Hurricane Season 2026: The Insurance Documentation Most Florida Landlords Skip

The 2026 hurricane season forecast looks calmer than 2024 — but 34.8% of Milton claims still went unpaid. Here's the documentation protocol that separates paid claims from denial letters.

Hurricane Season 2026: The Insurance Documentation Most Florida Landlords Skip

Every landlord in Florida knows they should trim their trees and board their windows before hurricane season. Most do. And most still end up fighting their insurance company after the storm.

The reason isn't lazy preparation — it's lazy documentation. The photos you take before the storm determine whether your claim gets paid. Not the shutters. Not the sandbags. The photos.

Hurricane Milton closed 34.8% of claims without payment in 2024. That's 134,177 claims — $5.6 billion in uncompensated losses across Florida. And the 2024 season wasn't even above average.

Here's the documentation protocol that separates paid claims from denial letters — whether you manage one Orlando duplex or a portfolio of Tampa rentals.

For the broader preparation guide — shutters, tree trimming, tenant communication — see our complete hurricane preparation checklist for Florida rental properties.

What Does the 2026 Hurricane Season Forecast Look Like?

The 2026 Atlantic hurricane season is forecast to be below average — 9 to 13 named storms, 4 to 6 hurricanes, and 1 to 3 major hurricanes. NOAA issued an El Niño watch in March 2026, and El Niño typically suppresses hurricane activity by increasing wind shear over the tropical Atlantic.

Don't let the forecast make you complacent. Tampa Bay was specifically flagged as a potential hot spot despite the quieter outlook. And quieter seasons have produced devastating storms before — Andrew in 1992 and Michael in 2018 both hit during El Niño years. Andrew was a Category 5.

The forecast means fewer storms, not zero storms. And it only takes one to destroy a rental property portfolio that isn't documented.

Want the printable version? Download the 30-day hurricane countdown checklist — the same documentation protocol our property managers use for Orlando and Tampa rentals.

Why Do So Many Florida Hurricane Insurance Claims Get Denied?

Let's look at what actually happened in 2024. Across three hurricanes — Milton, Helene, and Debby — the denial patterns tell the same story:

- Hurricane Milton: 34.8% of 385,146 claims closed without payment

- Hurricane Helene: 60% closed without payment

- Hurricane Debby: 68% of residential claims closed without payment

According to Florida's Office of Insurance Regulation, the primary reasons aren't insurer misconduct. They break down into three categories:

Damage below the deductible (41% of Milton denials). Most Florida landlords don't realize their hurricane deductible is a percentage of their insured value — not a flat dollar amount. On a $400,000 property with a 2% deductible, you're paying the first $8,000 out of pocket. At 5%, that's $20,000. Many "denied" claims actually fall below this threshold.

Flood damage exclusions (4-20% depending on the storm). Standard landlord insurance policies exclude flood damage. Period. You need a separate flood insurance policy through the NFIP or a private insurer. If you're waiting until a storm forms to buy flood coverage, you're already too late — NFIP policies have a 30-day waiting period.

Not sure what your current policy covers? Our guide to landlord insurance in Florida breaks down exactly what standard policies include and what they don't — including the flood gap that catches most landlords off guard.

Other coverage issues (18-23%). This includes lapses in coverage, properties that exceed stated condition, and — here's the preventable one — insufficient documentation of pre-storm property condition.

Insufficient documentation isn't the biggest denial category. But it's the one you can fix for free, in an afternoon, with your phone.

What Insurance Documentation Should Florida Landlords Have Before a Storm?

The insurance industry calls it a "pre-loss inventory." Landlords who've been through a claim call it "the thing I wish I'd done before the storm."

Here's what a defensible pre-loss inventory looks like for a rental property:

Exterior documentation (15-20 minutes per property):

- Every wall of the building, photographed from 10-15 feet back

- The roof from four angles (use a drone, a second-story window, or just stand across the street)

- All windows, doors, the garage door, and the front entry

- Landscaping, trees, and drainage paths

- The HVAC condenser unit, any outdoor equipment

- The property address visible in at least one photo

Interior documentation (20-30 minutes per property):

- Every room, wide-angle from the doorway plus one closer shot

- Every major appliance — and shoot the serial number sticker on each one

- Flooring and ceiling condition (these are the first things damaged by water intrusion)

- Water heater, HVAC air handler, electrical panel

- Open closets and storage areas

The critical detail: Timestamps. Make sure your phone's location services and timestamp display are on. An adjuster needs to see that these photos predate the storm.

Upload everything to cloud storage — Google Drive, iCloud, Dropbox — so the documentation survives even if the property doesn't. Update annually before each hurricane season.

One more thing most landlords skip: tree maintenance documentation. Florida insurers are increasingly denying claims by arguing the landlord failed to maintain the property. A dated photo showing trimmed trees and clean gutters undercuts that argument before it starts.

How Do Hurricane Deductibles Actually Work in Florida?

This is the section that makes landlords angry — because most don't understand their deductible until they're filing a claim.

Florida hurricane deductibles are governed by FL Statute 627.701. Insurers must offer options of $500, 2%, 5%, or 10% of your dwelling coverage limit. For properties insured above $250,000, the $500 option typically isn't available.

Here's a real example. Say your Orlando rental is insured for $380,000 with a 2% hurricane deductible:

- Your deductible = $380,000 × 2% = $7,600

- If the storm causes $6,000 in damage, insurance pays nothing — you're below the deductible

- If the storm causes $15,000 in damage, insurance pays $7,400 — the amount above your deductible

At a 5% deductible on that same $380,000 property, you're eating the first $19,000 out of pocket.

One piece of good news: Florida law says you only pay one hurricane deductible per calendar year. If two storms hit in the same season, you don't pay twice.

The deductible activates when the National Hurricane Center issues a hurricane warning for any part of Florida and extends through 72 hours after the last warning is terminated. It only applies to declared hurricanes — not tropical storms or windstorms.

Know your number. Call your insurer this week and ask: "What is my hurricane deductible, in dollars, at my current coverage level?" Write it down. That number determines whether your claim is worth filing.

What Should You Do After the Storm? The Claims Checklist

The storm has passed. Now the clock is running. Here's the sequence that maximizes your chances of getting paid:

Within the first 24 hours:

- Document ALL damage before touching anything. Photos and video — wide angles for context, close-ups for detail. Timestamps on every shot.

- Make emergency repairs to prevent further damage. Tarp the roof. Board broken windows. Extract standing water. Mold starts growing within 24 hours of water intrusion. Keep every receipt — emergency mitigation costs are reimbursable through your insurance claim.

- Do NOT throw away damaged items. Pile them, photograph them, keep them until the adjuster arrives.

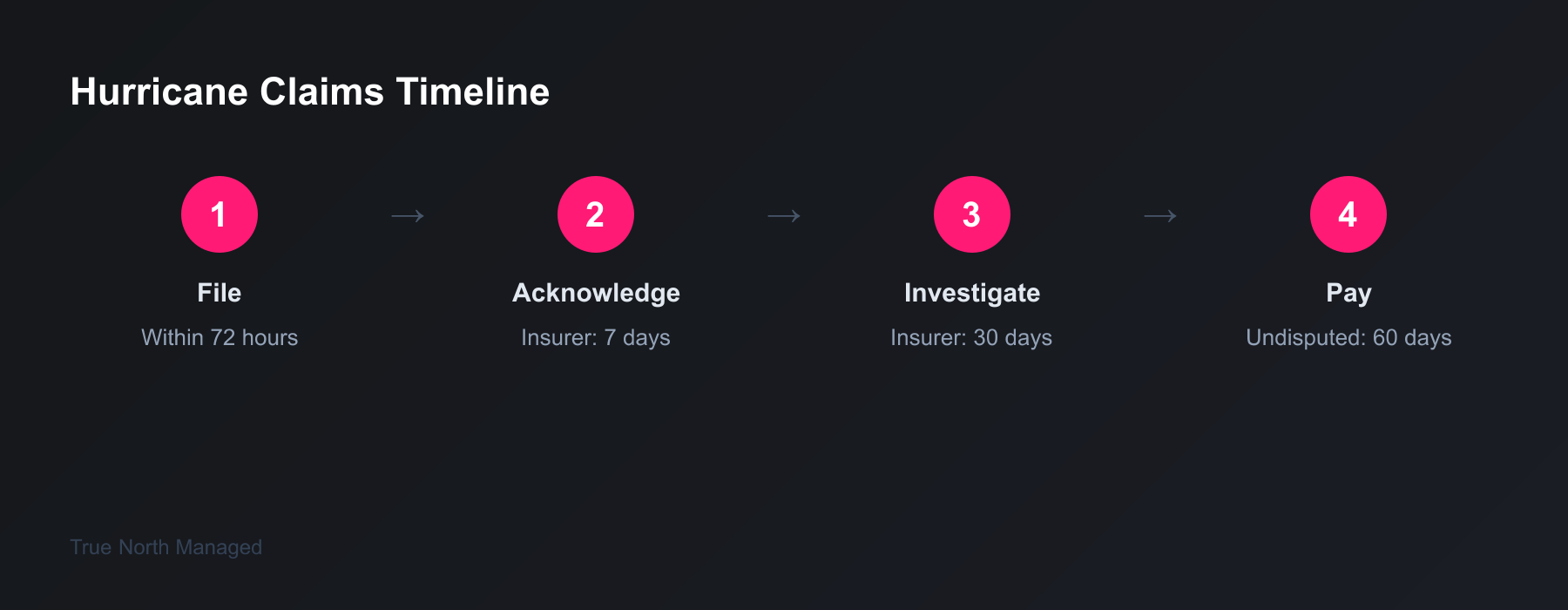

Within 72 hours: 4. File your claim directly with your insurance company — not through your agent. Under FL Statute 627.70132, you have 1 year from the date of loss for new claims and 18 months for supplemental claims. But waiting costs you money and attention.

Track the timeline:

- Insurer must acknowledge your claim within 7 days

- They must provide the Homeowner Claims Bill of Rights within 14 days

- They must investigate and respond within 30 days

- They must pay the undisputed portion within 60 days

If they miss any of these deadlines, document it. It matters if the dispute escalates.

If your claim is denied: Read the denial letter carefully. A surprising number of "denials" are actually "damage below deductible" — meaning your claim was legitimate but the damage didn't exceed your out-of-pocket threshold. That's different from a coverage exclusion.

For complex claims — especially those involving both wind and water damage, which insurers love to split into separate claims — consider hiring a licensed Florida public adjuster. They charge 10% of the settlement for emergency claims (the first year after a declared state of emergency). They work for you, not the insurance company.

One tenant-side note you can't ignore: FL Statute 83.63 gives tenants the right to terminate the lease if the premises are "substantially impaired" by casualty damage. If only part of the property is damaged, they can stay and pay reduced rent proportional to the usable space. Know this before the conversation happens — not after.

Tampa landlords dealing with flood zone properties should also check our Tampa Bay hurricane prep guide for basin-specific flood considerations and MacDill-area evacuation routes.

Your Pre-Season Action Plan

Hurricane season starts June 1, but preparation starts now — in March and April, while contractors are available and insurance changes can still take effect.

The full 30-day hurricane countdown checklist breaks this into a week-by-week timeline: insurance and documentation first (Days 30-14), property hardening second (Days 14-7), tenant communication last (Days 7-0). It's printable, checkbox-formatted, and includes the post-storm claims checklist on the back.

If you manage an Orlando or Tampa rental property and want a professional handling your hurricane prep — from pre-season inspections to post-storm insurance coordination — get a free rental analysis to see what that looks like for your specific property.