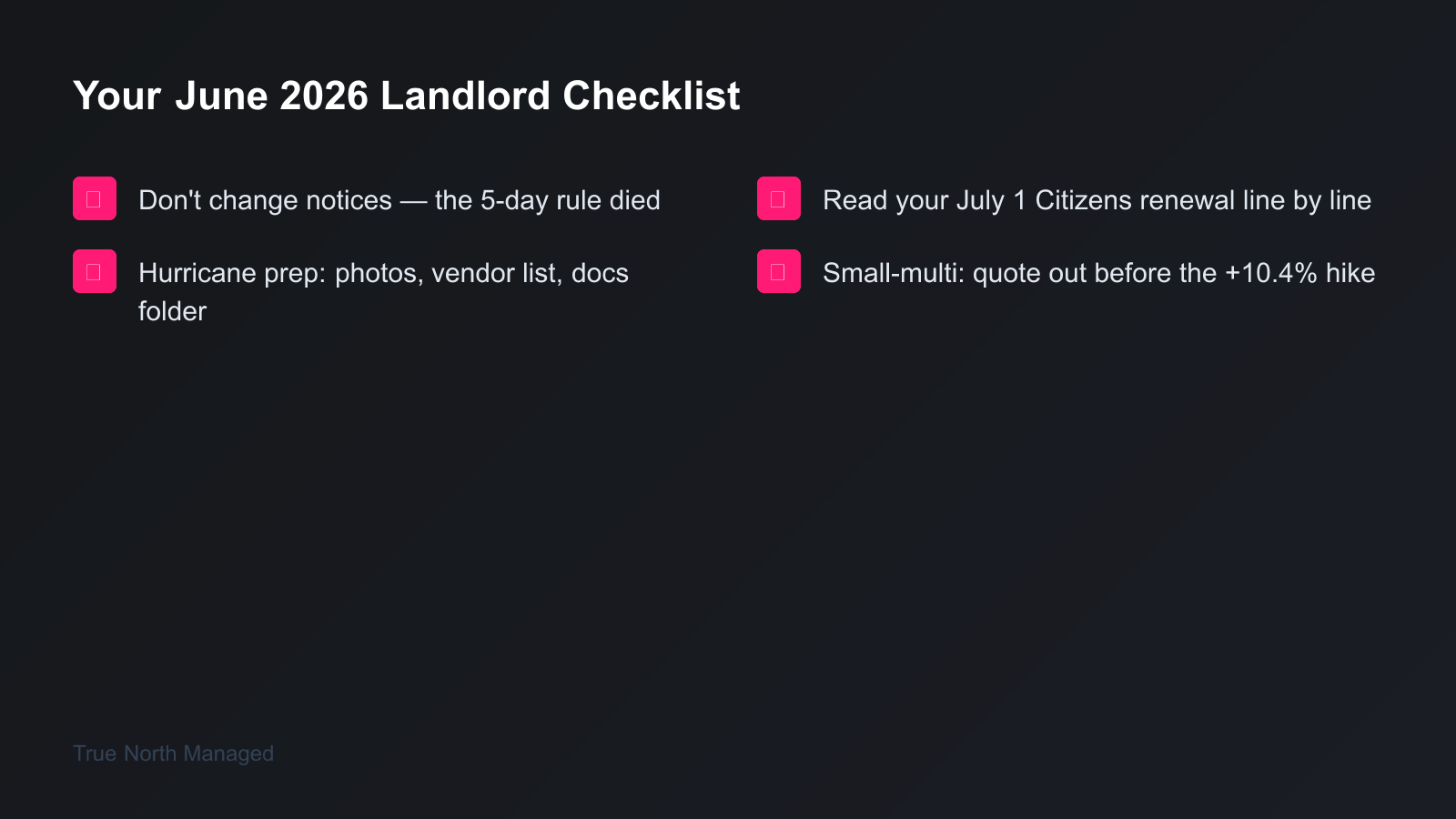

One real deadline, one widely repeated myth, and a storm season — all landing this month. Citizens' insurance rate change takes effect July 1, four weeks out. Hurricane season opened June 1. The rate sheet broke out of its spring range for a second straight week. And the SB 716 five-day eviction notice that half the internet told you to prep for? It died in committee — so the first item on this month's list is not changing your forms. Here are the four June developments that actually belong on your calendar.

Did Florida's new 5-day eviction notice take effect?

No — and this is the June item to get right, because a lot of landlord blogs got it wrong. SB 716 would have replaced Florida's 3-day pay-or-vacate notice with a 5-business-day notice and banned late fees during the grace period. It died in the Senate Judiciary Committee on March 13, 2026, and never became law. Florida Statute 83.56 is unchanged: the nonpayment notice is still three days.

If you updated your forms — or paid a vendor to — based on a "5-day notice effective July 1" headline, walk it back. A pay-or-vacate notice that gives a tenant five days when the statute calls for three doesn't help you; it hands the tenant's attorney an argument that your notice doesn't track the statute, which can get an eviction tossed. Serve the standard 3-business-day notice, base rent only, the way you always have.

Why did so many sources get this wrong? SB 716 was filed in January and written up as if passage were a formality. Bills die quietly — there's no press release when one stalls in committee — so the "coming July 1" articles never got corrected. The takeaway for June: when you see a confident date attached to a Florida landlord-tenant change, check it against the Florida Senate bill page before you change a form.

Did any Florida landlord law actually pass in 2026?

Yes — and this one helps you. While the eviction-notice bill died, HB 1293 cleared both chambers and was signed into law on June 12, 2026 (Chapter 2026-143). It takes effect October 1, 2026, and it creates a new crime: fraudulent entry of a residential dwelling. Move in using a forged ID, a fake paystub, a doctored bank statement, or a lie about who you are, and it’s now a third-degree felony — not a civil mess you chase through county court for months.

The operational win is in the fine print. The law treats a fraudulent move-in as noncompliance with no right to cure, so you don’t owe the usual cure-or-quit window to someone who got in on forged paperwork. It’s a faster off-ramp than a standard eviction, and it’s pointed straight at the forged-lease scams that turned Florida into a national headline. It builds on the existing squatter-removal process rather than replacing it.

One caution, because this is where owners get into trouble: it only works against fraud, not against a real tenant who fell behind. Someone who signed a legitimate lease and stopped paying still gets the standard three-day notice and a trip through county court — skipping that is an illegal lockout. So keep your paper trail tight. The felony hinges on proving the documents were fake, which means your screening records — the application, the ID, the income docs — are the evidence. We’ll cover the mechanics in full as the October 1 effective date approaches.

Is hurricane season worse this year?

No — NOAA is calling for a below-normal 2026 Atlantic season. The season opened June 1 and runs through November 30. NOAA's outlook forecasts 8 to 14 named storms, 3 to 6 hurricanes, and 1 to 3 major hurricanes, with a 55% chance the season runs below average.

Below-normal is good news. It isn't a free pass. Ian made landfall in 2022, a season NOAA classified as near-normal — and it didn't matter how many storms the forecast called for to the people whose roofs came off. June is the prep month, not the storm month. The work happens now, on a calm weekend, while you have time to do it right.

Here's the short list. Walk every property with your phone and shoot date-stamped photo or video of every wall, floor, and appliance. Save a vendor list in two places — a tarp roofer, a tree service, a water-mitigation company you've actually called. Keep your insurance declarations page in a digital folder you can open from anywhere. And if a property sits in a FEMA flood zone, confirm flood coverage is current, because new policies carry a 30-day waiting period.

If you own from out of state, this is the move that matters most for you. You can't drive over to check the shutters. The digital folder and a written storm-communication plan for your tenant carry the work you'd otherwise do in person. We pulled the full checklist together in our guide to getting a Florida rental ready for hurricane season.

What's changing with Citizens insurance rates in 2026?

Citizens' approved 2026 personal-lines rates take effect July 1 for new policies, and at renewal for existing ones. The headline is a decrease: a multiperil average of −8.8%, a wind-only average of −5.5%, and a minimum 2% cut across all personal lines. But Citizens' commercial-residential rates rise on the same date — multiperil about 7.2%, wind-only about 14.4% — and that's the bill small-multifamily owners feel.

This is the first Citizens decrease most Florida homeowners have seen in years, so it's worth reading the renewal carefully instead of just nodding at "−8.8%." Averages hide the spread. Citizens' 2026 rate and rule bulletin sets a statewide average, but your specific premium depends on your county, your wind exposure, and your roof age. When your renewal lands, read the wind premium row against last year and check the roof-age multiplier.

Pull your declarations page now and photograph the mitigation features that earn discounts — storm shutters, roof straps, a roof under ten years old, a hip-roof shape. Those credits only apply if your policy reflects them. And if you own a small multifamily building on a Citizens commercial policy, call your broker for an alternative quote this month, before that increase takes effect. For the bigger picture on coverage, our Florida landlord insurance guide covers what your policy actually has to do.

Where are mortgage rates headed for Florida landlords?

The 30-year fixed touched 6.53% on Freddie Mac's May 28 survey, eased to 6.48% on June 4, then ticked back up to 6.52% the week of June 11 — still parked above the spring range, where rates had hovered between 6.30% and 6.37% for months. The point isn't the weekly wiggle. It's that financing has settled into the low-6.5s and shows no sign of dropping, which keeps would-be buyers renting.Freddie Mac's Primary Mortgage Market Survey tracks the weekly print.

For most readers — owners of one Florida house — this is background noise. It doesn't change what your house rents for. But if you're weighing a purchase or a sale, the move matters. Buyer math tightened a touch. For small-multi buyers, the more interesting story is the deal flow forming behind the rate move: 2021-22 bridge loans written at 4-5% are maturing into a 6.5%-plus refinance market, and the buildings underwritten to old cap rates don't pencil. The right opportunity in this market is a sponsor with a loan they can't refinance — not a Zillow search.

For sellers, there's no distress signal in either Florida metro. Orlando is splitting into submarkets — Lake Nona near 96% occupancy on one end, Kissimmee lease-ups handing out concessions on the other — and the metro is stabilizing, not falling. Tampa's apartment vacancy was a record 10.7% entering 2026, the highest CoStar has tracked since 2000, but single-family rentals in established neighborhoods are still leasing in about three weeks. The throughline holds: price your house to single-family comps in your specific submarket, not to the metro average or the apartment number, and lean toward keeping good tenants over chasing turnover.

Will the 2026 property-tax amendment lower your rental’s tax bill?

Maybe — but not until 2027, and only if voters agree. On June 2 the Legislature put a constitutional amendment on the November 2026 ballot. The piece that matters for landlords: it would cut the annual assessment-increase cap on non-homestead property — your rentals — from 10% to 5%, starting January 1, 2027. It needs 60% approval to pass.

A 5% cap means a rental’s taxable value can’t climb more than 5% in a year, even when the market runs hot — real predictability on the expense line that’s been hardest to forecast. The catch: it’s a tax shift, not a tax cut. The money still has to come from somewhere, so the load can move toward millage rates and fees, and Orlando-area officials have already warned that renters and non-homesteaded owners may absorb the offset.

Nothing changes on your 2026 bill, so there’s no move to make today beyond knowing it’s coming. When you set next year’s rents and reserves, model both outcomes — the current 10% cap if it fails, 5% if it passes. If you want a refresher on how property tax works on a Florida rental, start there. We’ll run the numbers closer to the vote.

The Florida Landlord Briefing covers legislative changes, regulatory updates, market shifts, and practical action items for Orlando and Tampa rental property owners. Last month's edition covered the early-May market signals and the hurricane prep window, and you'll find the full library of guides in our Florida Owner's Guide.

One July 1 deadline, one storm season, a myth cleared up, and a market that rewards holding steady. If you'd like a clear read on what your specific property should rent for — or whether now is the moment to buy, sell, or hold — get a free rental analysis →