How Much Does It Cost to Become a Landlord in Florida?

What it actually costs to become a landlord in Florida — down payment, closing, make-ready, and the insurance bill that blindsides first-timers.

You ran the numbers. Down payment, closing costs, maybe a little for paint. The math worked. Then the landlord insurance quote came back, and suddenly it didn't.

That's the moment most first-time Florida landlords learn their pro forma was missing a line. The down payment was never the surprise. The surprise is everything that lands after it — and in Florida, the biggest piece of that is insurance.

Here's the honest answer up front. The cost to become a landlord in Florida is the national startup number plus a four-figure insurance reality. Budget the down payment and closing costs like you would anywhere. Then add roughly $6,000 to $12,000 more for make-ready, fees, and reserves — and know that a chunk of that exists only because this is Florida.

National "how much does it cost" articles skip this. They quote a generic insurance line ("about 25% more than a homeowners policy") and move on. Florida doesn't work that way. We have hurricane season, a separate hurricane deductible, and an insurance market that spent two years in crisis. Call it "The Insurance Surprise." It's the line item that wrecks a first-timer's spreadsheet, and it's the reason this post exists.

How much does it really cost to become a landlord in Florida?

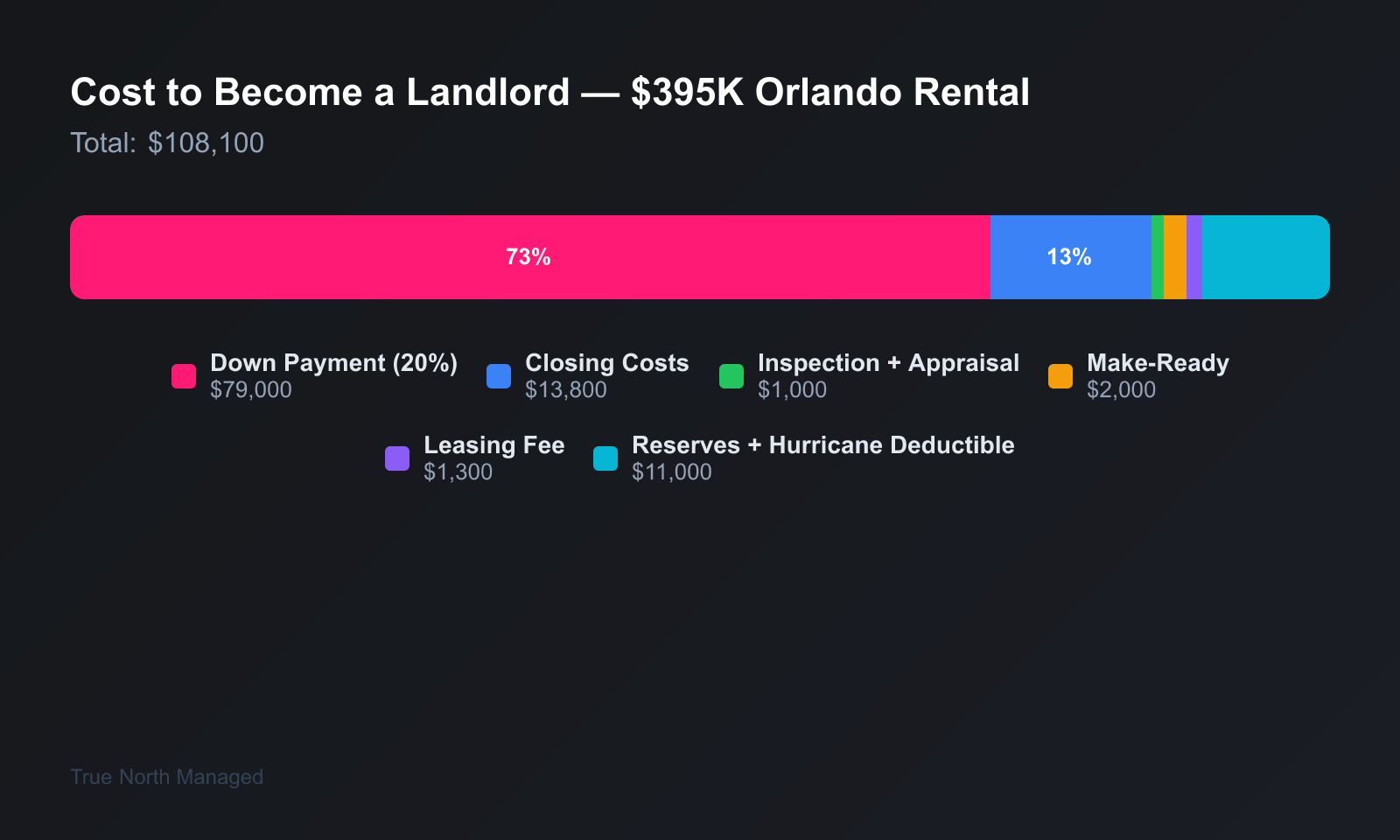

Becoming a landlord in Florida costs the property's down payment and closing costs — typically 17% to 30% of the purchase price combined — plus a separate $6,000 to $12,000-plus for make-ready work, leasing fees, and cash reserves. On a $395,000 Orlando home, that's roughly $75,000 to $130,000 in real money before your first rent check.

It helps to split the cost into two buckets.

One-time costs to open the door: the down payment, closing costs, inspection, getting the property rent-ready, and the leasing fee to land a tenant.

Day-one reserves: the cash you set aside before a tenant moves in — for repairs, vacancy, and the hurricane deductible. This bucket is the one new landlords skip, and it's the one Florida punishes you for skipping.

Let's price both.

What are the upfront costs to buy a Florida rental?

The upfront cost to buy a Florida rental is the down payment plus closing costs. Conventional lenders want 15% to 25% down on a non-owner-occupied single-family home, and Florida buyer closing costs run 2% to 5% of the purchase price. On a typical metro home, that's the largest check you'll write.

Start with the down payment. A rental isn't a primary residence, so the low-down-payment loan programs don't apply. Plan on 15% down with strong credit, 20% to 25% as the standard. On a $395,000 Orlando home — close to the Orlando Regional REALTOR Association's March 2026 metro median — 20% down is $79,000. A $420,000 Tampa single-family home at 20% is $84,000.

Closing costs come next. Florida buyers pay 2% to 5% of the purchase price, with 3% to 4% common — lender fees, title insurance, the state documentary stamp tax, prepaid taxes and insurance. On that $395,000 Orlando home, budget $11,850 to $15,800.

Then the small stuff that isn't small. A home inspection on a Florida single-family home runs $400 to $550. If the house is older, add a wind mitigation inspection ($75 to $150) and a four-point inspection ($75 to $200) — your insurer will likely require both. An appraisal is another $300 to $500. Realistically, $800 to $1,200 before you own anything.

Why is landlord insurance the line that wrecks a Florida pro forma?

Landlord insurance is the line that breaks a Florida pro forma because the premium is high and the hurricane deductible is separate. A landlord policy in Florida averages $2,200 to $2,800 a year — Florida ranks second-most-expensive in the country — and on top of that, a named-storm claim carries its own deductible of 2% to 10% of your home's insured value.

That hurricane deductible is the part nobody warns you about. Florida law (FS 627.701) requires insurers to offer hurricane deductibles of $500, 2%, 5%, or 10% of your dwelling limit — and for homes insured at $250,000 or more, the $500 option doesn't have to be offered. So your policy carries a percentage deductible. On a $350,000 dwelling, a 2% hurricane deductible is $7,000. That's $7,000 you pay before your insurer covers a dime of storm damage. It's not your regular deductible. It's a second one.

Where the property sits changes the number a lot. Inland Orlando rentals — most of the metro, with no coastal flood designation — land in the $1,000 to $3,000 range for landlord insurance. Tampa is a different story. Storm-surge zones in South Tampa and coastal Hillsborough push premiums to $4,000 to $5,800 for a $300,000 dwelling, and many of those properties need a separate flood insurance policy for the rental on top.

There's some good news for 2026. Florida's insurance market is finally settling. Citizens, the state-backed insurer, got approval for an 8.7% average statewide homeowners rate cut — the first real decrease since 2015 — and 17 new carriers entered the market. Rates are easing. But "easing" still means second-most-expensive in the nation. For a full breakdown of coverage and pricing, see our Florida landlord insurance guide.

Here's the part to internalize: the premium is an annual cost, but the hurricane deductible is a reserve you need in cash on day one. We'll come back to that.

What does it cost to get a Florida rental ready to lease?

Getting a Florida rental ready to lease costs $750 to $3,000 for make-ready work, plus a leasing fee of 50% to 100% of one month's rent if you place a tenant through a property manager, plus smaller setup costs. Most first-time landlords spend $2,000 to $5,000 here.

Make-ready is the work between closing and listing. An easy turn — deep clean, carpet cleaning, touch-up paint — runs $750 to $1,000. A full repaint with carpet replacement is closer to $2,500 to $3,000. Add a lock change for every exterior door ($50 to $300 total), because you don't know who the previous owner handed keys to.

Then there's getting a tenant in the door. A leasing or tenant-placement fee — marketing, showings, screening, lease prep — costs 50% to 100% of one month's rent, with Orlando managers commonly charging 50% to 75%. On a home renting for $2,050 a month, that's roughly $1,025 to $1,540. If you self-place, you still pay for tenant screening — background and credit checks run $30 to $50 per applicant.

A couple of smaller items. Holding the property in a Florida LLC costs $125 to file the Articles of Organization with the Division of Corporations, then $138.75 a year for the annual report — see our guide on putting a Florida rental in an LLC. And one cost that isn't a startup expense but belongs on your radar: property tax. A rental gets no homestead exemption, so it's assessed at full market value. New investors are routinely surprised by the bill — our Florida rental property tax guide walks through what to expect.

How much should you hold in reserve before your first tenant moves in?

You should hold three to six months of the property's expenses in reserve before your first tenant moves in — plus a separate cash reserve equal to your hurricane deductible. For a typical Orlando or Tampa rental, that's $8,000 to $15,000 sitting in an account doing nothing, and it isn't optional.

Reserves are the bucket new landlords treat as a "later" expense. It isn't later. The day you own a Florida rental, you own the risk that comes with it — a failed AC compressor in July, a tenant who breaks the lease, a roof claim after a storm. Common guidance is three to six months of rent or fixed costs per property. A practical floor is $5,000, built toward $10,000 to $15,000 as you go.

Here's the Florida-specific layer. Your hurricane deductible — that $7,000 on a $350,000 home — is money your insurer expects you to produce after a named storm before coverage kicks in. If a hurricane damages your rental in September and you don't have that $7,000 liquid, you can't start repairs, and you can't re-rent a damaged unit. So the reserve isn't a comfort cushion. It's the thing that keeps a bad month from becoming a lost year.

Hurricane season runs June 1 through November 30. If you're buying this spring, the deductible reserve needs to be funded before the season opens — not promised, funded.

What do first-time Florida landlords get wrong about startup costs?

First-time Florida landlords get startup costs wrong in three predictable ways — and each one shows up as a number that wasn't in the spreadsheet.

They budget the down payment and call it done. The down payment is the visible cost, so it gets all the attention. But closing costs, make-ready, the leasing fee, and reserves can add up to more than half the down payment again. Budget the second bucket, or it'll budget you.

They price insurance off a homeowners quote. A landlord policy — sometimes called a DP-3 — costs more than an owner-occupied homeowners policy, and the quote you got while house-shopping for yourself doesn't apply. Get an actual landlord insurance quote on the actual address before you close. The number can swing thousands of dollars between an inland Orlando home and a coastal Tampa one.

They skip the hurricane-deductible reserve. This is the one that hurts. A landlord with a thin reserve and a 5% deductible on a storm-damaged rental is a landlord who can't make repairs and can't collect rent. Fund the reserve before hurricane season, every year.

Becoming a landlord in Florida is a real investment, and the upfront number is bigger than most first-timers expect — but it's knowable. Price all of it, including the parts national guides leave out, and you walk in with eyes open. If you want a clear read on what your specific property could earn and what it'll cost to run, get a free rental analysis — it's the fastest way to turn a guess into a plan. For a wider walkthrough of getting started, our Florida Owner's Guide covers the next steps, and the first 30 days as a new landlord picks up right where this post leaves off.