Tampa Flood-Zone Rental: From Uninsurable to Leased

A Riverview owner had a paid-off home in a FEMA flood zone sitting vacant for four months. Here's how a Tampa flood zone rental went from uninsurable headache to a stable lease.

A Riverview owner called us with a problem that's getting more common around Tampa. He owned a paid-off three-bedroom house near the Alafia River, he'd relocated to North Carolina for work, and the place had sat empty for four months. Every prospect who asked about flood insurance walked. And he'd just heard there was a new Florida law about telling tenants the home floods.

He wasn't wrong to be nervous. But almost everything scaring him was fixable.

What was wrong with this Riverview flood-zone rental?

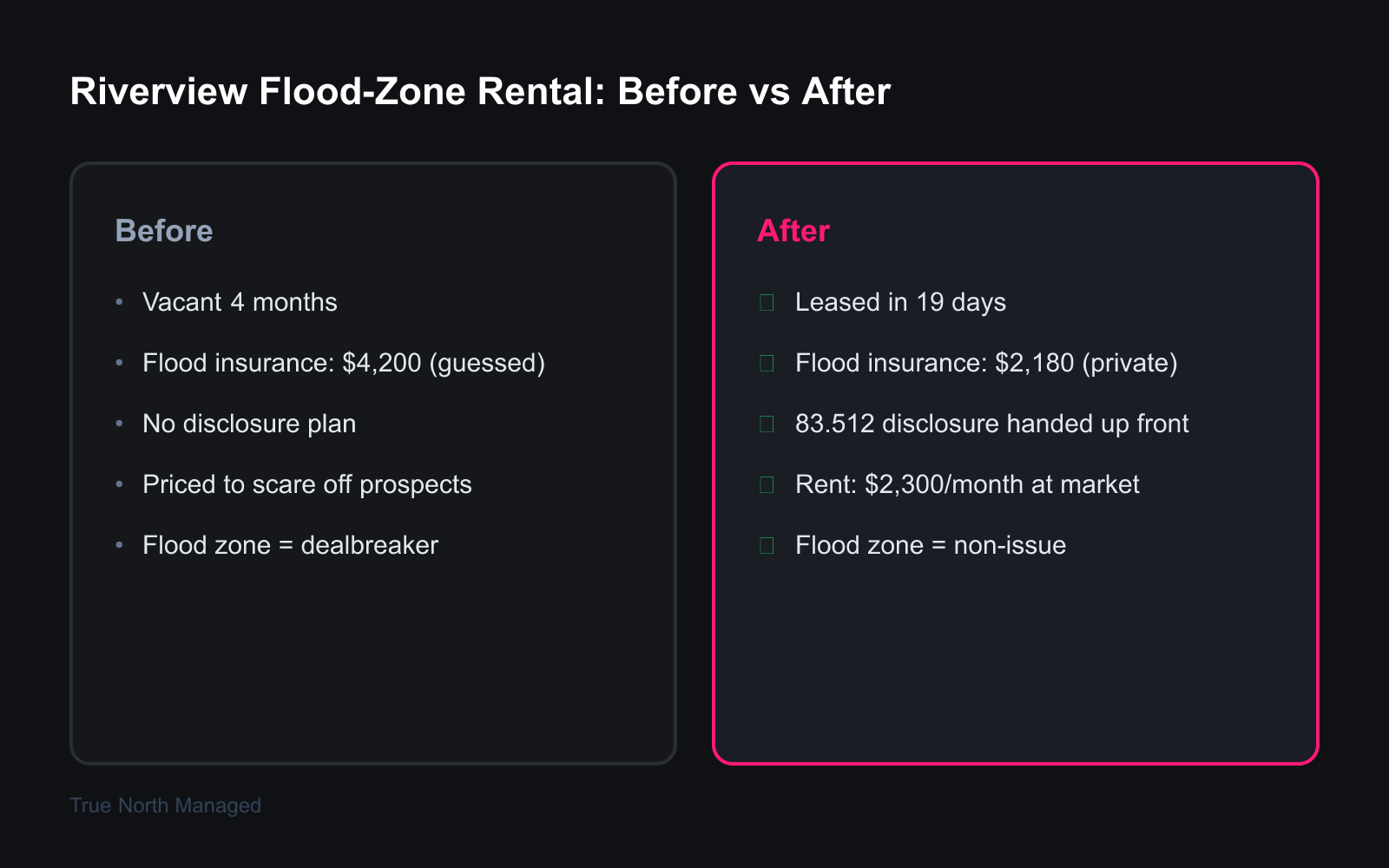

A paid-off Riverview home in a FEMA AE flood zone had been vacant four months. The owner was quoting prospects a $4,200 flood-insurance number he'd guessed at, didn't have a disclosure plan for the new state law, and had the rent priced where nobody would touch it. Three separate problems, all solvable.

Here are the specs. Three-bed, two-bath single-family, about 1,650 square feet, built in the early 2000s, on a street off Bell Shoals Road in Riverview. Paid off. The owner moved to Charlotte, decided to rent rather than sell, and listed it himself.

The Alafia River is the whole story here. When Hurricane Helene and then Milton came through in the fall of 2024, the river crested near record levels and put several feet of water into homes along its banks. Hillsborough County ran more than 700 water rescues. So when a prospect Googles the address and sees flood headlines, they get cautious. Fair enough.

The owner's instinct was to bury the flood issue and hope nobody asked. That instinct is exactly backwards, and it was costing him about $9,200 in lost rent across four vacant months.

Do landlords need flood insurance on a Tampa rental, and what does it cost?

Yes. A standard landlord policy — the DP-3 dwelling-fire form most Florida investors carry — flat-out excludes flood. Flood is always a separate policy. Through the National Flood Insurance Program, building coverage tops out at $250,000 and that covers the structure only, not a tenant's belongings.

The first thing we did was stop guessing. The owner's $4,200 number came from a quote he half-remembered. So we pulled the actual flood map at the FEMA Flood Map Service Center, confirmed the home sat in Zone AE — a high-risk Special Flood Hazard Area with a Base Flood Elevation on file — and then ordered an elevation certificate.

That certificate earned its keep. It showed the finished floor sitting about 1.5 feet above the Base Flood Elevation, which FEMA's default model hadn't captured. Under Risk Rating 2.0, elevation above BFE drops the premium, and on this house it dropped it a lot. The re-rated NFIP quote came in at $2,640 a year.

Then we shopped it. Private flood carriers often beat NFIP on a favorable-risk property, and one bound the same coverage at $2,180. So the "uninsurable" $4,200 headache became a real, quotable $2,180 line item — about half of what the owner had been scaring people with.

One more piece we sorted out: the building policy is the owner's. It does nothing for the tenant's couch, clothes, or TV. We made sure the lease pointed the tenant to a renter's contents flood policy of their own, which NFIP covers up to $100,000. Our Florida flood insurance guide for rentals breaks down that building-versus-contents split in full.

How does Florida's flood-disclosure law affect renting a flood-zone home?

Florida Statute 83.512 took effect October 1, 2025. It requires a landlord to give a prospective tenant a flood disclosure — in a separate document, not buried in the lease — at or before signing any lease of one year or longer. You disclose three things from your time owning the home: whether it flooded, whether you filed a flood-damage claim, and whether you got flood-damage assistance, FEMA included.

Skip it and the math gets ugly. If you don't disclose and the tenant later suffers a "substantial loss" from flooding — the statute defines that as repair or replacement costs hitting 50% or more of the value of the tenant's personal property — the tenant can terminate the lease with written notice within 30 days of the damage and walk with a refund of prepaid rent. You can read the full text on the Florida Legislature's site, and our Florida flood-disclosure guide for landlords walks through the form itself.

So we built the disclosure document and filled it in honestly. On this specific structure, there was nothing to report — no prior-ownership flooding, no claims, no assistance — because the home, sitting above BFE, hadn't taken water even in 2024. We handed that to every applicant up front.

That changed the conversation. Instead of dodging the flood question, the owner was the guy handing over a clean disclosure, a flood map, and a bound insurance policy. Disclosure stopped being a liability and started being a trust signal.

What did the turnaround actually achieve?

The house leased in 19 days after sitting empty for four months. Rent landed at $2,300 a month, right in line with Riverview's three-bedroom range. Flood insurance dropped from the owner's $4,200 guess to a bound $2,180 policy. The flood zone stopped being a dealbreaker the moment we stopped hiding it.

A timing note worth knowing: NFIP policies carry a 30-day waiting period before coverage starts, so we bound the flood policy early — well before a tenant moved in — instead of scrambling at lease signing. You don't want a gap on a flood-zone property during hurricane season.

The owner had been treating a manageable cost like a fatal flaw. Priced right, insured right, and disclosed right, his "unrentable" Riverview house rents like any other Riverview house.

What can other flood-zone landlords learn?

Don't guess your flood premium, don't price around your fear of the flood zone, and don't hide the zone from tenants. Call it "The Flood-Zone Discount Trap" — the owner who slashes rent and skips insurance because he assumes the flood label kills demand, when the real fix is information.

A few things that actually move the needle:

- Pull your real FEMA map and get an elevation certificate. The default flood model is often pessimistic, and being a foot or two above Base Flood Elevation can cut your premium meaningfully.

- Shop NFIP against private flood every renewal. They price risk differently, and the gap on a single house was over $2,000 a year here.

- Comply with Statute 83.512 and treat the disclosure as a feature, not a confession. Tenants trust the landlord who's straight with them.

Flood-zone properties around Tampa aren't broken investments. They're properties that need the numbers run correctly. See the Tampa property management guide for how we approach the rest of Hillsborough's submarkets.

Got a flood-zone rental that's costing you more than it should? Get a free rental analysis and we'll run the insurance, pricing, and disclosure side by side.

Property Specs and Timeline

3-bed, 2-bath single-family, Riverview (East Hillsborough), ~1,650 sq ft, built early 2000s, paid off. FEMA Zone AE, ~1.5 ft above Base Flood Elevation. Owner relocated out of state. Month 1: pulled FEMA map, ordered elevation certificate, re-rated and shopped flood insurance ($4,200 guess → $2,640 NFIP → $2,180 private). Month 1: built the 83.512 flood-disclosure document, repriced to market. Leased in 19 days at $2,300/month after four months vacant.