Tampa Rental Market Update — June 2026

The Two Tampas split hasn't moved much this month — but the calendar did. Hurricane season opens June 1, mortgage rates just ticked back up, and Citizens insurance rate cuts land July 1. Here's what to do this month.

There are still two rental markets in Tampa — the apartment market and the single-family market, moving in opposite directions. We covered that split last month and called it "The Two Tampas." The numbers haven't moved much in 30 days. What moved is the calendar.

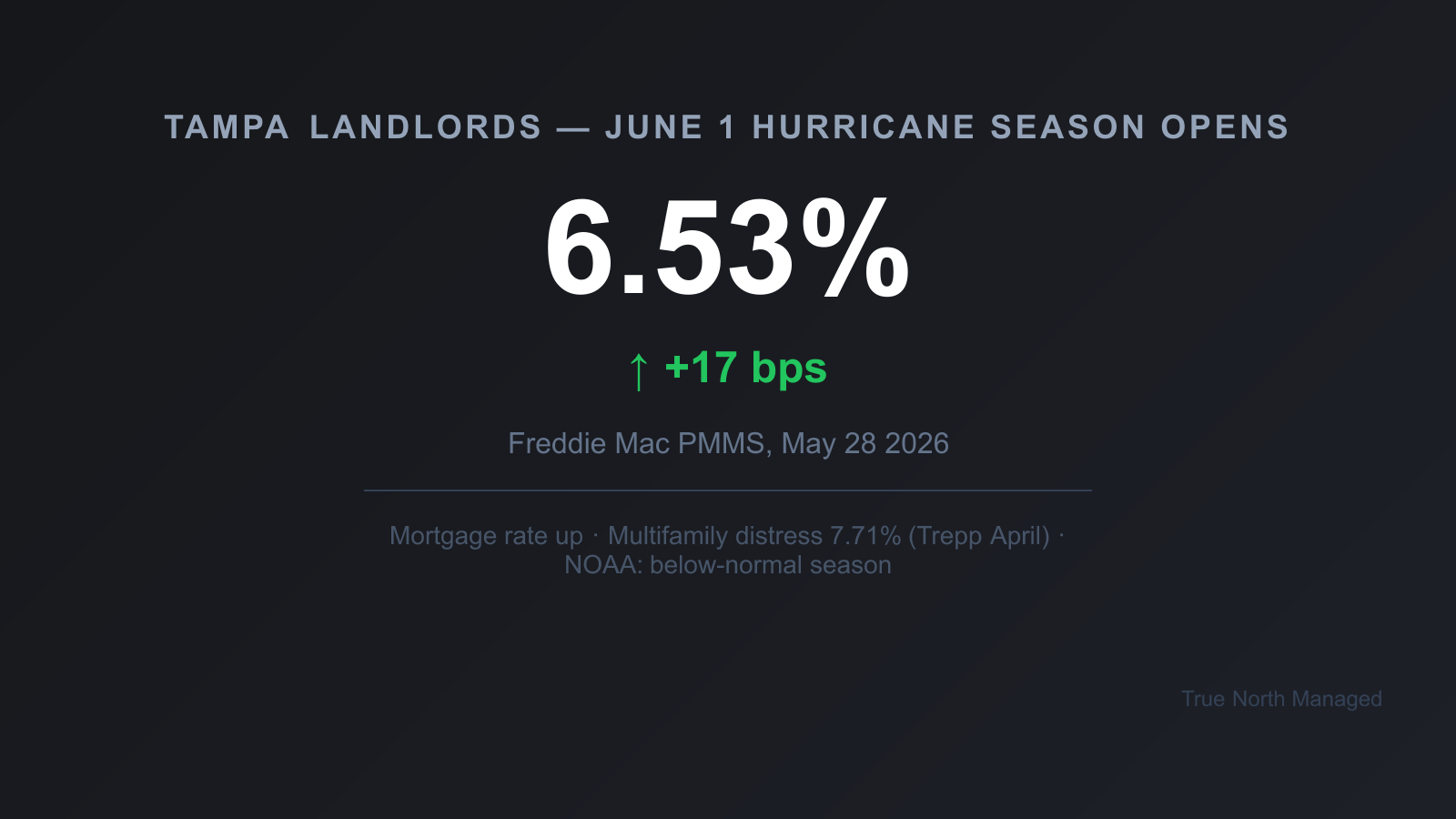

June 1 brings two things at once. Hurricane season opens, and the 30-year mortgage rate ticked back down — 6.48% on Freddie Mac's June 4 print, off the 6.53% late-May high. A third date matters too, but it's July 1, not June 1: Florida Citizens' approved personal-lines rate cuts take effect then. This update is less about a new rent print and more about what you should actually do over the next four weeks.

What changed in Tampa's rental market this June?

The split is the same. Apartment vacancy in Tampa is still around 10.7%, the highest CoStar has tracked since 2000, and apartment effective rents are still down roughly 5.4% year-over-year per RealPage. Single-family rents are still holding up — nationally Zillow had single-family rents up 2.5% in March against just 1.3% for multifamily. Same divergence, same neighborhoods carrying it in Tampa: Seminole Heights, Hyde Park, Palma Ceia.

What's new since last month's update isn't a number on a chart. It's the calendar pulling forward. June 1 reaches every Tampa landlord whether you rent a house or a sixplex. July 1 reaches your insurance bill. And a small mortgage move in the past two weeks sharpens the buyer story for anyone watching small-multi prices.

What does June 1 actually mean for Tampa landlords this year?

Three June 1 drivers, plus a fourth that lands July 1.

Hurricane season opens June 1. NOAA's 2026 Atlantic Hurricane Outlook, released May 22, calls for a below-normal season — 8 to 14 named storms, 3 to 6 hurricanes, 1 to 3 major hurricanes. Below-normal is comforting. It isn't a permission slip. Ian hit in what was considered an average season. June is the prep month, not the storm month — which means the work to do happens now, while you have a calm weekend.

Mortgage rates backed off. Freddie Mac's Primary Mortgage Market Survey had the 30-year fixed at 6.36% on May 14, 6.51% on May 21, and 6.53% on May 28 — its spring high — then back down to 6.48% on June 4. Not a regime change, and the brief climb has already unwound. But rates parked near 6.5% still make the distress story sharper.

Distress data moved. Trepp's April print on multifamily CMBS delinquency came in at 7.71%, up 56 basis points from six months ago. MSCI expects 60% of apartment loans originated in 2021–2022 to mature in the second half of 2026. Those were 4–5% loans. Refinancing them at 6.5%+ doesn't pencil on buildings underwritten to old cap rates. Tampa keeps getting named as a Sun Belt distress metro in those analyses.

The July 1 piece is its own thing. Florida Citizens' OIR-approved 2026 personal-lines rates take effect for new policies on July 1: a multiperil average of −8.8%, wind-only average −5.5%, with a minimum decrease of 2% across all personal lines. Existing policies reprice at renewal after that. Citizens' commercial-residential rates rise July 1 — multiperil ~7.2%, wind-only ~14.4% — and that's the bill small-multifamily owners feel. June is when you get ahead of both.

What does the June calendar mean for your Tampa house?

The 10.7% vacancy headline is an apartment number. It isn't your house. Single-family rentals in established Tampa neighborhoods are still moving — a well-priced house leases in about three weeks, an overpriced one sits. That part of the story we covered last month, and the comps haven't shifted.

What June changes is what's around your house. Storm risk reaches every Tampa landlord regardless of property type. And rent expectations don't form in a vacuum — your applicant has been shopping apartment towers running concessions all spring. They expect a deal. You're not competing on price with a tower throwing one month free. You shouldn't try to. But the renter walking through your door doesn't separate the two markets the way you do.

For small-multi owners specifically: the Citizens commercial-residential increase (multiperil ~7.2%, wind-only ~14.4%) lands on your renewal next quarter. That bill is real. Plan for it now, not in September. Pull the current FEMA panels for your address while you're at it — and if you don't already have a current policy, flood insurance for Florida rentals walks through what a landlord-side policy actually has to cover.

What should Tampa landlords do this June?

Three moves. Each tied to a date you already know.

Hurricane prep before June 1. Walk every room with your phone. Date-stamped photo or video of every wall, every floor, every appliance. Vendor list saved in two places — a tarp roofer, a tree service, a water mitigation company you've actually called. Insurance declaration page in a digital folder you can access from a hotel parking lot if you have to. If you own from out of state, this is the move that matters most for you — you can't drive over to check shutters, so the digital folder and a written hurricane-comms plan for your tenant carry the work you'd normally do in person. NOAA's below-normal call is good news, not a permission slip to skip the work.

Document for July 1 — both Citizens letters. Personal-lines policies will reprice down at renewal once the new July 1 rates apply — multiperil average −8.8%, wind-only −5.5%, minimum −2%. Averages hide spread, so when your renewal arrives, read the wind premium row against last year and check your roof-age multiplier. Pull your current declarations page now. Photograph any mitigation features that earn discounts — storm shutters, roof straps, a roof under ten years, hip-roof shape — so your renewal is priced against what you actually have. If you own from out of state, ask your property manager for a dated photo set of those mitigation features now — you can't photograph the roof straps yourself, and your renewal is priced on what's documented. Small-multi owners on a Citizens commercial policy: call your broker for an alternative quote this month, before the commercial-residential increase (approved at ~7.2% multiperil / ~14.4% wind-only) takes effect July 1.

Read the distress data before the headlines. Apartment foreclosure activity is climbing into the second half of 2026. For most readers — owners of one Tampa house — that's noise that affects the city, not your asset. For small-multi buyers, that's deal flow forming. The right opportunity in this market is a sponsor with a 2021 bridge loan they can't refinance, not a Zillow search. If you're a single-family owner wondering whether to sell, fundamentals haven't broken. Rent growth is intact, vacancy on SFH is low, the sale market is balanced — the signals that would actually justify selling aren't flashing yet.

The thread through all three: June isn't about a new number on a chart. It's about a calendar pulling two real deadlines into the same four weeks. Paper your hurricane prep before the season opens, get your insurance documentation in order before the July 1 rates land, and price to what houses actually do. If you'd like a clear read on what your Tampa house should rent for this June, our team's Free Rental Analysis lays it out, comp by comp. You can also browse the rest of our Tampa property management resources for more on managing through this market.