Landlord Insurance in Florida: What Property Owners Need

What Florida landlord insurance covers, what it doesn't, what it costs in Orlando, and the coverage gaps that catch rental owners off guard.

If you own a rental in Orlando, you've probably heard that landlord insurance is "recommended." Here's the straight version: Florida law doesn't require it. But if you carry a mortgage, your lender almost certainly does — and even if you own the place outright, skipping it is a gamble most owners shouldn't take. Hurricanes, sinkholes, water damage, liability claims — that's the cost of owning property in Central Florida. The right policy protects the building, your rental income, and the rest of what you own.

• Before a tenant moves in: Replace your homeowners policy with a landlord (dwelling) policy. A homeowners policy on a tenant-occupied home can be denied at claim time.

• If you have a mortgage: Your lender requires landlord insurance — and flood insurance if the property sits in a FEMA Special Flood Hazard Area.

• Aim for a DP-3 policy with a dwelling limit set to replacement cost, $300,000–$1,000,000 liability, and loss-of-rent coverage.

• Review the policy every year — Florida construction costs and flood rules change, and an underinsured rental leaves you paying the gap.

Does Florida require landlord insurance?

No — Florida law does not require landlord insurance. But a mortgage lender will require it as a condition of the loan, and an unmortgaged rental left uninsured exposes the owner to a total, uncovered loss from fire, storm, or a liability lawsuit. In practice, every Florida rental needs a policy.

So the question isn't really "do I need it." It's "do I have the right one." If you became a landlord by accident — you relocated, you inherited the house, you couldn't sell — the most common and most expensive mistake is leaving the old homeowners policy in place. It was written for a home you live in. The day a tenant moves in, that policy is the wrong tool, and an insurer can deny a claim on exactly that basis.

Landlord insurance vs. homeowners: what's the difference?

A homeowners policy covers an owner-occupied home — dwelling, your personal belongings, liability, and living expenses if you're displaced. A landlord policy (a dwelling fire or rental dwelling policy) covers a tenant-occupied home: the structure, liability for injuries on the property, and lost rent when the unit can't be lived in. They are not interchangeable.

Your homeowners policy is built for the house you live in. Landlord insurance — often called a dwelling fire policy or rental dwelling policy — is built for the house you rent out.

Homeowners policies cover your dwelling, personal property, liability, and additional living expenses, and they're underwritten for owner-occupied homes. Rent the property out, file a claim, and the insurer can deny it — the policy wasn't designed for tenant occupancy and the pricing never accounted for that risk.

Landlord policies focus on the structure, liability for injuries on the property, and loss of rental income when the unit becomes uninhabitable. They usually cost 20–30% more than a homeowners policy for a similar rebuild value. They're also the only appropriate coverage for a rental. A homeowners policy on a tenant-occupied home is a coverage gap waiting to bite you.

What are the DP-1, DP-2, and DP-3 dwelling policy tiers?

Landlord insurance comes in three dwelling-policy forms. DP-1 covers named perils only and pays depreciated (actual cash) value. DP-2 covers 18 named perils and pays replacement cost. DP-3 is open-perils — it covers everything except stated exclusions — and pays replacement cost. Most Florida landlords should hold DP-3.

DP-1 (Basic Form). Named perils only — fire, lightning, windstorm, hail, smoke, and a few others. Pays out on actual cash value (depreciated), so you cover the gap between the check and what repairs actually cost. It's the cheapest option and, for most landlords, too thin. See our guide to windstorm insurance for Florida landlords for how storm coverage layers in.

DP-2 (Broad Form). Covers 18 named perils — everything in DP-1 plus freezing pipes, falling objects, water damage, electrical damage, and collapse. Pays replacement cost rather than ACV. Mid-range price. A real step up from DP-1.

DP-3 (Special Form). Open perils — it covers everything except what's explicitly excluded (flood, earthquake, wear and tear, mold from neglect). Pays replacement cost. It's the most complete protection and what most Orlando landlords should aim for. It costs more. But when a pipe bursts at 2 a.m. or a storm peels back part of the roof, DP-3 is the policy you want. Our guide to flood insurance for Florida rentals covers the one big gap DP-3 still leaves.

What does landlord insurance actually cover?

A solid Florida landlord policy gives you three core coverages: property damage to the structure from covered perils, liability for injuries on the property, and loss of rent when a covered loss makes the unit uninhabitable. DP-3 covers the structure on an open-perils basis; liability and loss of rent are added alongside it.

Property damage. Repairs to the structure from covered perils — fire, lightning, wind, hail, vandalism, burst pipes, and more. DP-3 covers "all risk" except the listed exclusions. Set the dwelling limit to your replacement cost, not your purchase price. Florida construction costs have climbed; underinsure the building and you're short exactly when you need to rebuild.

Liability. Medical and legal costs if someone is injured on your property — a tenant, a guest, a delivery driver. Standard advice for Florida landlords runs $300,000–$500,000 in underlying liability, and many agents push $1 million as a baseline. One serious injury or wrongful-death claim can blow past that fast. Umbrella policies stack another $1–5 million on top and typically run $250–$550 a year for $1 million in coverage. If you hold the property in your own name, an umbrella is worth a hard look.

Loss of rent. When a covered loss makes the unit uninhabitable, loss-of-rent coverage reimburses the income you would have collected. Most policies provide 20–25% of the dwelling limit. On a $300,000 dwelling policy, that's $60,000–$75,000 in potential rent replacement — usually six to twelve months depending on your rent. It does not cover eviction, tenant abandonment, or lease violations. It kicks in only when the damage comes from a covered peril and the unit is genuinely uninhabitable.

What does landlord insurance not cover in Florida?

Standard Florida landlord policies exclude flood, exclude gradual water damage and neglect-related mold, and treat sinkhole loss as an optional add-on. They also limit or drop coverage on a property that sits vacant for 30–60 days. Each of these gaps matters in Central Florida.

Flood. Standard policies exclude flood. If your property sits in a FEMA Special Flood Hazard Area and you have a federally backed mortgage, flood insurance is required. Citizens Property Insurance — Florida's insurer of last resort — is phasing in a flood-coverage requirement for its wind policies: structures with a dwelling replacement cost of $500,000 or more from January 1, 2025, $400,000 or more from January 1, 2026, and all remaining personal residential property from January 1, 2027. Even outside a high-risk zone, Orlando sees heavy rain and localized flooding. Private flood policies can include loss-of-rent coverage; the federal NFIP usually doesn't. Check your flood zone and your lender's requirements.

Sinkhole loss. Orlando sits in one of the country's most active sinkhole zones. Florida law splits this in two: "catastrophic ground cover collapse" — a sudden, dramatic collapse that condemns the building — is covered under standard policies, while "sinkhole loss" (gradual damage: foundation cracks, stuck doors, uneven floors) is optional and must be added by endorsement. Florida Statute 627.706 requires insurers to make sinkhole-loss coverage available for an additional premium. If you own or are buying a rental in Central Florida, get a quote for it. The geology here makes it relevant.

Wind and hurricane deductibles. Florida uses percentage-based "named storm" deductibles — typically 2%, 5%, or 10% of your dwelling limit. On a $300,000 policy with a 5% deductible, you pay $15,000 out of pocket before coverage kicks in. That's separate from your standard all-peril deductible. One break: you pay only one hurricane deductible per calendar year per insurer, even if multiple storms hit. Still, budget for that hit. Impact windows, hurricane straps, and a newer roof can sometimes lower your premium or open up better deductible options.

Water damage and mold. Sudden, accidental water damage — a burst pipe, an appliance overflow — is usually covered. Gradual leaks, deferred maintenance, and mold from neglect usually aren't, and many Florida policies cap mold coverage near $10,000. Document your maintenance, fix leaks fast, and require tenants to report problems quickly. Your landlord responsibilities under Florida law include keeping the home habitable — letting problems fester can void coverage.

Vacancy. Standard landlord policies often limit or exclude coverage once a property sits empty 30–60 days. Between tenants, mid-renovation, or waiting on a sale, you may need vacant-property insurance. It costs more — often 10–20% above standard rates — but an empty Orlando rental is a magnet for vandalism, undetected leaks, and mold. Don't assume your policy covers a vacant unit.

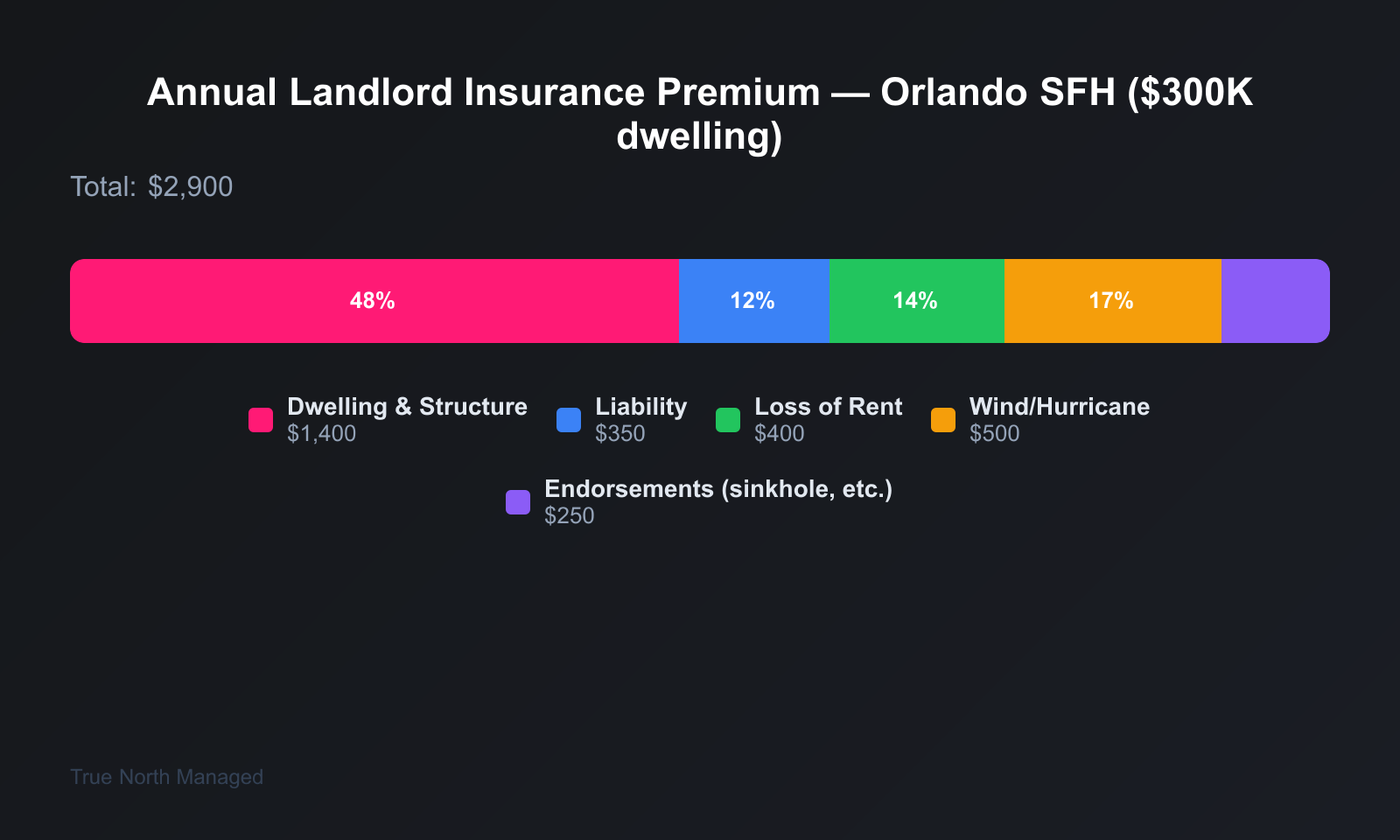

What does landlord insurance cost in Orlando?

Orlando landlord insurance runs about $1,000–$3,000 per year — lower than coastal Florida because Orlando is inland with less hurricane and flood exposure. The statewide average runs higher, closer to $2,300–$2,800, and coastal markets like Miami can top $10,000.

For a typical Orlando single-family home with $300,000 in dwelling coverage, the annual premium usually breaks down like this:

- Dwelling and structure: the bulk of the premium — replacement cost for the building.

- Liability: usually bundled; $300K–$1M limits.

- Loss of rent: often 20–25% of the dwelling limit.

- Wind/hurricane: built into the premium and deductible structure.

- Optional add-ons: sinkhole, ordinance or law, water backup.

Older homes — 15-plus years — often face higher rates or inspection requirements. Storm-resistant upgrades like impact windows, reinforced doors, and hurricane straps can qualify you for discounts. Insurers increasingly ask for maintenance records on roofs, plumbing, and electrical, so having that documentation ready smooths the process.

What is ordinance or law coverage, and do I need it?

Ordinance or law coverage pays the extra cost of rebuilding to current Florida building codes after a loss — including demolition of undamaged portions when code requires it. Standard insurance pays only to repair the damage, not to upgrade. For Florida rentals built before 2010, this coverage is worth keeping.

Florida updates its building codes every three years. If damage exceeds 50% of a building's value, you may have to bring the whole structure — undamaged parts included — up to current code. Standard insurance pays to repair the damage; it doesn't automatically pay for the code-upgrade cost.

Ordinance or law coverage fills that gap: demolition of undamaged portions when codes require it, plus the increased construction cost of meeting current standards. Florida insurers must offer it, and many policies include it at 25% of the dwelling limit unless you decline in writing. For homes built before 2010 — especially pre-1992 or pre-2000 — keep it. Without it, a partial loss can force tens of thousands out of pocket to rebuild to code.

How do pets affect landlord insurance and liability?

Allowing pets adds liability exposure that standard landlord policies often don't fully cover. A Florida landlord can be held liable for a tenant's dog bite if the landlord had actual knowledge the dog was dangerous and the power to remove it. The fix: require tenant renters insurance and set clear pet rules in the lease.

Many Orlando landlords allow pets, and tenant dog bites can create real liability. Standard landlord policies often don't include specific pet liability. Require tenants to carry renters insurance with adequate liability limits, and consider asking to be named as an additional insured on their policy. Your pet policy should spell out breed restrictions and requirements — that cuts risk and supports your defense if something goes wrong.

How do I compare landlord insurance quotes?

Get at least three quotes and compare them on the same terms: dwelling limit set to replacement cost, both deductibles (standard and hurricane), loss-of-rent amount and duration, liability limits, exclusions, and optional endorsements. Rates vary widely by carrier, property age, and location.

- Dwelling limit — does it match your replacement cost?

- Deductibles — standard and hurricane/named storm.

- Loss of rent — amount and duration.

- Liability limits — $300K minimum for umbrella eligibility; $1M is common.

- Exclusions — flood, sinkhole, mold, vacancy.

- Optional endorsements — sinkhole, ordinance or law, water backup.

Carriers writing landlord policies in Florida include Olympus Insurance, American Integrity, and various regional carriers. If you can't find coverage in the standard market, Citizens offers dwelling fire policies for tenant-occupied homes — though not for short-term rentals (more than three rentals a year of under 30 days each). Work with an agent who specializes in investment property; they'll know which carriers are writing in Orlando and what documentation you'll need. If you also own in Tampa, our Tampa landlord insurance guide covers the coastal differences.

The bottom line on Florida landlord insurance

Landlord insurance isn't optional in practice — lenders require it, and going without it exposes you to a catastrophic, uncovered loss. Orlando's inland location keeps premiums below the coast, but you still need the right policy: DP-3 for broad coverage, adequate liability, loss of rent, and add-ons for flood, sinkhole, and ordinance or law where they make sense. Review the policy every year. When you inherit a property or take on a new rental, get it covered correctly from day one.

If you own one rental and the insurance side of being a landlord feels like a lot — choosing the policy form, tracking the flood rules, keeping the maintenance records an insurer will ask for — that's a normal reaction, and it's exactly the kind of thing a property manager handles day to day. We manage single properties too, not just portfolios. A free rental analysis is a no-pressure way to see what your Orlando rental could earn and how we'd help you keep it protected and documented.