Flood Insurance for Florida Rental Properties: NFIP vs. Private Market

Your landlord policy will not cover flood. Here is how to choose between NFIP and private flood insurance for a Florida rental — and when it is required.

Florida rental properties face flood risk from hurricanes, storm surge, and plain heavy rain — and your landlord policy doesn't cover any of it. Flood is always a separate policy. Here's how to choose between NFIP and the private market, when coverage is required, and what a single-property owner actually needs to know.

If your rental has a mortgage and sits in a FEMA Special Flood Hazard Area (Zone A or V): flood insurance is mandatory — your lender requires it, and they can force-place a costlier policy if you don't.

Before hurricane season: buy now if you're buying at all. A new NFIP policy has a 30-day waiting period (waived only when a lender requires it at closing). A policy bought in June won't cover an August storm.

Check your zone: look up your exact address on the FEMA Flood Map Service Center before you decide anything.

Does a Florida landlord policy cover flood damage?

No. A standard landlord (DP-3) policy specifically excludes flood. Flooding from storm surge, a swollen river, or heavy rainfall is never covered by your regular property insurance — you need a separate flood policy, either through the National Flood Insurance Program (NFIP) or a private carrier. This is the single most common and most expensive misunderstanding Florida landlords have.

Wind-driven rain that enters through a roof your insurer agrees the wind damaged may be covered by your windstorm coverage. But rising water on the ground — the kind of flooding Florida sees most — is flood, and only a flood policy pays for it.

When is flood insurance required for a Florida rental?

Flood insurance is required when your rental has a federally backed mortgage (FHA, VA, Fannie Mae, Freddie Mac) and the property sits in a FEMA Special Flood Hazard Area — Zone A or Zone V. The lender mandates it for the life of the loan. If you own the property free and clear, coverage is optional — but in flood-prone Florida, "optional" is not the same as "unnecessary."

Even outside the high-risk zones, many Florida lenders require flood coverage anyway. And about one in four flood claims comes from properties outside the mapped high-risk areas. Your inland Orlando rental in Zone X isn't risk-free — riverine flooding and rainfall flooding don't follow the lender's map.

What is NFIP flood insurance and what does it cover?

The National Flood Insurance Program is the federal flood insurance option, available through FloodSmart.gov and most insurance agents. Coverage is standardized: building coverage caps at $250,000 for a residential structure, and contents coverage caps at $100,000. Premiums are set by FEMA.

Two things matter for landlords. First, NFIP building coverage tops out at $250,000 — if your rental costs more than that to rebuild, NFIP alone leaves a gap. Second, and this is the big one: NFIP does not cover loss of rents. If a flood makes your rental uninhabitable for six months, NFIP pays to repair the building but nothing for the rent income you lose while it's empty.

How did Risk Rating 2.0 change flood insurance premiums?

Risk Rating 2.0 is FEMA's pricing model, fully rolled out in April 2023. Instead of pricing a policy on its flood zone alone, it prices each property individually — using distance to water, flood frequency, building characteristics, and rebuilding cost. The result: two houses on the same street can carry very different premiums.

Some Florida properties saw premiums drop under the new model. Others saw sharp increases. The only way to know where yours lands is to get a current quote. Don't assume last year's number, and don't assume the previous owner's number — Risk Rating 2.0 reprices on a property-specific basis.

Should you choose private flood insurance or NFIP?

For a landlord, the deciding factor is usually loss-of-rents coverage. NFIP doesn't offer it. Many private flood carriers do — covering lost rent for 12 to 24 months while a flooded rental is repaired. Private policies also offer higher building limits (well above NFIP's $250,000 cap), replacement-cost contents coverage, and sometimes shorter waiting periods.

Private flood often runs 10–30% cheaper than NFIP for properties with favorable risk — newer construction, elevation above the base flood elevation, a moderate-risk zone. The tradeoff: private carriers aren't federally backed and can choose to non-renew, while NFIP renewal is guaranteed. For a coastal Tampa property you'll own for decades, that stability has real value.

The practical move: get quotes from both NFIP and at least one private carrier before you decide. An agent who specializes in Florida coastal property can run both. Compare not just the premium but the loss-of-rents coverage, the building limit, and the deductible.

What should you consider when insuring a rental in a high-risk flood zone?

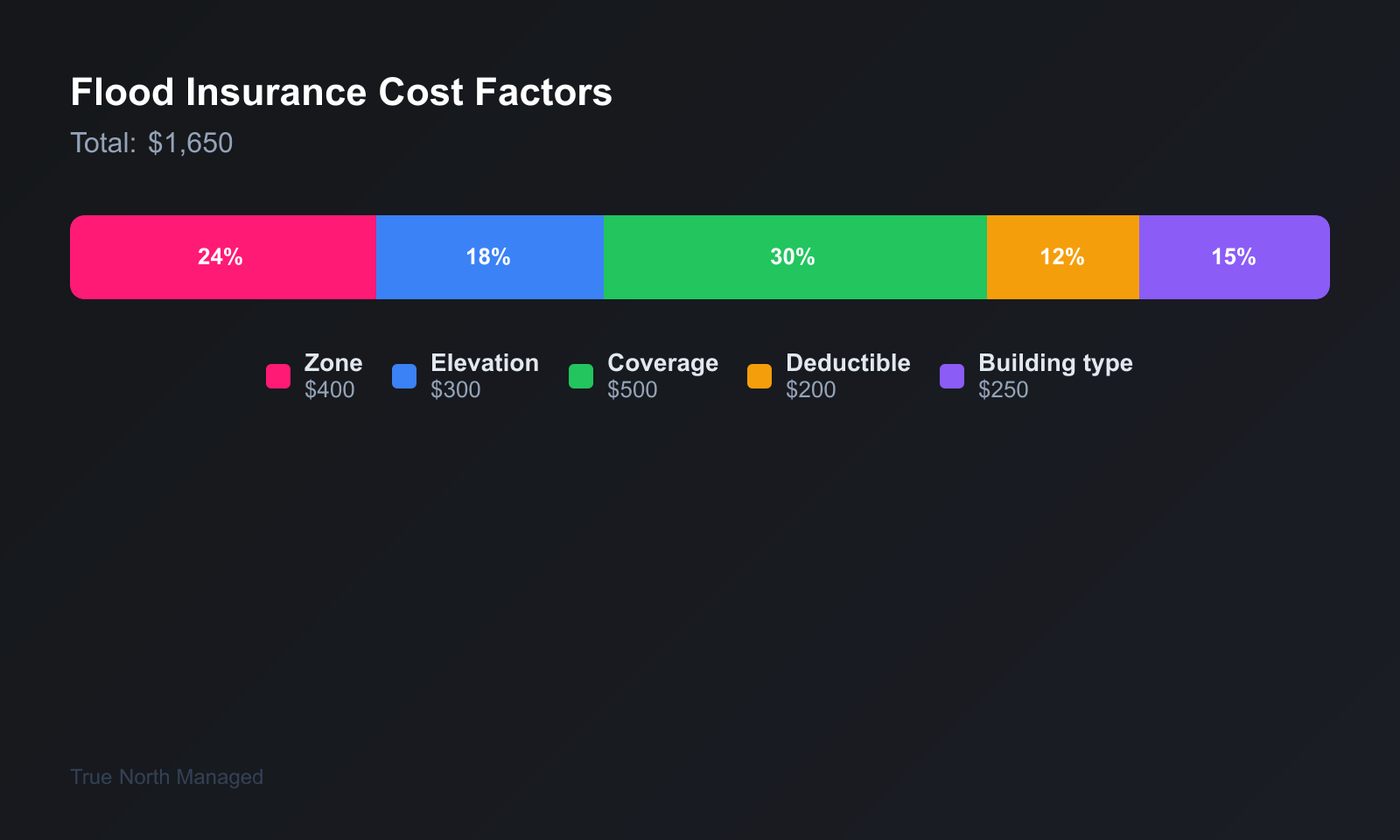

For a rental in a high-risk zone (Zone A or V), weigh five things: the building limit relative to your full rebuild cost, whether the policy includes loss-of-rents coverage, the deductible you can absorb, whether an elevation certificate could cut your premium, and the carrier's renewal stability. In a high-risk zone, the gap NFIP leaves on rebuild cost and lost rent is exactly where a flood will hurt most.

Elevation certificate. If your property's lowest floor sits above the base flood elevation, an elevation certificate documents it and can significantly reduce premiums in a high-risk zone. It costs roughly $500–$1,000 from a licensed surveyor, stays with the property, and often pays for itself within a year or two in a Zone A property.

Cost benchmarks. NFIP premiums in Florida vary widely. In a moderate-risk zone, expect roughly $500–$1,500 a year for a typical single-family rental. In a high-risk zone, $2,000–$4,000 or more is common. Private quotes can come in 10–30% lower for a favorable-risk property — get both before you buy, and factor the number into your cash-flow math.

How does flood exposure differ between Orlando and Tampa?

Tampa and Orlando face different flood risks, and that changes your coverage decision. Coastal Tampa and Pinellas County properties face hurricane storm surge — the most destructive and most expensive flood exposure in the region. Inland Orlando properties face riverine flooding and rainfall flooding, especially low-lying areas and properties near lakes or retention ponds.

Neither metro is flood-free. Check the FEMA Flood Map Service Center for your exact address — flood risk is parcel-specific, not city-wide. Flood is one piece of a complete Florida rental protection plan; pair it with solid landlord insurance and windstorm coverage.

Common flood insurance mistakes Florida landlords make

Assuming the landlord policy covers flood. It doesn't. Flood is always separate.

Dropping coverage when the mortgage is paid off. No lender requirement doesn't mean no risk. One flood can wipe out the equity you just finished paying for, and your tenants' belongings are exposed too.

Buying NFIP only and ignoring the loss-of-rents gap. NFIP repairs the building but pays nothing for the months of lost rent. For a landlord, that gap is the whole point of insurance.

Waiting until hurricane season. A new NFIP policy has a 30-day waiting period. Buy in May, not when a storm is in the Gulf.

Not documenting contents. If you provide appliances or furniture, photograph and list them. A contents claim without documentation is a hard claim to win.

Frequently asked questions about flood insurance for Florida rentals

Does landlord insurance cover flood damage in Florida?

No. A standard landlord (DP-3) policy excludes flood. Flooding from storm surge, rivers, or heavy rain requires a separate flood policy through the NFIP or a private carrier.

What should I consider when choosing flood insurance for a rental in a high-risk zone?

Weigh five things: the building limit against your full rebuild cost, whether the policy includes loss-of-rents coverage (NFIP does not), the deductible you can absorb, whether an elevation certificate could lower your premium, and the carrier's renewal stability. In a high-risk zone, NFIP's gaps on rebuild cost and lost rent are where a flood hurts most.

Does NFIP flood insurance cover lost rent?

No. NFIP pays to repair the building but does not cover loss of rental income while the property is uninhabitable. Many private flood policies do cover loss of rents, typically for 12 to 24 months — a key reason landlords compare private carriers against NFIP.

What are the NFIP coverage limits for a rental property?

NFIP residential building coverage caps at $250,000 and contents coverage at $100,000. If your rental costs more than $250,000 to rebuild, NFIP alone leaves a gap, and you would need a private policy or an excess flood policy for full replacement cost.

Is flood insurance required for a rental property in Florida?

It is required if the property has a federally backed mortgage and sits in a FEMA Special Flood Hazard Area (Zone A or V). Many Florida lenders require it outside high-risk zones too. If you own the property free and clear, coverage is optional but still strongly advised.

How long does it take for flood insurance to take effect?

A new NFIP policy has a 30-day waiting period before it takes effect. The waiting period is waived when coverage is required by a lender as a condition of closing. Buy well before hurricane season — a policy purchased in June will not cover an August storm.

Is private flood insurance cheaper than NFIP in Florida?

For properties with favorable risk — newer construction, elevation above the base flood elevation, a moderate-risk zone — private flood often runs 10–30% less than NFIP. Private carriers can also offer higher limits and loss-of-rents coverage, but they are not federally backed and can non-renew. Get quotes from both before deciding.

Flood insurance is one of the bigger line items in a Florida rental budget, and it's the one most owners underestimate. Get the zone right, compare NFIP against a private quote, and don't let the loss-of-rents gap catch you off guard.

If you own one Florida rental and the insurance math is starting to feel like a second job, you don't have to sort it alone. We manage single Orlando and Tampa rentals — not just portfolios — and we factor real insurance costs into the numbers. Get a free rental analysis and we'll show you where your property stands.