How to Set the Right Rent for Your First Florida Rental

Pricing your first Florida rental? Here's the comp-based method that beats guesswork — plus the 14-day test that tells you fast if your number is too high.

Most people don't plan to become a Florida landlord. You got relocated, you inherited a house, or you listed it to sell and the offers never came — and now there's a property you need to rent. The first real decision lands fast, and it's the one that costs the most if you get it wrong: what do you charge?

Here's the short version. To set rent for your first Florida rental, pull three to five real comparable listings near your property, price your home at roughly the 70th to 85th percentile of that range, market it hard, and then watch the first two weeks. If those two weeks are silent, your number is too high — and the market is telling you before it costs you a full month of vacancy. Let's break down how to do each part.

How do you actually set rent for your first Florida rental?

Setting rent for a first Florida rental is a five-step method: pull true comps, place your home in a percentile band based on its condition, list it at that number, read the response over the first 14 days, and adjust once if the market goes quiet. The number comes from the market, not from your costs.

That last part trips up almost every first-timer. Florida has no rent control — Florida Statute 125.0103 bars cities and counties from capping what landlords charge. So legally, you can put any number you want on that listing. The law gives you total freedom here.

The market gives you none. Renters in Orlando, Tampa, and every metro in between have a phone, twenty open tabs, and a clear sense of what a three-bedroom in your zip code should cost. Your job isn't to pick a number you like. It's to find the number that's already true and claim it before someone underprices you to it. Before you even reach the pricing step, it helps to know what it costs to become a landlord in Florida so the rent you set is measured against a full picture of your numbers.

Why shouldn't you price to your mortgage payment?

You shouldn't price to your mortgage because the market doesn't know what you owe and doesn't care. Rent is set by supply, demand, and what comparable homes are leasing for — not by your loan balance, your taxes, or the repairs you just paid for. Pricing to your costs is the single most expensive first-timer mistake in Florida.

Call it "the Mortgage Mirror." You look at your monthly nut — principal, interest, taxes, that newly painful insurance premium — and you see a rent number reflected back. It feels objective. It isn't. It's just your costs wearing a disguise.

Picture an accidental landlord in Winter Garden. Her mortgage, taxes, and insurance run $2,650 a month, so she lists her house at $2,800 to "stay ahead." The comps for her street say $2,400. She's not ahead — she's $400 over market, and her house is going to sit. Meanwhile a renter three streets over signs a lease in nine days at $2,375, because that landlord priced to the market instead of to a bank statement.

This matters more in 2026 than it did a few years ago. Florida's rental market has cooled into a normalization phase — Florida Realtors' 2026 outlook describes more supply, softer rent growth, and vacancy running near 10% across most metros. Renters can shop. Some new apartment communities are dangling a free month to fill units. An overpriced single-family listing doesn't just sit — it sits while competing against concessions. If your costs are higher than the market rent, that's a hard truth worth knowing now. But the answer is never to make the renter pay for it. They'll just rent the house down the block.

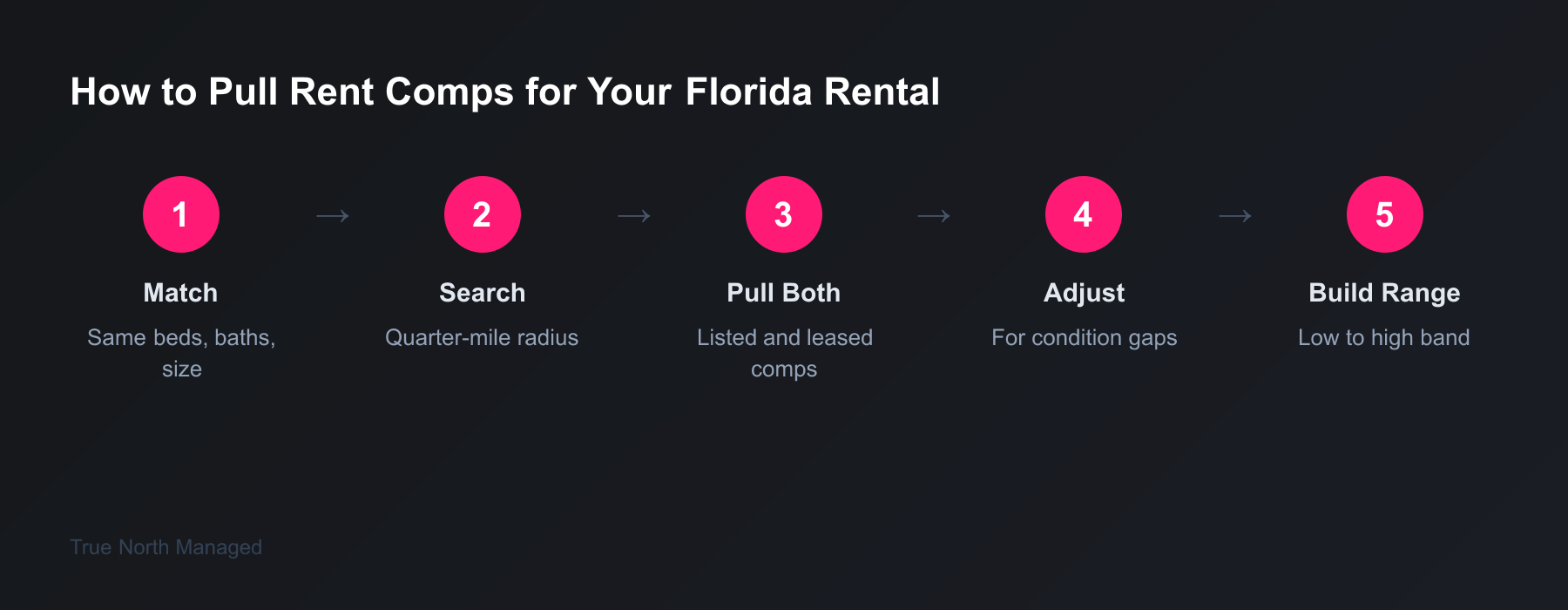

How do you pull real rent comps?

You pull rent comps by finding three to five homes near yours — within a quarter to a half mile — that match your bedroom count, bathroom count, and square footage, and that are either listed for rent right now or leased in the last few months. Active competing listings are your most important comps, because those are the homes a renter is choosing between instead of yours.

Don't lean on a single algorithm. Zillow's Rent Zestimate and Rentometer are fine as a quick gut check, but both can miss real market rent by 5 to 10% — sometimes more in neighborhoods with thin data. They're a starting cross-reference, not a verdict. Treat them like a weather app: useful, often close, occasionally just wrong.

Here's the process I'd walk a new owner through:

- Define your match. Same bedroom and bathroom count. Square footage within about 15%. Same general property type — don't compare your house to an apartment.

- Search a tight radius. A quarter to a half mile. In Florida, crossing one major road or one school zone can move rent $150, so keep it close.

- Pull both kinds of comps. Currently listed homes show you the asking market. Recently leased homes show you what renters actually paid. You want both.

- Adjust for the gaps. Your comp has a renovated kitchen and yours doesn't? Adjust down. Yours has a fenced yard and a screened lanai theirs lacks? Adjust up. Be honest.

- Build your range. Line up the adjusted numbers. The low and high give you a band — and your home's real condition decides where in that band you land.

If your rental is in Orlando or Tampa, we've already done the metro-level homework. Our guide to how much you can charge for rent in Orlando and the companion piece on setting rent in Tampa both walk through neighborhood-level numbers and the comp adjustments that matter most in each market. As a benchmark, Orlando apartments average around $1,782 a month and Tampa single-family homes around $2,600, per RentCafe's 2026 market data — but those are backdrops, not your answer. Your answer comes from the five comps closest to your front door.

Where in the comp range should your number land?

Your rent should land at the 70th to 85th percentile of your comp range — not the average, and not the top. The exact spot depends on your home's condition. A clean, updated, move-in-ready home earns the upper end. An average or dated home belongs at the bottom of the band or just below it.

Aiming above the average is deliberate. You want to test whether the market will pay a bit more, and you'd rather start slightly high and have room to come down than start low and lock in a below-market number for a 12-month lease. But the top of the band is earned, not assumed.

Formula: Comp range low to high → place at the 70th–85th percentile → adjust for condition.

Example: Your three-bedroom house in Brandon has comps ranging from $2,200 (dated, no updates) to $2,600 (renovated, fenced yard). The band's 70th–85th percentile is roughly $2,480 to $2,540. Your kitchen was redone two years ago and the AC is new, but the bathrooms are original. That's solidly above-average condition — not top-of-market. List at $2,500.

What's good or bad? If you're tempted to list that same house at $2,600 because one comp got it, stop. That comp had renovated bathrooms and yours doesn't. Matching a comp's price without matching its condition is how a listing goes stale. And listing at $2,200 because you just want it filled leaves $300 a month — $3,600 over the lease — on the table.

What is the 14-day test, and how do you read it?

The 14-day test is simple: after your listing goes live, the first 10 to 14 days draw the most attention a rental will ever get. If a well-marketed home gets few inquiries and no applications in that window, the rent is too high. Two quiet weeks is the market voting no — and it's a far cheaper messenger than a vacant month.

Florida single-family rentals now take around 36 days to lease on average, up from about 25 days in 2022. But "leased in 36 days" usually means a listing that drew interest early, not one that sat silent. A faster signal: if a well-marketed listing gets fewer than three qualified inquiries in the first 72 hours, your rent is likely sitting 10 to 15% above market.

Here's what you must do during those 14 days:

- Days 1–3: Confirm the listing is actually live everywhere and the photos are good. No inquiries on a broken or invisible listing isn't a pricing signal — it's a marketing problem.

- Days 3–7: Count qualified inquiries. Fewer than three or four from a clean, well-marketed listing is an early warning.

- Days 7–10: Look at showings and applications. Lots of clicks but no showings often means the price scared people off before they reached out.

- Days 10–14: If you have no application and weak interest, drop the rent. One adjustment of 3 to 5%, made decisively. Don't trickle it down $25 at a time over two months.

Why move that fast? Run the math. Say your target rent is $2,000 and your fixed monthly costs — mortgage, taxes, insurance — run about $1,500. One vacant month doesn't cost you $2,000. It costs you the lost rent plus the carrying costs you pay anyway: roughly $3,300 once you count it honestly. Industry data from the National Association of Residential Property Managers puts each vacant month at 1.5 to 2 times the monthly rent.

Now weigh that against the thing you were protecting. Holding firm at $2,075 instead of dropping to $2,000 earns you $75 a month — $900 over a year-long lease. One extra month of vacancy chasing that $75 wipes out three-plus years of the gain. The 14-day test exists so the market can correct you for free, before vacancy corrects you for $3,300.

Common mistakes first-time Florida landlords make on rent

First-time Florida landlords lose the most money to three pricing mistakes: anchoring rent to their mortgage instead of the market, defaulting to the top of the comp range, and ignoring the 14-day signal because they don't want to believe it.

- Pricing to the Mortgage Mirror. Your costs are your problem to solve — through a lower purchase price, a refinance, or a tax appeal — not the renter's. The market sets rent. Your spreadsheet doesn't get a vote.

- Defaulting to the top of the band. The 70th–85th percentile is a range for a reason. You earn the high end with above-comp condition. List at the top with an average home and you've just talked yourself into the overpriced trap on day one.

- Ignoring two weeks of silence. When the inquiries don't come, the instinct is to wait "one more week" and blame the photos, the weather, the season. Sometimes it is the photos. Usually it's the price. Adjust decisively at day 14.

- Pricing applicants differently. Set one published number and apply it to everyone. Quoting different rent or offering a concession to some applicants and not others can run into the Florida Fair Housing Act. One number, one standard.

Pricing is the first real test of being a landlord, and it sets the tone for the whole lease. Get it right and your house leases in two or three weeks to a tenant who feels they got a fair deal. Get it wrong and you're staring at an empty house, watching $3,300 a month walk out the door while you wait for a number the market already rejected. If you want the bigger picture on starting out, our guide for accidental landlords in Florida covers the early decisions, and the first 90 days as a Florida landlord walks through what comes after the lease is signed.

Not sure where your number should land? You don't need to own a portfolio to get help — we price and manage single properties all the time. Request a free rental analysis and our team will pull the comps near your home, weigh its condition honestly, and give you a rent recommendation built on current Florida market data. For more on building a rental the right way from the start, the Florida Owner's Guide is the place to begin.