Renting to Family in Florida: What to Put in Writing

Renting a Florida property to a relative? A written, at-market lease is what protects your tax deductions — here's exactly what to put in writing.

CALLOUT — What you must do: Before your relative moves in, put a written lease in place that charges fair market rent — within roughly 10% of true local comps. Save three to five comparable listings to prove the number. Below-market rent reclassifies the property as personal-use and quietly kills your rental deductions. The lease and the comps are your proof.

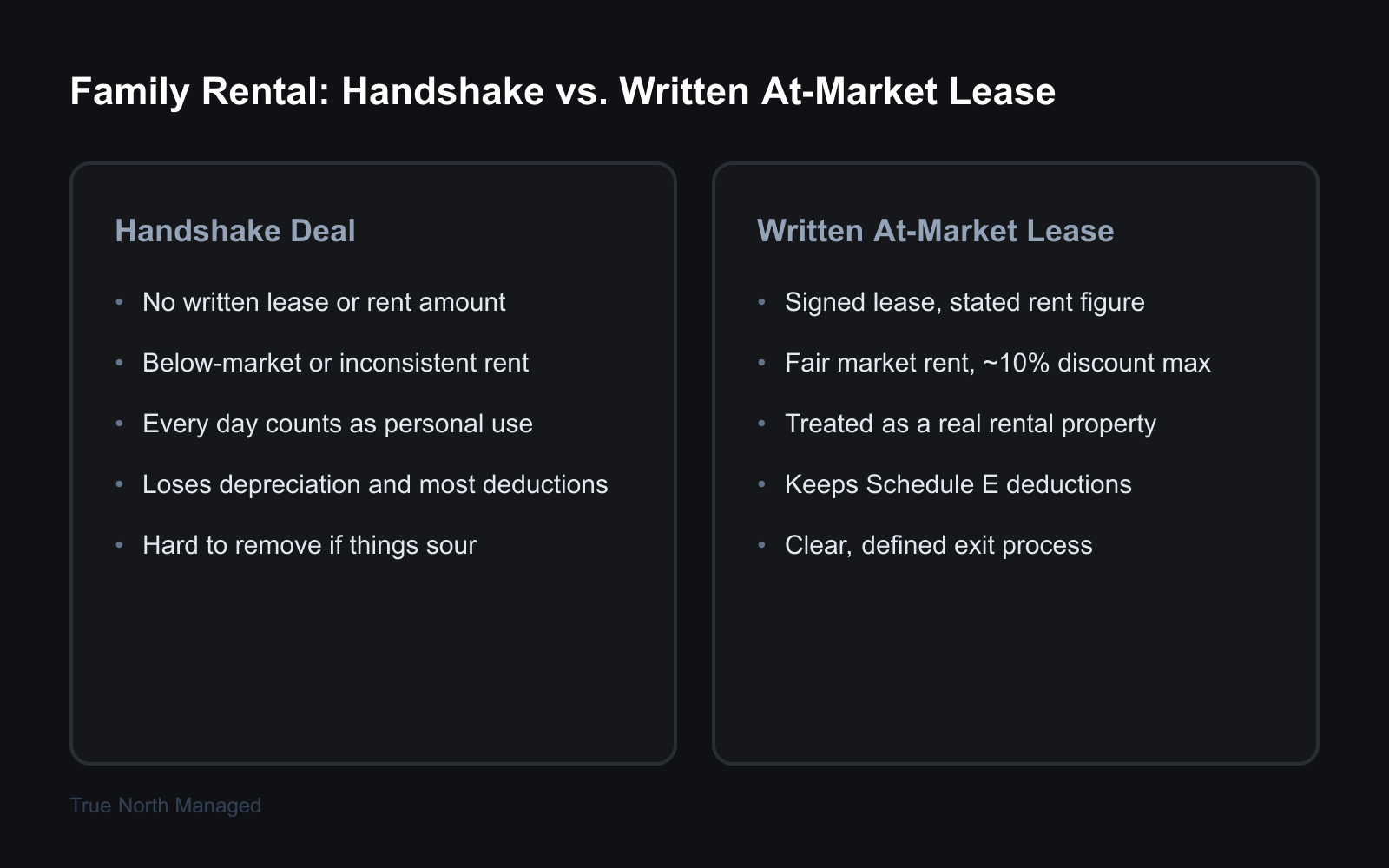

You're renting your spare house to your daughter. Or your mom is moving into the duplex you own in Brandon. Maybe a brother needs a place after a divorce, and you've got an empty rental in east Orlando. So you skip the lease. It feels strange to hand a family member a document and ask for a signature.

Here's the thing: with a family tenant, the lease isn't really about being able to evict your cousin. It's about protecting your taxes. Renting to a family member in Florida at the wrong rent — or with no lease at all — can reclassify your property in the eyes of the IRS and wipe out the deductions that make the rental worth owning. The written, at-market lease is the proof that keeps those deductions alive.

Let's break down what to put in writing, and why the paperwork matters more than you'd guess.

Why does renting to family change your taxes?

Renting to a relative changes your taxes because the IRS treats family use as personal use unless the relative makes the home their main residence and pays a fair rental price. Rent below market value turns every day they live there into a personal-use day — and enough personal-use days push the property out of rental classification entirely.

Call it "The Personal-Use Trap." It's the part nobody downloading a free lease template online ever hears about.

Under IRS Publication 527, a property you rent to a family member counts as personal use — the same as if you were living there yourself — unless two things are both true. The relative uses it as their main home. And they pay you a fair rental price. Miss either one, and the IRS doesn't see a rental anymore. It sees your second home that a relative happens to occupy.

Why does that distinction land so hard? Because the tax code limits personal use to 14 days a year (or 10% of the days the place is rented, whichever is greater) before a property loses its rental status. If your sister lives in your Orlando house all year at a sweetheart rent, every one of those 365 days counts as a personal-use day. You're not at 14. You're at 365. The property is no longer a rental for tax purposes — and it didn't take a tax audit to get there. It happened the day she moved in under a handshake.

What happens to your deductions if the rent is too low?

If your property gets reclassified as personal-use, you still owe tax on the rent your relative pays you — but you lose nearly every deduction that offsets it. Depreciation, repairs, insurance, lawn care, management fees: gone. Only mortgage interest and property tax survive, and they move off Schedule E onto Schedule A as itemized deductions.

That's a brutal trade. The rent is still income. The expenses mostly aren't deductible against it.

Here's what that looks like with real numbers. Say you own a single-family rental in Kissimmee. Market rent is $1,900 a month — right around the Orlando-area median, per Zillow's Orlando rental data. You rent it to your son for $1,100 because that's what he can afford.

As a proper rental at $1,900: You report $22,800 in rent, then deduct depreciation (roughly $7,000 a year on a typical Central Florida single-family), insurance, property tax, repairs, and more. Many landlords show a paper loss in the early years and owe little or no tax on the rental.

As a personal-use property at $1,100: You report $13,200 in rent as income. You deduct almost none of it. Depreciation — your biggest shelter — is off the table. The repair you made last spring? Not deductible. Your son's discount cost you the favor and a tax bill you didn't see coming.

The fix isn't complicated. Charge fair market rent, write it into a lease, and keep the records that prove the number. That last part — the proof — is exactly what the lease and a folder of comps give you. If you want the full picture on the deduction you're protecting, our Florida landlord's guide to rental property depreciation walks through how it works and why it's worth defending.

How much can you discount the rent for a family member?

You can give a family member a modest discount and still keep the property classified as a rental — most tax advisers treat about 10% below true market rent as a safe, defensible "good-tenant" discount. Some have argued for up to 20%. But 20% is risky, and you'd better be able to prove every dollar of it.

The 10% figure isn't arbitrary. The reasoning is that a reliable family tenant saves you real costs — no vacancy between tenants, no turnover painting, no leasing fee, fewer late-night maintenance surprises — so a small discount reflects a genuinely lower-cost tenancy, not a gift.

The 20% number has a cautionary tale attached. In Bindseil v. Commissioner, a landlord rented to his parents below market on the theory that they'd take unusually good care of the place and cover certain costs themselves. The IRS's own expert conceded a 20% discount could be reasonable in some cases. And the landlord still lost — because he couldn't actually prove that the reduced rent plus the parents' contributions added up to fair value. That's the whole lesson. A discount only protects you if it's documented. An undocumented discount is just a below-market rental waiting to be reclassified.

So on that $1,900 Kissimmee house, a defensible family rent is somewhere around $1,710 — roughly 10% off — written into a lease, with comps in the file. Not $1,100 on a handshake.

How do you prove the rent is fair market value?

You prove fair market rent the way the IRS, courts, and insurers all accept it: with comparable rentals. Pull three to five active listings for similar properties in the same area, average the rents, and keep dated copies. That folder is your defense if the rent is ever questioned.

One comp isn't enough. The IRS's own recordkeeping guidance is clear that you need records that support what's on your return — and a single listing is easy to pick apart. Three to five similar properties, averaged, is credible evidence.

Here's how to build the file:

- Find true comparables. Same city or submarket, similar bedroom and bathroom count, similar size and condition. A Winter Park three-bedroom doesn't prove the rent on a Brandon three-bedroom.

- Screenshot the listings with the date visible. Zillow, Apartments.com, your county's rental sites — anything showing what comparable homes actually ask.

- Average them. Add the rents, divide by the number of comps. That's your fair market rent. Apply your good-tenant discount from there if you're giving one.

- Re-pull every year at renewal. Rents move. Tampa apartment rents are down about 2% over the past year and Orlando's down around 3%, per RentCafe — small shifts, but a three-year-old comp file is a stale one. Refresh it when the lease renews.

Keep that folder with your lease and your tax records. If nobody ever asks, you've lost an afternoon. If someone does ask, you've kept your deductions.

Does Florida landlord-tenant law still apply to family?

Yes — completely. The moment a relative pays you rent to live in your property, they're a tenant under Chapter 83 of the Florida Statutes, the same as any stranger off Zillow. There's no family exception. That cuts both ways, and it's the second reason the lease matters.

It matters on the way in: a Florida residential lease still needs its required disclosures even when the tenant is your brother. Landlord identity, the radon disclosure, lead-based paint for a pre-1978 home, and — for any lease of a year or longer — the flood disclosure that took effect October 1, 2025. Our guide to required Florida lease clauses covers the full list. Skipping them because "it's family" doesn't make them optional. Our breakdown of the documents every new Florida landlord needs before listing covers each disclosure in full, family lease or not.

And it matters if things go sideways. If your relative stops paying and you need them out, you can't change the locks or shut off the power — self-help eviction is illegal in Florida, family or not. You'd serve the proper notice and, if needed, file in county court, just like any eviction. A relative paying rent on a month-to-month basis is owed 30 days' written notice to end the tenancy under Florida Statute 83.57. A clear lease with a defined term and a written exit process — see our guide to early lease termination in Florida — makes a hard conversation a lot less ugly.

Two more Florida wrinkles. If you currently hold a homestead exemption on the property, renting it out — to anyone, including family — for more than 30 days in two consecutive years can cost you that exemption, so check with your county property appraiser first. And if you hold the rental in an LLC, the family lease should name the LLC as landlord; our LLC for rental property guide explains why that consistency matters. If a family rental is also your first rental, our guide to the cost of becoming a landlord in Florida lays out the startup numbers worth running first.

What should the family lease actually say?

A family lease should say everything a normal Florida lease says — it just has one extra job: documenting that the rent is at fair market value. Treat it as a real lease, not a courtesy. The whole point is that it reads like an arm's-length agreement, because for tax purposes it has to be one.

Put these in writing:

- The rent amount, and how you set it. State the monthly rent. Keep your comp file attached or referenced. If you're applying a good-tenant discount, the comps show the discount is modest.

- The lease term and renewal. A real start and end date. Month-to-month is fine, but pick a structure and write it down.

- Who pays what. Utilities, lawn care, pest control, HOA dues. Spell it out so a "favor" doesn't quietly drift into you covering costs that undercut the at-market rent.

- The four required Florida disclosures. Landlord/agent identity, radon, lead paint for pre-1978 homes, flood disclosure for leases of a year or more.

- Security deposit handling. How much, where it's held, the return process. Yes — even with family.

- Maintenance and repair responsibilities. Who calls who, and who pays.

- The exit terms. How either side ends the lease, and the notice required.

Sign it. Date it. Have your relative actually pay the rent — by check or transfer, on the first, every month. A lease that says $1,710 while $600 actually changes hands isn't a lease. It's a below-market rental with extra steps.

What do landlords get wrong renting to family?

The mistakes that cost Florida landlords money here aren't dramatic. They're small, comfortable shortcuts that feel kind in the moment.

1. No lease at all. "It's my daughter, we don't need paperwork." But with no lease and no documented rent, you've handed the IRS a personal-use property and handed yourself a removal headache if the living situation ever sours. The lease protects the relationship as much as the deductions — everyone knows the terms.

2. Vague or inconsistent rent. "Pay me when you can." Erratic payments and an unstated rent amount look exactly like a gift, not a rental. Pick a number, write it down, collect it on a schedule.

3. Treating it as a favor instead of a rental. This is the big one. The instinct is generosity — charge little, skip the comps, keep it casual. But casual is what triggers the reclassification. You can absolutely be generous: give the 10% good-tenant discount, be patient, be flexible on small things. Just do it inside a documented, at-market lease.

The bottom line

Renting to family in Florida can work well — a reliable tenant you trust, a relative in a stable home. The trap is treating it as a favor instead of a rental. Charge fair market rent, give a modest documented discount if you want to, write a real lease, keep your comps, and follow the same Florida rules you'd follow for any tenant. Do that, and you keep your deductions and your relationship. If you're new to all of this, our Florida owner's guide is a good place to get your footing.

If you're not sure what fair market rent is for your property — or you'd rather not be the one chasing your brother for the check — that's exactly the kind of thing we help with. Our free rental analysis includes a real look at comparable rents in your Orlando or Tampa neighborhood, so the number in your family lease is one you can stand behind. No pressure — just a clear figure and a clear picture.