How to Prep a Florida Rental for Summer Storm Season

Storm prep on a Florida rental isn't a checklist of shutters — it's a division of labor between you, your tenant, and your insurance. Here's how to settle it before June 1.

Hurricane season opens June 1, and if you own a Florida rental from another state, you already know the hard part: when a storm is three days out, you can't drive over and board a window. By then it's too late to do anything but watch the radar.

So the work has to happen now — and it isn't the work most landlords think it is.

Here's the short version. To prepare your Florida rental for hurricane season, settle a three-way division of labor before the first watch is issued: what the lease obligates your tenant to do, what you as the owner must do, and how your wind and flood insurance split a claim. Storm prep on a rental is a document, not a chore. Let's assign each lane.

What does a Florida landlord actually have to do before hurricane season?

Florida law does not require a landlord to install hurricane shutters, board windows, or otherwise storm-proof a rental — unless the lease specifically says so. What the law does require, under Florida Statute 83.51, is that you keep the roof, windows, doors, and structural components in good repair and meet all building, housing, and health codes. That's a year-round duty, not a storm duty.

This surprises a lot of owners. There's no statute that sends you running to the property with plywood when a storm is named. Your legal obligation is structural soundness — a roof that isn't already failing, windows that aren't already cracked, a building that's up to code. If you keep the structure sound, you've met the law's baseline.

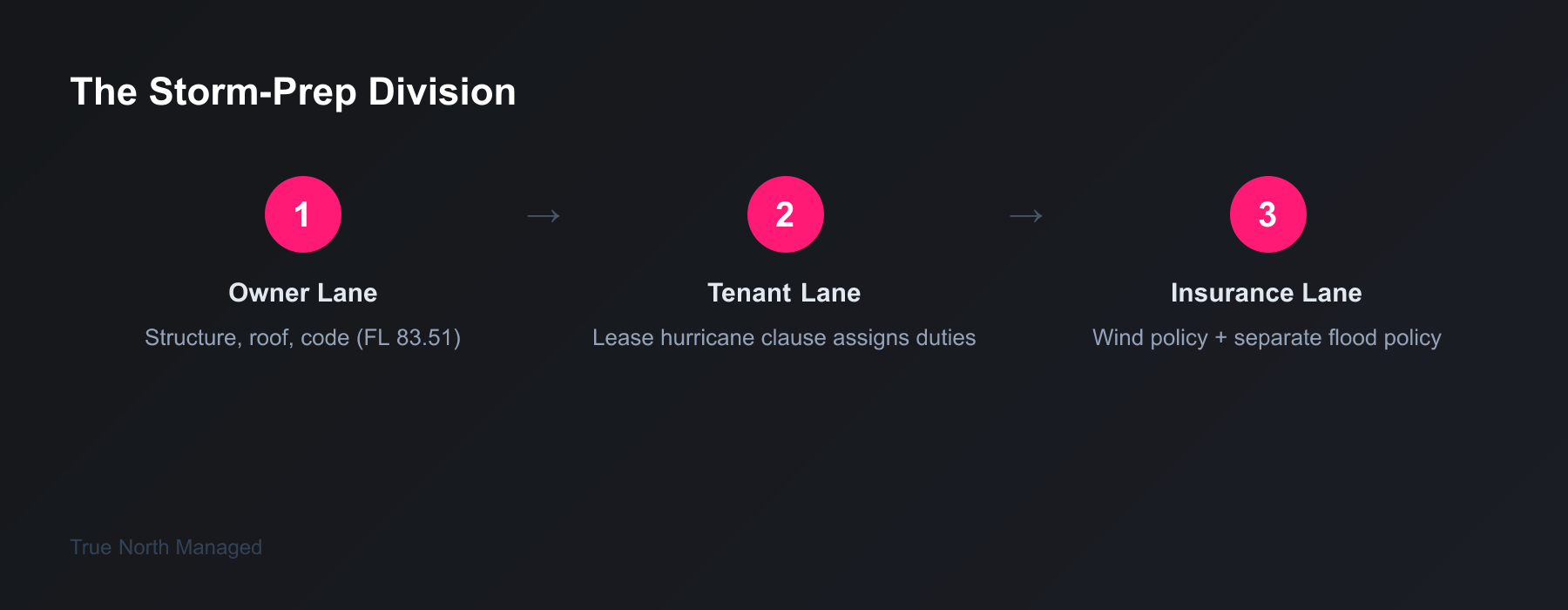

But the law's baseline and a smart storm plan are two different things. Think of the full plan as The Storm-Prep Division — three lanes, each one assigned to a different party before the season opens. Lane one is yours: the structure. Lane two belongs to your tenant. Lane three belongs to your insurance. The owners who get burned are the ones who never assigned lanes two and three.

Your lane, the owner lane, is the physical property. Trim trees away from the roofline. Clear the gutters. Check that the roof has no loose or missing shingles. If the home has shutters or panels, confirm they're present and the hardware works. None of this is legally mandatory — but a failing roof that the law already required you to fix becomes a six-figure problem when 100-mph wind finds it.

What should the lease make the tenant responsible for?

The tenant lane is whatever your lease assigns to it — and if the lease is silent, the tenant has no storm duties at all. For a single-family home or duplex, Florida Statute 83.51 lets you shift most non-structural responsibilities to the tenant by written agreement. The hurricane clause is where you do it.

A solid casualty or hurricane clause puts these duties on the tenant:

- Secure loose outdoor items. Patio furniture, grills, planters, and toys become projectiles in high wind. The tenant brings them in.

- Cooperate with storm preparation. If you send someone to install panels, the tenant gives access and doesn't get in the way.

- Don't block emergency repairs. After the storm, your contractor needs in.

- Report damage promptly. A roof leak found on day one is a repair; the same leak found on day thirty is a mold claim.

- Carry renters insurance. Your landlord policy covers the building — never the tenant's belongings or their relocation costs. Require renters insurance in writing.

One piece of the tenant lane isn't yours to assign — it's the law. Under Florida Statute 83.63, if a storm damages the home badly enough that the tenant's use is substantially impaired, only the tenant gets to decide whether to terminate the lease and move out. You can't terminate it for them. If only part of the home is unusable, the tenant can stay and the rent drops by the fair value of the damaged portion. Knowing this in advance changes how you respond after a storm.

What you must do: pull up your current lease today. If it has no hurricane or casualty clause, add one as a signed addendum before June 1. A lease that's silent on storms isn't a neutral document — it's one that leaves every loose patio chair, every unreported leak, and every uninsured tenant as your problem.

How do wind and flood deductibles split when a storm hits your rental?

One Florida storm can trigger two separate insurance claims with two separate deductibles. Wind damage falls under your landlord (DP-3) policy. Flood damage — including storm surge and rising water — falls under a separate flood policy. When a hurricane delivers both, you file twice, wait on two adjusters, and pay two deductibles.

This is the lane owners understand worst. Start with the wind side. Florida insurers offer hurricane deductible options of $500, 2%, 5%, or 10% of your dwelling coverage, as outlined by the Florida Department of Financial Services. The percentage ones are the trap. On a home insured for $400,000 with a 5% hurricane deductible, you pay the first $20,000 of wind damage yourself before the policy contributes a dollar. Know your number before the season, not after the claim.

Now the flood side. A standard landlord policy excludes flood entirely, so you need a National Flood Insurance Program (NFIP) or private flood policy — with its own deductible. And the timing matters: a new NFIP policy carries a 30-day waiting period before it takes effect. Buy it on June 15 and you have no flood coverage until July 15. To be covered when the season opens, the policy has to be bought by late May.

A few owners think flood is optional because they're not on the coast. Check before you assume. The FEMA Flood Map Service Center shows your property's flood zone by address — zones labeled A, AE, V, or VE are high-risk Special Flood Hazard Areas. And as of January 1, 2026, Citizens policyholders with homes insured above $400,000 must carry flood insurance to keep their wind coverage at all.

Insurance is its own deep topic. Our guide to flood insurance for Florida rentals covers the coverage side, and the hurricane-season insurance documentation guide walks through the photo inventory and paperwork that make a claim go smoothly.

How does an out-of-state owner prep a rental they can't see?

If you own the property remotely, the prep that matters most isn't a task — it's a delegation. You can't physically be there, so the lease has to do the tenant's job, your insurance review has to do the money job, and a named local contact has to do the hands-on job. Set all three before June.

The single most important item is that local contact. Your tenant needs one phone number that reaches a real person when the power's out and water is coming through the ceiling. That can be a handyman you keep on retainer, a trusted neighbor, or a property manager — but it can't be you, 1,000 miles away, when cell towers are down.

Before the season, walk through your owner lane by proxy. Have your local contact or a contractor confirm the trees are trimmed back from the roof, the gutters are clear, the roof has no loose shingles, and any shutters or panels are on site with working hardware. Have them photograph the property's condition with dated images — that's your before picture if a claim ever follows.

Consider the accidental landlord who relocated from Chicago and rents out the old Orlando house. She did the easy part — found a tenant, signed a lease off the internet. The lease said nothing about storms, and she had no one local. When a tropical storm clipped Orange County, her tenant had no number to call, the patio furniture went through a sliding door, and the repair argument lasted a month. None of it was bad luck. It was three unassigned lanes.

Common storm-prep mistakes Florida landlords make

Even careful owners miss the same handful of things every June. Watch for these:

- Reading a quiet forecast as a safe season. NOAA's official 2026 outlook calls for a below-normal season — 8 to 14 named storms, 3 to 6 hurricanes, and 1 to 3 major — with a 55% chance the season runs below normal as El Niño develops. But "below normal" still means storms reach land. One landfall on your street is a 100% season.

- Leaving the lease silent on storms. No hurricane clause means no tenant duties. Add the addendum before June 1.

- The single-deductible blind spot. Assuming one hurricane means one claim. Wind and flood are separate policies with separate deductibles — know both numbers.

- No local contact. A remote owner with no one on the ground leaves the tenant stranded and the property unprotected.

For more on managing repairs you can't oversee in person, our guide to emergency maintenance for Florida rentals covers building a remote response plan, and the post-storm mold prevention guide explains why fast damage reporting matters so much.

Settle the division before the season opens

Storm season is predictable in one way: it arrives the same week every year. That's the advantage. You have until June 1 to turn three vague worries into three assigned lanes — a lease that puts real duties on your tenant, an insurance review that tells you both deductible numbers, and a named local contact who can act when you can't.

If managing a Florida rental from out of state feels like more than you signed up for, that's exactly the job a property manager does — and a good one is your local contact, your storm plan, and your after-hours line all in one. Our Free Rental Analysis is a no-pressure place to start, and the Owner's Guide covers the rest of the Florida landlord playbook. Either way, settle The Storm-Prep Division now. The radar won't wait for you to read your lease.