House Hacking in Florida: Live in One Unit, Rent the Rest

Buy a 2-4 unit property in Florida with FHA, live in one unit for a year, and let the rent cover most of your mortgage. How it works in Orlando and Tampa.

Buy a duplex. Live in one side. Rent the other. Your tenant's rent covers most of your mortgage, and you're building equity while you sleep. That's house hacking — and in Florida it's one of the cheapest ways into real estate, because FHA lets you put as little as 3.5% down on a 2–4 unit property.

The catch is simple: you have to live there for at least a year. After that, you can move out, rent both units, and do it again. Here's how house hacking works in Orlando and Tampa, with real numbers.

• Live in one unit for at least one year — FHA and VA loans require owner occupancy. Moving out sooner creates problems with your lender.

• Run the self-sufficiency test on a triplex or fourplex — FHA requires 75% of the market rent from all units to cover the full PITI payment.

• Screen the other units' tenants as carefully as a standalone rental — you'll share walls with them.

• Use a proper Florida lease and collect a deposit under FS 83.49 for every rented unit.

• Split expenses for taxes — the rental portion goes on Schedule E; the part for your own unit doesn't.

Why does house hacking work in Florida?

House hacking works in Florida because the fundamentals line up: no state income tax, strong rental demand in Orlando and Tampa, and real duplex inventory in the suburbs. You buy a small multi-unit property with a low-down-payment owner-occupant loan and let a tenant's rent carry most of the mortgage.

The math is the appeal. Put 3.5% down on a $350,000 duplex and rent the other unit for around $1,650, and that rent covers 70–80% of your mortgage payment. You're living for a fraction of market rent while a tenant pays down your loan and Orlando or Tampa appreciation builds your equity. Duplexes turn up in suburbs like Brandon, Riverview, Lake Nona, and Avalon Park — close enough to job centers to lease easily.

What are the FHA requirements for a house hack?

An FHA loan on a 2–4 unit property requires 3.5% down with a 580+ credit score, and you must occupy one unit for at least a year. It's the lowest-cost financing path into a small multi-unit property, but it comes with rules worth knowing before you shop.

- Owner occupancy. You must live in one unit for at least one year — no exceptions.

- Property type. 2–4 units.

- Down payment. 3.5% of the purchase price. On a $350,000 duplex, that's $12,250.

- Credit. 580 minimum for 3.5% down; 500–579 can qualify with 10% down.

- Mortgage insurance. You'll pay MIP until you refinance or reach 20% equity.

- Self-sufficiency test (3–4 units). For a triplex or fourplex, FHA requires 75% of the appraiser's market rent from all units — including the one you'll live in — to cover the full PITI payment. Many higher-priced 3–4 unit deals fail this test, so run it early.

VA loans carry similar owner-occupancy requirements if you're eligible. For the full menu of financing options, see our guide to financing your first rental property in Florida.

Where do you find duplexes in Orlando and Tampa?

Small multi-unit inventory in Central Florida clusters near job centers, where rents are strong enough to support the mortgage. In Orlando, look around Lake Nona, Avalon Park, Winter Park, and Dr. Phillips, with prices generally running $300,000–$450,000. In Tampa, Brandon, Riverview, Seminole Heights, and South Tampa hold solid duplex stock around $320,000–$400,000.

Aim near the metro's demand drivers — Medical City, UCF, MacDill Air Force Base, and the downtown cores all anchor reliable renter pools. Our first rental property guide covers how to evaluate a location, and our deal analysis guide walks through running the numbers before you make an offer.

What do the numbers look like on a Tampa duplex?

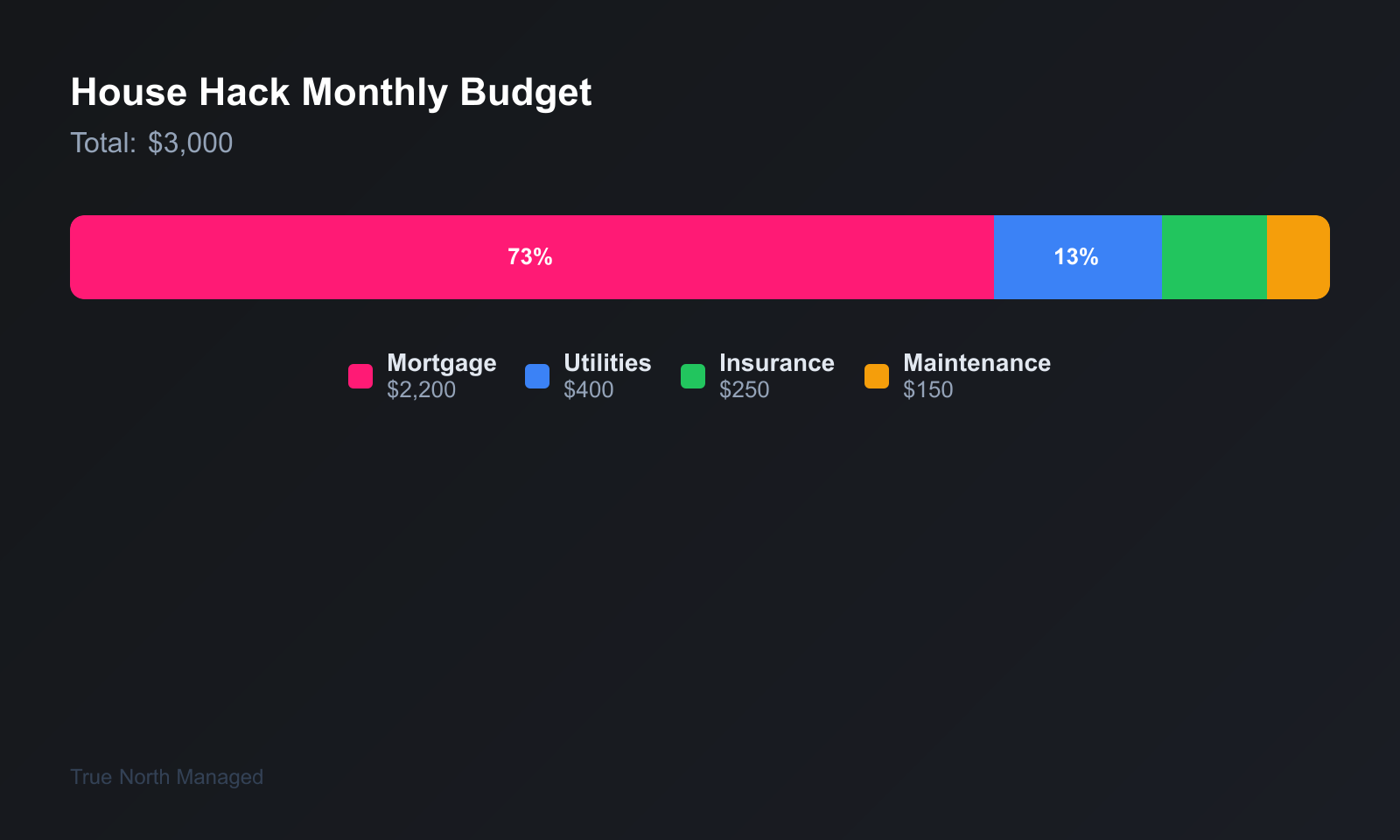

Here's a real-world example. A $360,000 duplex in Brandon at 3.5% down means $12,600 down plus roughly $10,000 in closing costs — about $22,600 total cash to get in. The other unit rents for $1,600 a month, and the total PITI runs about $2,876 a month.

Subtract the $1,600 of rent and your out-of-pocket housing cost is roughly $1,276 a month — less than most Tampa apartments, while you own the building and build equity. That's the house-hack advantage in one number. Just budget for the gap: if the rented unit sits vacant, you still owe the full $2,876, so keep a reserve and don't count on 100% occupancy.

How should you screen your first house-hack tenant?

Screen the tenant in the other unit exactly as carefully as you would for a standalone rental — income, credit, rental history, references. Don't relax your standards because you're the owner-occupant. You'll share walls and common areas, so a bad tenant next door isn't just a financial problem, it's a daily quality-of-life problem.

Run consistent, written screening criteria and apply them to every applicant — that's both good practice and fair housing compliance. Our guide to tenant screening and fair housing in Florida covers how to set criteria that protect you and stay legal. Use a proper Florida lease for the rented unit and collect a security deposit under Florida Statute 83.49, the same as any other tenancy.

What are the tax implications of house hacking?

When you live in one unit and rent the others, you split the property's expenses. The rental portion — a share of mortgage interest, insurance, repairs, depreciation — goes on federal Schedule E. The portion tied to your own unit is personal and isn't deductible.

There's an exit benefit too. When you eventually sell, you may qualify for the Section 121 capital gains exclusion on your own unit — up to $250,000 of gain if single, $500,000 if married filing jointly — but not on the rented units, which are subject to capital gains and depreciation recapture. A CPA who works with rental owners is worth the fee here. Our Florida rental tax deductions checklist covers what to track from day one.

What are the most common house-hacking mistakes?

A few mistakes turn a good house hack into a bad year. Avoid these:

- Buying in a bad neighborhood to save money. You're going to live there — pick somewhere you'd actually want to be.

- Ignoring the numbers. If the other unit's rent doesn't cover most of your mortgage, you're not really house hacking. Run the deal analysis first.

- Relaxing screening for the other unit. Owner-occupying is no reason to lower your standards — apply the same income, credit, and reference checks.

- Assuming FHA lets you rent every unit right away. You must occupy one unit for at least a year first.

- Not budgeting for vacancy. An empty unit doesn't pause your mortgage. Keep reserves.

- Skipping the HOA covenants. Some communities restrict or ban renting a unit — check the rules before you buy. Our guide to HOA risks for Florida investors covers what to look for.

House hacking only works if the numbers work. Get the deal analysis right, screen carefully, and follow the owner-occupancy rules — then after a year you can move on and rent your unit too, or refinance to a conventional loan and do it again.

Want a clear read on what the other unit could rent for before you make an offer? Get a free rental analysis — real market rent for Orlando and Tampa duplexes, no obligation.