Citizens Cut Rates — But Your Landlord Policy May Go Up

Citizens cut personal-lines rates 8.8% for 2026 — but apartment and condo-association landlords got an increase on July 1. Here's how to tell which bucket your Florida rental is in.

You probably saw the headline back in January: "Citizens cuts insurance rates 8.8%." If you own a rental in Florida, your next thought was reasonable — does that mean my bill drops too? Here's the honest answer. It depends entirely on which kind of policy you hold. And for a whole lot of landlords, July 1 didn't bring a cut at all. It brought an increase.

That's not a typo. The cut everyone read about is one slice of Citizens' book. A different slice — the one a lot of multifamily and apartment owners sit in — went the other way.

✅ The short version — and what to do• The −8.8% cut is personal lines only. Single-family rentals and small 1–4-unit buildings on a DP-3 dwelling policy got it. • Apartment buildings (5+ units) and condo/HOA associations are commercial residential — those rates went up on July 1, 2026. • Pull your declarations page and find the policy form. That one line tells you which bucket you're in. • Either way, flood is still separate, and the cut shows up at your renewal date — not all at once.

Did the Citizens rate cut apply to landlords?

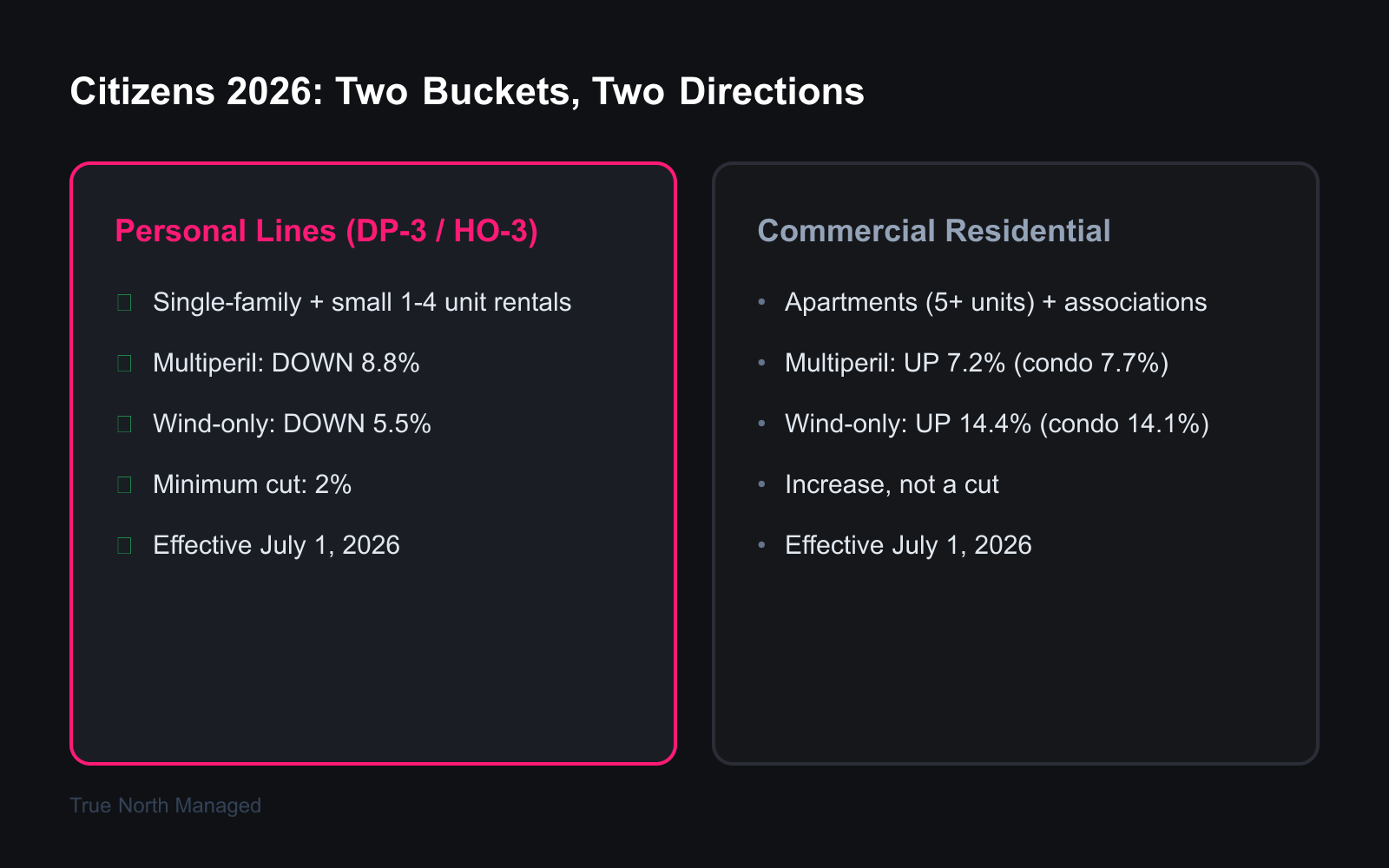

The cut is real, but it's narrow. It applies to Citizens personal lines policies — homeowners and dwelling-fire forms — at an average of 8.8% on multiperil policies, 5.5% on wind-only, with a minimum 2% reduction for every personal-lines policyholder. The numbers took effect July 1, 2026, and it's the first personal-lines decrease Citizens has handed out since 2015.

So if you own a single rental house, you're almost certainly in the bucket that won. Same if you own a duplex, a triplex, or a small fourplex you rent out — those usually sit on a dwelling-fire policy, which Citizens classifies as personal lines. The cut is yours. You don't have to do anything to claim it; it lands when your policy renews.

The catch is the word "personal." Citizens didn't cut every rate. The state's own bulletin announcing the decrease is specific that it's a personal-lines action. The headline writers dropped that qualifier, and that's where the confusion starts — because Florida landlords don't all hold personal-lines policies.

Which Citizens policy bucket are you in?

Two buckets, and they moved in opposite directions. Personal lines residential covers single-family homes and small dwelling-fire rentals — that bucket got the cut. Commercial lines residential covers apartment buildings and condo or HOA associations — that bucket got an increase. Which one you're in comes down to what kind of building you own.

This isn't a marketing distinction. It's written into Florida Statute 627.351, the law that created Citizens. The statute defines personal lines residential coverage as "the type of coverage provided by homeowner, mobile home owner, dwelling, tenant, condominium unit owner, and similar policies." Commercial lines residential is "the type of coverage provided by condominium association, apartment building, and similar policies." Notice where "dwelling" lands — on the personal side. Notice where "apartment building" lands — on the commercial side.

Here's the rule of thumb that covers most landlords:

- One rental house — personal lines. Got the cut.

- A small 1–4-unit building you rent out — usually a DP-3 dwelling policy, personal lines. Got the cut.

- A rented condo unit (your own HO-6 on the unit) — personal lines. Got the cut. (More on the condo wrinkle below.)

- An apartment building with 5 or more units — commercial residential. Got the increase.

- A condo or homeowners association master policy — commercial residential. Got the increase.

If you're fuzzy on the dwelling-fire forms themselves — DP-1 versus DP-2 versus DP-3, and what each one actually pays — our Florida landlord insurance guide breaks them down. For today, the only thing that matters is which side of the personal-versus-commercial line your building sits on.

How much did commercial-residential rates go up on July 1?

If your rental is commercial residential, here are the numbers. Multiperil policies went up an average of 7.2% statewide — 7.7% for condominium associations specifically. Commercial wind-only policies went up 14.4%, and 14.1% for condo associations. All of it took effect on new business and renewals on or after July 1, 2026.

That wind-only line is the one that stings. A 14.4% bump on the wind portion of an apartment building's coverage is a serious number, and it hits hardest where wind exposure is already priced steep — the coast. Citizens spells these increases out in its 2026 rate and rule changes bulletin, and they're not small. On a mid-size apartment building carrying six figures of annual premium, a 7-to-14% increase is real money out of your operating budget.

If you own on both sides of I-4, the coastal-versus-inland gap matters here too. Our Orlando vs. Tampa insurance cost comparison walks through why a Tampa building and an Orlando building rarely price the same — and a wind-only increase widens that gap.

Why is Citizens raising commercial-residential rates while cutting personal lines? Because the commercial book has been priced below where the actuaries say it should be, and Citizens is catching it up. Different bucket, different math, opposite direction.

How do I tell from my declarations page which one I have?

Pull the declarations page — the one-page summary at the front of your policy — and look for the policy form. The form code tells you the bucket. A dwelling-fire form (DP-3, or "DP 00 03," with a Coverage A line labeled "Dwelling") is personal lines. Anything labeled commercial residential, apartment, or an association master policy is the commercial side.

On a dwelling policy, you'll see Coverage A for the dwelling, Coverage B for other structures, and a payout basis of replacement cost. That's the personal-lines fingerprint. A commercial-residential dec page looks different — it'll reference a commercial property form and usually a per-building or blanket limit across multiple units.

Own the property from out of state and don't have a paper copy in front of you? You don't need one. Ask your agent directly. A single email does it: "Is my policy personal lines or commercial residential, and what's the form number?" That one answer tells you whether July 1 helped you or cost you. Keep the reply — your dec page is also the document you'll reach for after a storm, which is exactly why we tell every owner to keep their insurance documentation current and accessible.

I own a rented condo — does the increase hit me?

Sort of, sideways. Your unit's HO-6 policy is personal lines, so your own coverage got the cut. But the condo association's master policy is commercial residential — it got the 7.7% multiperil increase. And associations don't eat those increases. They pass them to owners through higher dues or a special assessment.

So your personal premium can drop a few percent while your association bill climbs. Florida requires every HO-6 policy to carry at least $2,000 in loss-assessment coverage, but on a rented condo, $2,000 won't cover much. If you own a condo you rent out, this is the year to check your loss-assessment limit and ask your board what the master-policy renewal did to the budget.

What should Florida landlords do now?

Start with the dec page — confirm which bucket you're in and don't assume the headline applies to you. If you're personal lines, watch for the cut at your renewal date; it phases in policy by policy, not all at once. If you're commercial residential, build the increase into your 2026 operating budget now and get fresh quotes from the private market. Then there's the eligibility rule. And flood, which is its own line item no matter which bucket you're in.

On the private-market point: Citizens is the insurer of last resort, and its 20% rule still governs. If a private carrier will cover your building within 20% of your Citizens premium, you're not eligible to stay on Citizens — and depopulation may move you whether you ask or not. With a commercial-residential increase landing, this is a good year to see what the private market will write, because the gap that kept you on Citizens may have narrowed. The broader Florida market has softened: private carriers have filed rate decreases of 5 to 15% for 2026, and Citizens' own policy count has fallen roughly 76% from its 2023 peak.

And flood. Neither the cut nor the increase touches it. Flood is excluded from both personal and commercial property policies and bought separately — our flood insurance guide for Florida rentals covers the one gap that catches owners off guard at claim time. For the bigger picture on running a Florida rental the right way, the Florida Owner's Guide pulls the pieces together.

Common mistakes landlords make reading insurance headlines

A few traps, and they're easy to fall into.

Assuming the cut is universal. It's personal lines. If you own an apartment building, the July 1 headline was about somebody else's policy.

Budgeting for relief on a multifamily building. Penciling in a lower insurance line for a 5-plus-unit property in 2026 sets you up for a budget miss. That building got the increase.

Ignoring the wind-only number. The 14.4% wind-only bump is bigger than the 7.2% multiperil figure and easy to skim past. If your building carries wind-only, that's your real number.

Confusing the recommendation with the approved rate. Back in December, Citizens recommended a 2.6% average personal-lines cut effective June 1. That was a proposal. Regulators then approved the deeper 8.8% multiperil cut effective July 1. If you're still anchored to the 2.6% figure, you're reading old news.

Frequently asked questions

Does the Citizens 2026 rate cut apply to landlords? Only to landlords on personal-lines policies — single-family rentals and small 1–4-unit buildings on a dwelling-fire (DP-3) form. Those got the average 8.8% multiperil cut. Apartment and association owners on commercial-residential policies did not.

What is the Citizens commercial-residential rate increase for 2026? Commercial-residential multiperil went up an average of 7.2% (7.7% for condominium associations), and commercial wind-only went up 14.4% (14.1% for condo associations), effective on or after July 1, 2026.

How do I know if my rental is on a personal-lines or commercial-residential policy? Check the policy form on your declarations page. A dwelling-fire form (DP-3 / DP 00 03) with a "Dwelling" coverage line is personal lines. A commercial property form or an association master policy is commercial residential. If unsure, ask your agent for the form number.

When do the 2026 Citizens rate changes take effect? Both the personal-lines cut and the commercial-residential increase took effect July 1, 2026, for new business. Existing policies see the change at their renewal date, so the reduction or increase phases in across the year rather than all at once.

Does the increase affect landlords who own a single rented condo unit? Your unit's HO-6 policy is personal lines and got the cut. But the condo association's master policy is commercial residential and got the increase — which the association can pass to you through higher dues or a special assessment.

Is the −2.6% Citizens rate figure still accurate? No. The 2.6% average cut was a December 2025 recommendation effective June 1. Regulators later approved a deeper 8.8% average multiperil cut effective July 1, 2026, which superseded the earlier figure.

The bottom line

"Citizens cuts rates" was true — for personal-lines policyholders. If you own a single rental house or a small dwelling-fire building, congratulations, the cut is yours and it shows up at renewal. If you own an apartment building or a condo association sits between you and your coverage, July 1 went the other way, and the smart move is to budget for it and shop the market while it's soft. The headline isn't wrong. It's just not about everyone.

If you own one rental and the insurance side feels like a moving target — which form you hold, which way your rate moved, whether you're overpaying Citizens when a private carrier would write you cheaper — that's the kind of thing a property manager tracks so you don't have to. We manage single properties, not just portfolios. A free rental analysis is a no-pressure way to see what your Florida rental could earn and where your insurance dollars are actually going.