How to Finance Your First Rental Property in Florida

Conventional, FHA house hack, DSCR, portfolio, hard money, HELOC -- how each financing option works for a Florida rental, with down payments and rates.

You've got the down payment. You've run the numbers on a few Orlando listings. But how do you actually pay for the thing? Financing a rental property works differently from financing a home you'll live in — and the right loan can save you thousands or open up a deal you couldn't otherwise touch.

Here's how each financing option works for a Florida rental: the down payment, the typical rate, and when each one is the right call.

• Get pre-approved before you shop — investment loans have stricter requirements than a primary-home loan.

• Shop 2–3 lenders. Half a point on a $300,000 loan is real money over 30 years.

• Budget for reserves. Lenders want 6 months or more of PITIA (principal, interest, taxes, insurance, association dues) in the bank at closing.

• Quote Florida insurance before you buy. Wind and flood premiums can swing your cash flow by thousands a year.

• Run the pro forma with the actual rate and down payment — not a generic estimate.

Why does financing matter for Florida rental investors?

Your financing choice drives three things: monthly cash flow, the size of your down payment, and how fast you can buy the next property. Florida charges no state income tax on rental income, but loan type and rate still decide whether a deal cash-flows. A 1% difference in rate on a $300,000 loan shifts the monthly payment by roughly $200.

Conventional investment rates have run in the 6.5–7.5% range through early 2026, with investment-property loans priced above owner-occupant loans. Orlando and Tampa both have deep lender pools for first-time investors — conventional banks, credit unions, and a strong bench of DSCR lenders. The point is to match the loan to your situation, not just chase the lowest advertised rate.

How do conventional investment loans work?

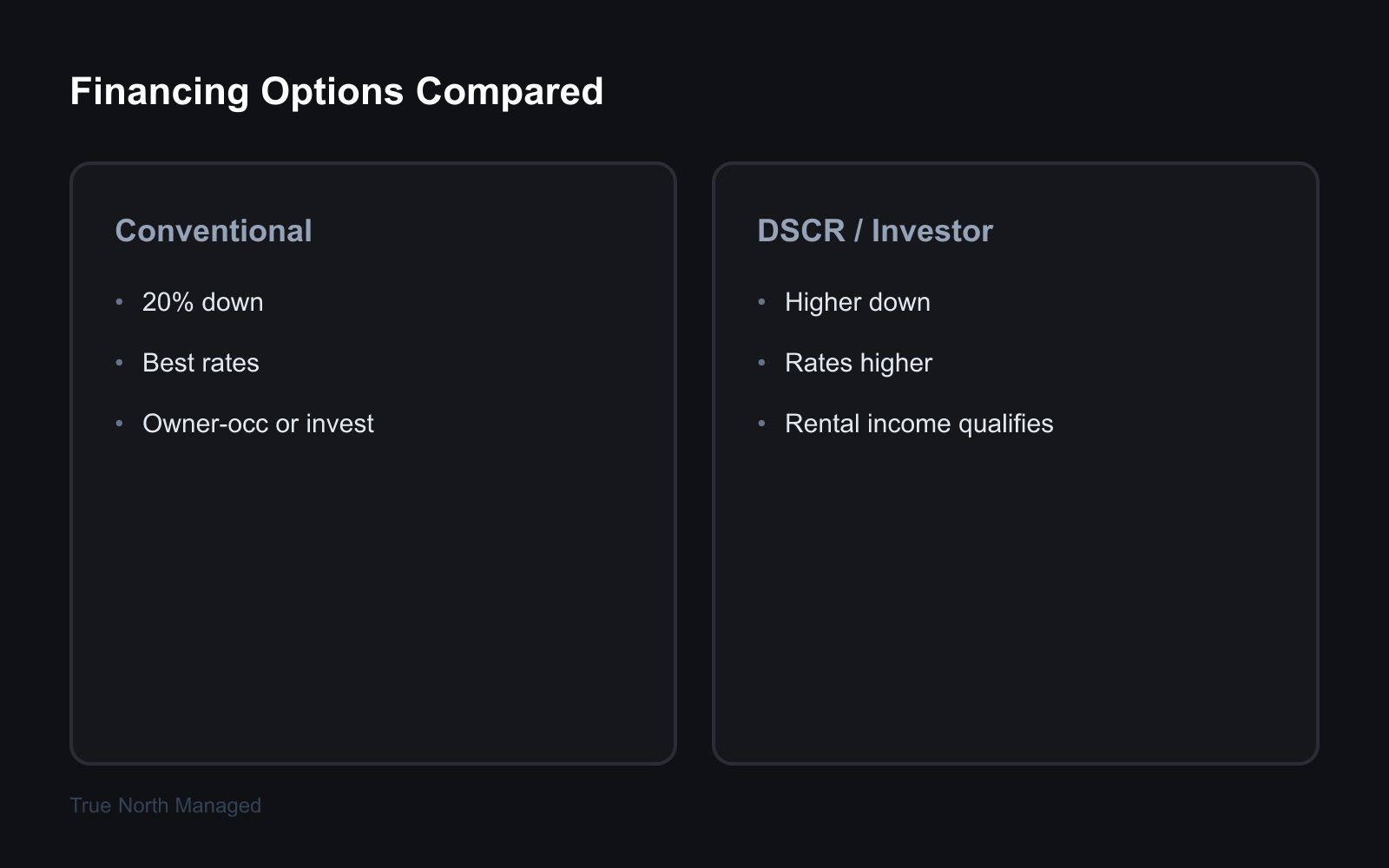

A conventional investment loan qualifies you on your income, credit score, and debt-to-income ratio, with the property treated as an investment rather than a primary residence. For a single-unit rental, the minimum down payment is 15%; for a 2–4 unit property, it's 25%. Most lenders prefer 20%+ on a single-family rental for the best pricing.

Down payment. 15% minimum on a single-unit rental, 25% on a 2–4 unit. A $300,000 Orlando single-family at 20% down means $60,000 plus closing costs.

Rates. Typically 0.5–0.875% above owner-occupant rates. If owner-occupant pricing is 7%, expect 7.5–7.875% on the investment loan.

Good for. First-time investors with W-2 income, a 680+ credit score, and 20–25% to put down. Fannie Mae allows a borrower to carry up to 10 financed properties, so a conventional loan can take you well past your first rental — though borrowers with 7–10 financed properties face higher reserve requirements.

Can you use an FHA loan to buy a rental in Florida?

Yes — through a house hack. An FHA loan lets you buy a 2–4 unit property with just 3.5% down (with a 580+ credit score) as long as you live in one unit for at least a year. You rent the other units, and that rent helps cover the mortgage.

Down payment. 3.5% of the purchase price. On a $350,000 Tampa duplex, that's $12,250 — a fraction of what a conventional investment loan would require.

The catch on triplexes and fourplexes. FHA applies a self-sufficiency test to 3–4 unit properties: 75% of the appraiser's market rent from all units, including the one you'll occupy, must cover the full PITI payment. Many higher-priced 3–4 unit properties fail this test, so run it early.

Good for. First-time buyers willing to live on-site for a year. It's the lowest-down-payment path into a rental in Florida — our full house hacking in Florida guide walks through finding and running a 2–4 unit deal.

What is a DSCR loan, and when should you use one?

A DSCR loan qualifies you on the property's rental income instead of your personal income. DSCR stands for debt service coverage ratio — net operating income divided by annual debt service — and most lenders want a ratio of 1.0–1.25x, meaning the rent covers the loan payment with a cushion.

Down payment. Usually 20–25%.

Rates. Often 1–2% higher than conventional. Expect roughly 8–9%.

Good for. Self-employed investors whose tax returns understate their income, or anyone past the conventional financed-property limit. Orlando and Tampa both have plenty of DSCR lenders, and no personal income verification means a faster, simpler file. Just factor Florida's higher insurance cost into the ratio — it raises debt service and can pull the DSCR below the lender's minimum.

What about portfolio and hard money loans?

Portfolio and hard money loans are specialty tools — useful in the right situation, wrong for most first rentals. A conventional or DSCR loan is the typical path for a first Florida rental, but it's worth knowing what's next.

Portfolio loans. A local bank or credit union holds the loan on its own books instead of selling it. That means more flexible terms — but fewer lenders offer them, and they're aimed at investors scaling a real portfolio rather than buying property number one.

Hard money loans. Short-term, asset-based loans from private lenders. Florida rates run 10–14% plus 2–5 points, with fast funding but a high cost. They fit a BRRRR rehab or a flip with a clear 6–12 month exit — not a buy-and-hold rental.

Should you use a HELOC or cash-out refinance?

If you have equity in a paid-off home or an existing rental, you can tap it to fund the next purchase. Orlando and Tampa have seen strong appreciation, so for many owners that equity is real and usable.

A HELOC is a revolving line of credit secured by the property — you draw what you need and pay interest only on the balance. A cash-out refinance replaces your existing mortgage with a larger one and hands you the difference. A HELOC keeps your low first-mortgage rate intact and works well for a short-term need; a cash-out refi makes more sense when you want a fixed rate on a large, long-term draw. Either way, you're adding debt to a property you already own, so make sure the new purchase carries it.

What are the most common financing mistakes?

First-time investors lose money in a handful of predictable ways. Here's what to avoid:

- Shopping rate alone. A slightly lower rate can come with worse terms, higher fees, or slow service that costs you a deal. Compare the full offer.

- Assuming you'll qualify. Get pre-approved before you make offers — investment loans have stricter credit, reserve, and down-payment requirements than a primary-home loan.

- Under-budgeting for insurance. Florida wind and flood premiums have doubled in some areas. A $200/month insurance swing changes annual cash flow by $2,400. See our flood insurance guide for Florida rentals.

- Ignoring reserves. Lenders want 6 months or more of PITIA in reserves, and you should keep your own cushion on top of that for repairs and vacancy.

- Buying at your maximum approval. Leave room in the budget for turnover, repairs, and a month or two of vacancy. Our breakdown of the hidden costs of a Florida rental covers what first-time buyers miss.

- Skipping the pro forma. Run the numbers with your actual rate and down payment before you make an offer — our Florida rental pro forma guide shows how.

One more lever that's free: build your credit before you shop. Lenders pull scores at pre-approval, and a 720+ score lands a better rate tier than a 680. Pay down cards, avoid opening new credit, and fix report errors. Six months of clean credit behavior can move you into a lower rate — real savings over a 30-year loan.

Conventional vs. FHA vs. DSCR: which loan is right?

For a first Florida rental, the choice usually comes down to three loans. Conventional fits a W-2 buyer with 15–25% down who wants the lowest rate. FHA fits a buyer willing to live in one unit of a 2–4 unit property for a year and put just 3.5% down. DSCR fits a self-employed investor or anyone qualifying on the property's income rather than a tax return.

Whichever you pick, the discipline is the same: shop 2–3 lenders, factor Florida's insurance cost into your debt coverage, keep 6+ months of PITIA in reserves, and run the pro forma before you offer. Financing is one piece of the deal — whether the property cash-flows is the other.

If you own a rental in Orlando or Tampa, or you're about to buy your first, a clear read on what it can earn changes the financing math. Get a free rental analysis — real market numbers, no obligation.