How to Price a Florida Rental in a Softening Market

In a softening market, the wrong rent number costs more than most Florida landlords realize. Here's how to price a rental so it leases fast and protects your bottom line.

You've got a house coming vacant, the market feels softer than it did last year, and you're staring at a number wondering if it's too high. Set it wrong and you'll find out the slow, expensive way — week after week of no applications.

Here's the short answer. In a softening market, you price to what comparable houses actually leased for in the last six months — not last year's rent, not the Zillow estimate. Price a little ahead of the softening and your house sits empty. Price it at the real market and a good house rents in a few weeks. The cost of guessing high is bigger than almost every landlord thinks, and that's what this guide is really about.

Why pricing is harder in 2026

Florida's rental market has cooled. Apartment rents in Orlando are down around 3% over the past year, and Tampa's are down closer to 5% — you can read the detail in our Orlando market update and Tampa market update for May 2026. Roughly 40% of apartment complexes are running move-in specials.

Single-family homes are holding up better — Cotality's Single-Family Rent Index shows house rents still rising nationally, and the National Association of Realtors reports detached homes outpacing apartments by a wide margin. But "holding up" isn't "ignore the market." Tenants have more choices than they did two years ago, and they're comparing. The mistake that cost you a slow week in 2023 costs you a slow month now.

What does a softening market actually mean for your rent?

A softening market doesn't mean slash your rent. It means the market has lost its patience for an optimistic number. In a hot market, an overpriced house still rents — it just takes a little longer. In a soft market, an overpriced house doesn't rent at all until you fix the price.

The signal to watch is showing activity in the first ten days. A correctly priced Florida house generates steady inquiries and at least one application inside two weeks. If your listing has been up for ten days with thin interest, the market is telling you something, and it isn't "wait longer." It's "the number is wrong." The longer you argue with that feedback, the more an empty house costs you — which brings us to the math that should drive every pricing decision.

How do you find the right rent number?

You build a rent comparison — the same comparative market analysis a good agent runs, scaled to one house. Pull three to five homes in your area that actually leased in the last six months, matched as closely as you can on bedrooms, bathrooms, square footage, and condition. Average them. That average is your anchor.

The method:

- Find recently leased comps — not active listings. An active listing is an asking price; a leased comp is a real one. Your MLS, a property manager, or rental sites will show you both.

- Match the basics: same bed and bath count, similar size, same school zone or neighborhood.

- Adjust for the gaps. A renovated kitchen or a fenced yard earns a premium over a comp without them. Dated finishes or no garage means a discount.

- Take the average, and note the high and low so you know your range.

Example. Say four similar three-bedroom homes near yours leased between January and April for $2,150, $2,225, $2,100, and $2,275. The average is about $2,190. Your house has a newer kitchen but a smaller yard, so you land near the middle — call it $2,200. That is a defensible number. "$2,400 because that's what I need to cover my new mortgage payment" is not.

One warning: don't lean on an automated estimate alone. A Zestimate or similar tool is a starting point, and in a market that's actively softening, those tools lag — they're reading yesterday's prices. Use them as a sanity check, never as the decision. For deeper local comps, our neighborhood pricing breakdowns for Orlando rentals and Tampa rentals walk through it street by street.

What does an empty month really cost? The Empty-Month Math

Here's the calculation most landlords get wrong, and it's the heart of pricing well. Call it "The Empty-Month Math."

Formula: True cost of a vacant month = lost rent + your carrying costs (mortgage, taxes, insurance, utilities while empty) + the share of turnover and marketing you'll spend re-leasing.

Example. Your house should rent for about $2,200. You decide to "try" $2,350 instead. It sits. One extra month empty costs you the $2,200 in rent you didn't collect, plus roughly $250 in utilities and lawn care you cover on an empty house — call it $2,450 for that month. Industry estimates put the all-in cost of a 30-day vacancy at 1.5 to 2 times a month's rent once turnover and marketing are added.

Now compare. To chase that extra $150 a month, you'd need the house to rent at $2,350 for 16 straight months just to break even against a single empty month at $2,200. Most landlords never get there — the lease turns over first. The optimistic price doesn't earn you more. It quietly costs you a month's rent to learn the comps were right.

What's good or bad? A Florida single-family home priced at the real market should lease within two to four weeks. Sitting past 30 days is a clear sign the price is too high — not that the right tenant "hasn't come along." There is no right tenant at the wrong price.

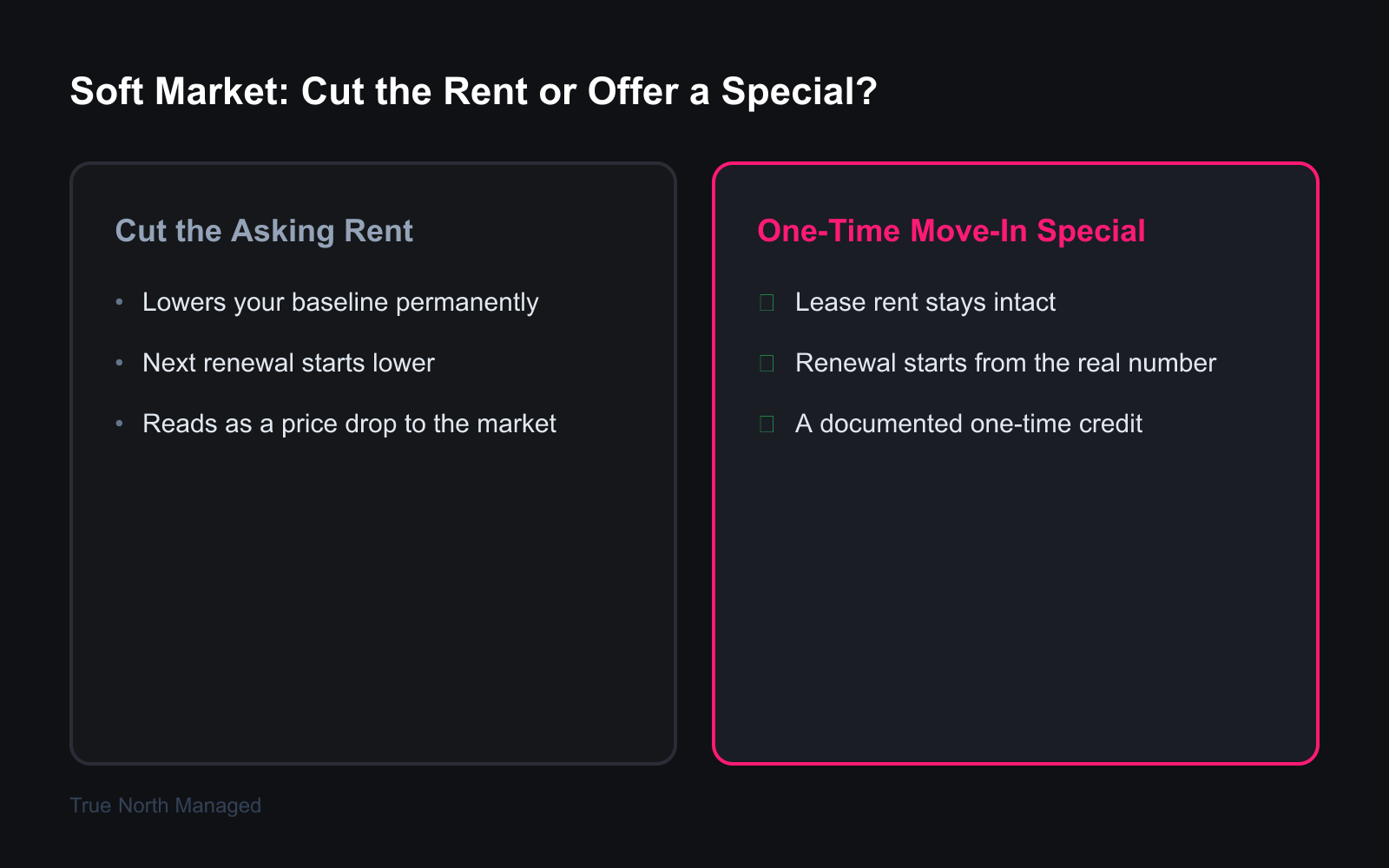

Should you cut the rent or offer a move-in special?

If your house has sat too long, you have two levers, and they are not equal. You can cut the asking rent, or you can hold the rent and offer a one-time move-in special — a half-month credit, a waived fee, covered move-in costs.

In a softening market, the move-in special is usually the smarter lever, and here's why: it protects your renewal number. Cut the rent from $2,200 to $2,050 and you've reset your baseline — next year's renewal starts from $2,050. Offer two weeks free instead and your lease still says $2,200; you gave up about $1,100 once, but the renewal conversation starts from the real number.

The net-effective-rent math is worth knowing. One free month on a 12-month lease is an 8.3% discount spread across the year. A half-month credit is closer to 4%. Keep concessions modest — around 10% of a month's rent or less — and never stack three of them; the goal is to win the lease, not give the house away. And put the special in a written lease addendum, not a handshake. In Florida, a clearly documented move-in concession prevents a deposit or renewal dispute later.

How often should you reprice?

Reprice at every turnover, without exception — pull fresh comps before you relist, because a number that was right 14 months ago is a guess today. Between turnovers, check the market once before each renewal offer so you're not raising rent into a market that's falling, or leaving money on the table in one that's rising. Our guide on when to raise rent in Florida covers the renewal side in full. The point is simple: pricing is a habit, not a one-time decision.

Common pricing mistakes Florida landlords make

- Pricing from need, not the market. Your mortgage, your taxes, and your target return are real — but the tenant doesn't see your spreadsheet. The market sets the rent; your job is to read it accurately.

- Trusting the automated estimate. Online estimates lag a softening market by months. They're a sanity check, not an answer.

- Ignoring the first two weeks. Showing feedback is data. Thin interest after ten days isn't bad luck — it's a price signal. Adjust early, while one week is the cost, instead of late, when a month is.

Frequently asked questions

How do I know if my rental is overpriced? The clearest sign is time. A correctly priced Florida single-family home draws steady inquiries and at least one application within two weeks. If your listing has been live for 10 to 14 days with little interest, it's overpriced — regardless of what comparable asking prices suggest.

How much does one vacant month actually cost a landlord? More than one month's rent. Beyond the lost rent, you still cover the mortgage, taxes, insurance, and utilities on an empty house, plus turnover and marketing costs. Industry estimates put the all-in cost of a 30-day vacancy at 1.5 to 2 times the monthly rent.

Should I lower the rent or offer a move-in special? In a soft market, a one-time move-in special (a half-month credit or waived fee) is usually better than cutting the asking rent. It leases the house while protecting your renewal number — a rent cut permanently resets your baseline.

How do I find rent comps for my property? Pull three to five similar homes — same bedrooms, bathrooms, size, and area — that actually leased in the last six months. Average their rents, then adjust up or down for your home's condition and amenities. Use leased prices, not active asking prices.

How often should I reprice a rental? Every time the property turns over, pull fresh comps before relisting. Between turnovers, review the market once before each renewal offer. Pricing should be revisited at least annually.

Are Florida rents going down in 2026? Apartment rents in Orlando and Tampa are down roughly 3% to 5% year-over-year as a wave of new construction is absorbed. Single-family home rents are holding up better, still rising modestly in line with national trends.

Getting your number right

Pricing well isn't guesswork and it isn't optimism — it's reading real comps, respecting the Empty-Month Math, and acting on showing feedback fast. Get it right and a good Florida house leases in weeks at a number you can defend.

If you'd like that done for you, our team's Free Rental Analysis pulls current comps for your specific property and gives you a defensible rent number — no guessing, no Zestimate. For the bigger picture on running a profitable Florida rental, start with our Owner's Guide.