Orlando vs. Tampa: Where Should You Buy Your First Florida Rental?

A first-time investor's decision guide to picking between Orlando and Tampa for your first Florida rental, broken down by entry price, rent, insurance, and goal.

If you're trying to decide where to buy your first Florida rental, the Orlando vs. Tampa rental investment question is probably keeping you up at night. Both metros sit in the same state, follow the same landlord-tenant law, and ride the same population boom. Yet they reward different kinds of investors. Tampa pays you in rent if you can stomach the insurance bill. Orlando pays you in growth if you can afford to wait. This guide breaks down the eight things a first rental buyer actually cares about, then shows you how to pick based on your own goal.

A quick note first: if you already own a property and didn't plan to rent it out, you're not really choosing a metro. You're managing what you have. Start with our guide for Florida's accidental landlords instead. This post is for buyers actively shopping for their first deal.

Is Orlando or Tampa the better market for a first rental?

For most first-time investors in 2026, Orlando edges out Tampa on stability and Tampa edges out Orlando on raw rent for a single-family house, but the real deciding factor is insurance. Orlando sits inland with lower wind and flood exposure, so your carrying costs are more predictable. Tampa offers stronger single-family rents but coastal insurance that can erase the difference.

Neither metro is "better" in a vacuum. They're better for different goals, which is the whole point of this comparison. Before you fall in love with a listing, you need to know what each market asks of you and what it gives back. Let's break it down piece by piece.

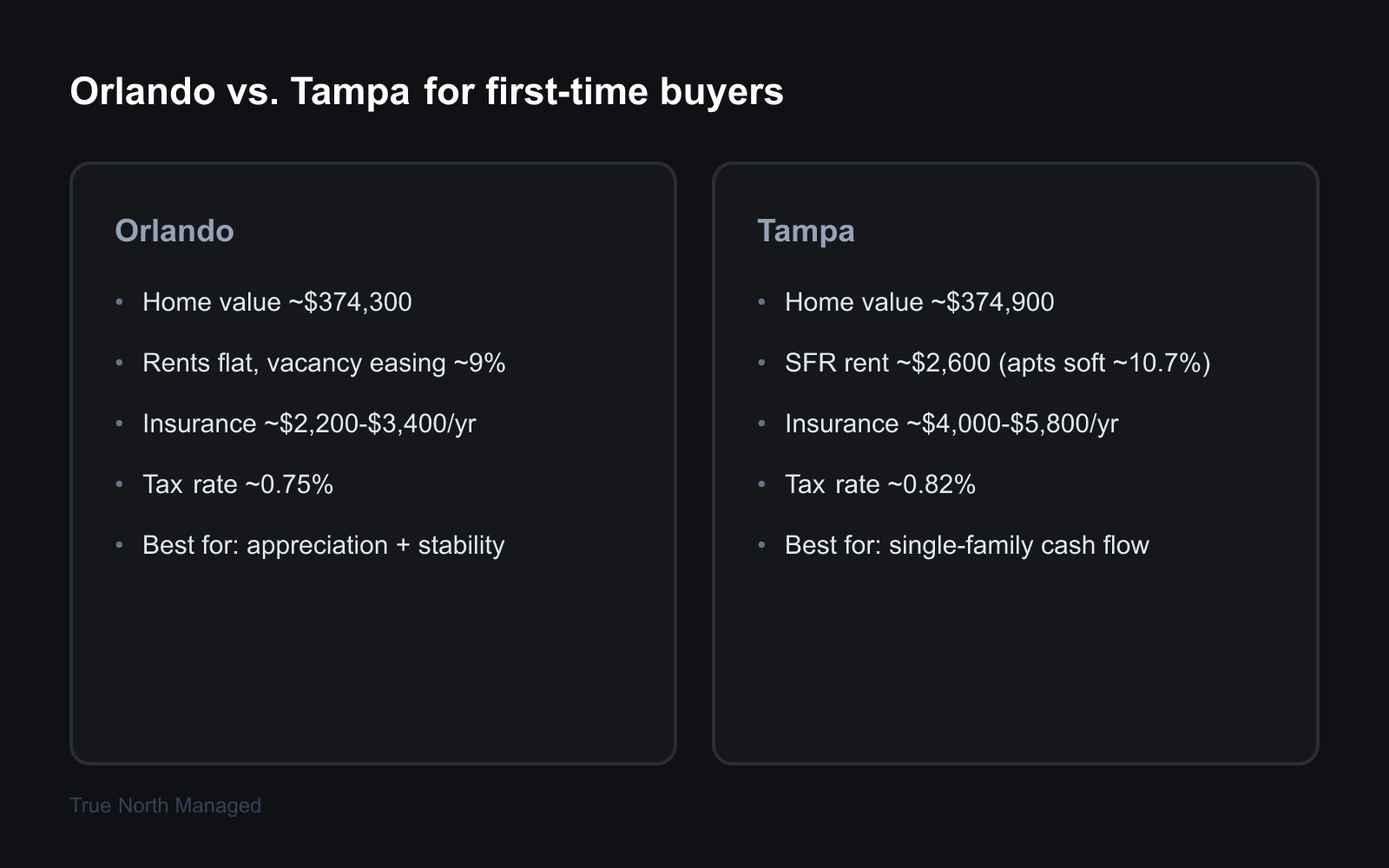

How do entry prices and rents compare in Orlando vs. Tampa?

Entry prices are close. As of spring 2026, the Zillow Home Value Index put the typical Orlando metro home near $374,300 (down about 3.2% year over year) and the typical Tampa home near $374,900 (down about 3.5%) — and across the broader Tampa–St. Petersburg metro, the typical home runs a bit lower still. Either way, you're paying roughly the same to get in. Rents are where the markets split: Tampa's single-family houses rent higher, while its apartments are soft.

Here's the side-by-side a first-time buyer needs:

| What you care about | Orlando | Tampa |

|---|---|---|

| Counties | Orange, Seminole, Osceola | Hillsborough, Pasco |

| Typical home value (Zillow ZHVI, spring 2026) | ~$374,300 (−3.2% YoY) | ~$374,900 (−3.5% YoY) |

| Single-family rent (typical) | Flat to slightly down | ~$2,600/mo, up ~4% YoY |

| Apartment vacancy | ~9% (easing) | ~10.7% (record high, March 2026) |

| Homeowners insurance, $300k dwelling | ~$2,200–$3,400/yr | ~$4,000–$5,800/yr (surge zones) |

| Effective property tax rate | ~0.75% (Orange) | ~0.82% (Hillsborough) |

| Top demand drivers | Tourism, healthcare, Lake Nona | Healthcare, USF, MacDill AFB |

| Best fit | Appreciation, stability | Single-family cash flow |

A few of those numbers deserve real-world context. In Orlando, the priority ZIPs we track sit around $2,059 median rent on roughly $470,700 of home value (Zillow data, as of April 2026). Lake Nona (ZIP 32827) runs about $2,341 in rent against $643,100 in value. Avalon Park near UCF (32828) sits near $2,121, up a hair year over year.

In Tampa, our tracked ZIPs land near $2,044 median rent on about $466,900 of value (same April 2026 Zillow data). South Tampa near MacDill (33611) rents around $2,312, up 1.7%. Push out to Riverview (33578) and you're closer to $1,988 in rent on just $338,000 of value, which is the kind of price-to-rent math that catches a first-timer's eye. For a deeper neighborhood breakdown, see our guides on average rent across Orlando and how much rent you can charge in Tampa.

One thing every buyer faces in both metros: financing. The 30-year fixed mortgage averaged 6.52% the week of June 11, 2026, per Freddie Mac's weekly survey. That rate is the same whether you buy in Orange County or Hillsborough, so it cancels out of the decision. What doesn't cancel out is everything below.

Why does Tampa have higher vacancy than Orlando right now?

Tampa's roughly 10.7% apartment vacancy is a record high, but it's almost entirely a supply story, not a demand problem. Builders delivered more than 12,500 apartment units in 2024 alone and another 7,500-plus in 2026. That wave outran even Tampa's strong population growth, so landlords are competing on price and concessions.

Here's the part that matters for a first-time buyer, and the part most comparison articles skip: that vacancy number is an apartment number. If you buy a single-family house or a small duplex, you're not competing with a 300-unit complex offering two months free. Single-family rental supply isn't expanding the way apartments are, which is exactly why Tampa's house rents held up around $2,600 and even nudged higher while apartment rents fell toward $1,768.

Orlando went through its own supply surge and is now on the other side of it. Apartment vacancy peaked near 11% in late 2024 and has eased back toward 9%, with the construction pipeline down roughly 40% from its peak. The takeaway: don't let Tampa's scary apartment headline scare you off a house. Just buy the right property type for the market you're in.

How much more does insurance cost in Tampa vs. Orlando?

Insurance is the single biggest cost difference between the two metros, and it's the one that catches new investors off guard. On a $300,000 dwelling, Orlando's inland location keeps homeowners premiums roughly in the $2,200–$3,400 range, while Tampa Bay properties in storm-surge zones can run $4,000–$5,800. That gap can be $2,000 or more every single year.

Then there's flood insurance, which is separate from your homeowners policy and excluded from nearly every standard policy. In the Tampa Bay area, flood coverage runs about $700–$1,800 for moderate-risk zones and $2,500 to well over $10,000 for high-risk coastal properties. Much of metro Orlando sits in lower flood-risk inland zones, so many owners pay far less or skip mandatory flood coverage entirely.

There's good news on both sides: the Florida insurance market is softening in 2026, with several carriers filing 5–10% rate reductions after recent tort reform. But the structural difference remains. When you run your numbers, pull a real quote for the specific address before you write an offer. A house that cash-flows on paper in Tampa can go negative once a surge-zone premium lands on the statement. Run that line first, not last.

What about property taxes in Orange vs. Hillsborough County?

Property taxes tilt slightly in Orlando's favor, but the gap is small. Orange County's effective property tax rate runs about 0.75%, with a typical annual bill near $3,227. Hillsborough County sits a touch higher at roughly 0.82%, with a median annual payment around $3,453. On a $375,000 property, that's a difference of a couple hundred dollars a year.

That's real money, but it's not a deal-maker or a deal-breaker on its own. Remember that Florida reassesses property when it sells, so your tax bill as a new buyer will be based on your purchase price, not the prior owner's lower assessed value. Budget for the bump. The bigger county-level cost difference, by a wide margin, is insurance, not taxes.

Who rents in each metro, and is the demand reliable?

Both metros have deep, durable renter demand, but it comes from different engines. Orlando's tenant pool is driven by tourism, healthcare, and the fast-growing Lake Nona Medical City, which is projected to create up to 30,000 jobs. Tampa's renters lean on healthcare, the University of South Florida, and MacDill Air Force Base, whose military tenants come with steady housing allowances.

Orlando is the bigger growth story. The metro reached roughly 2.94 million people in mid-2024 and grew 2.7% in a single year, the fastest among U.S. metros over a million residents, per Census Bureau estimates. Osceola County alone grew 4.7%, consistent with the state's own demographic estimates. The May 2025 opening of Universal's Epic Universe added thousands of hospitality jobs on top of that. More people moving in means more tenants competing for your unit.

Tampa's demand is steadier and arguably more recession-resistant. Healthcare is the metro's largest hiring sector, and MacDill anchors about 30,000 workers whose housing allowance makes them reliable, long-term tenants. For the specific data on absorption and rent trends each quarter, our Orlando vs. Tampa market pulse tracks the numbers in detail. Both markets pass the "will my unit rent?" test. The question is what kind of tenant and how fast.

Is the law more landlord-friendly in one metro?

No. Florida landlord-tenant law is statewide, so Orlando and Tampa play by identical rules. There is no security deposit cap in either city, you must notify a tenant within 30 days of how their deposit is held, and you return it within 15 days if you make no claim or 30 days if you do. Evictions follow the same statutory process. None of that changes when you cross a county line.

This trips up a lot of first-time investors who assume one metro is "easier" to be a landlord in. The Florida Residential Landlord and Tenant Act, Chapter 83, governs both. Florida also bans local rent control statewide, so neither city can cap what you charge. What actually differs between the metros isn't the law. It's the cost of carrying the property (insurance, taxes) and the speed of finding a tenant (vacancy, demand). Focus your energy there.

One small local wrinkle: short-term rentals. If you're picturing an Airbnb, know that Orange County's rules are fairly strict in single-family residential zones, and both metros require a state vacation-rental license. Don't assume a short-term strategy works the same as a traditional 12-month lease. Most first rentals should be a standard annual lease anyway.

What should an out-of-area buyer plan for in each market?

If you're buying from out of state, plan for the same core challenge in both metros: you can't see, screen, or fix anything in person. That means a local property manager isn't optional, it's the difference between a rental and a liability. Florida managers typically charge 8–10% of collected rent, plus a tenant-placement fee, and they handle showings, screening, rent collection, and maintenance.

The remote-ownership playbook is identical whether you land in Orlando or Tampa, and we cover it fully in our guide for the out-of-state Florida landlord. The one market-specific item: in Tampa, insist on a flood-zone determination and, for high-risk addresses, an elevation certificate before closing. From 1,000 miles away you can't eyeball whether a house sits in a surge path. That single document can save you thousands a year in flood premiums or warn you off a property entirely.

Whichever metro you pick, get your first lease, screening, and rent-pricing process right from day one. The most expensive mistakes happen early, which is why we keep a running list of the first-time landlord mistakes we see most often. Read it before you sign anything.

How to choose your Orlando vs. Tampa rental investment by goal

Pick your metro based on what you want the property to do for you. If you want monthly cash flow, lean Tampa single-family. If you want long-run growth, lean Orlando. If you want the steadiest, most predictable ride, lean Orlando inland. Here's the logic behind each path.

If your goal is cash flow, Tampa's single-family houses give you the strongest rent-to-price math in 2026, especially in growing suburbs like Riverview where you can buy in the $330,000s and rent near $2,000. Just underwrite the insurance and flood line conservatively, because a surge-zone premium can flip a positive number negative. Run that quote before you commit.

If your goal is appreciation, Orlando's population and job growth give it the longer runway. The metro is adding residents and jobs faster than almost anywhere in the country, and engines like Lake Nona and the theme-park economy keep pulling people in. You may cash-flow thin at first, but a property that breaks even today can look like a winner in five years.

If your goal is stability, Orlando's lower insurance, lower taxes, and inland location make your monthly numbers easier to predict, which is exactly what a nervous first-timer needs. Fewer surprises beats a slightly higher rent when it's your first deal and you're learning the ropes.

The honest answer for most first-time buyers? Either metro works if you buy the right property type and budget insurance correctly. The wrong move is buying a Tampa surge-zone house on apartment-level rent assumptions, or buying in Orlando expecting Tampa's single-family rents. Match the property to the market, and match the market to your goal. For the bigger picture on building a Florida portfolio, start with our Florida Owner's Guide.

Not sure which metro your budget and goals point to? We manage rentals in both Orlando and Tampa, and we'll tell you straight which market fits your first deal. Get a free rental analysis and we'll run the real numbers, insurance included, for the property you're considering.