Florida Rental Application Fee Laws: What Landlords Can Charge

Florida puts no cap on rental application fees, but that freedom comes with strings. Here's what you can legally charge, what the fee can cover, and the FCRA and fair-housing rules that actually bind you.

Here's a question almost every Orlando and Tampa landlord gets wrong: what's the legal limit on a rental application fee in Florida? Most people assume there's a number. There isn't.

Florida rental application fee laws set no statewide cap on what you can charge an applicant. You set the fee yourself. But that freedom is exactly the trap. The real rules that bind you aren't about the dollar amount. They're about how you describe the fee, whether it's refundable, how it differs from a deposit, and the federal screening laws that kick in the moment you pull a credit or background report.

Get those wrong and a $50 fee can turn into a fair-housing complaint or an FCRA lawsuit. Let's break down what you can and can't do.

Do Florida rental application fee laws cap what you can charge?

No. Florida has no statewide cap on rental application fees. Unlike California, New York, or Wisconsin, the state sets no maximum dollar amount and requires no specific fee. A 2025 Florida Senate staff analysis confirmed there is "no statutory cap" on what a landlord may charge an applicant.

That makes Florida one of the more landlord-friendly states on this point. Several states tie application fees to actual screening costs or ban them outright. California caps them at the landlord's real costs (around $62 per applicant, indexed to inflation). New York limits them to $20. Wisconsin, $25. Virginia, $50. Vermont prohibits them entirely.

Florida does none of that. You decide the amount.

That doesn't mean you should charge whatever you want. The state's silence on a cap isn't permission to turn screening into a profit center. Courts and fair-housing investigators look at whether a fee reasonably reflects the cost of processing the application. A fee that's wildly out of line with what screening actually costs invites scrutiny, even without a statute naming a number.

It's also worth knowing the rule almost changed. CS/SB 362 in the 2025 session would have restricted certain screening fees when applicants used a reusable screening report. That bill was withdrawn from consideration on May 3, 2025 and died in Community Affairs on June 16. It never became law. So as of the 2026 leasing season, there is still no cap and no fee restriction tied to portable reports on the books.

What's a reasonable application fee in Orlando and Tampa?

A reasonable Florida application fee covers your actual screening costs plus a modest amount for the time it takes to process. In practice, that lands most fees between $30 and $75 per adult applicant. Across Orlando and Tampa, $30 to $50 is the common range. There's no legal number, only a defensible one.

Here's the math behind a defensible fee. A credit report runs roughly $15 to $30. A background and eviction-history check adds another $15 to $40 depending on the provider. Then there's your time, calling prior landlords, verifying income, reviewing the file. Add those up and a $40 to $50 fee per adult covers it without padding.

Two practical notes for Florida landlords:

- Charge per adult, not per unit. Every adult who will be on the lease gets screened individually, because background and credit checks are run on individuals. A per-adult fee tracks the real cost. A married couple is still two separate screens.

- Stay competitive. In a market where applicants are filling out three applications in a weekend, a $150 fee makes your unit the one they skip. Pricing close to your actual cost keeps your applicant pool wide, which is its own form of risk management.

The point isn't to be generous. It's that a fee tied to real costs is one you can defend if an applicant ever challenges it, and it keeps good tenants applying.

Are rental application fees refundable in Florida?

Generally, no. A Florida rental application fee is non-refundable by default, and the state does not require you to return it, even if you deny the applicant or the applicant withdraws. The fee pays for screening work you already performed. Once you've run the reports, the money has done its job.

But "non-refundable" only holds if the money is genuinely a screening fee. This is where landlords get into trouble. If you collect money to "hold" the unit, or money that will later be applied to rent or to a deposit, that's no longer just an application fee. The label you put on it doesn't control. The function does.

So if you take $300 to take the property off the market while you decide, and you'd give it back if the applicant doesn't get approved, you've collected a refundable holding deposit, not a fee. Treat it like one. The single best protection here is to keep the screening fee small and separate from any money that secures the unit, and to put both in writing before you collect a dollar.

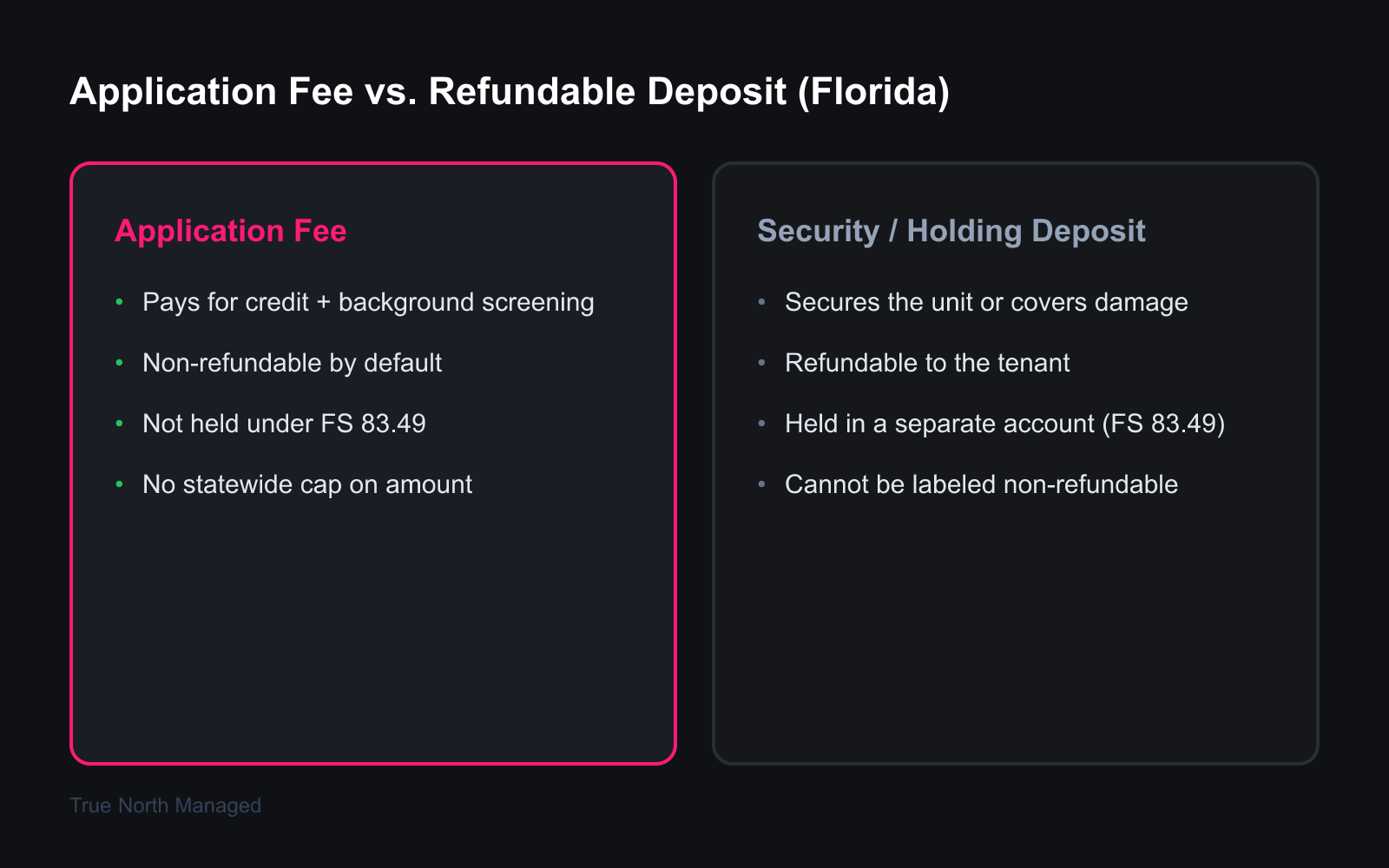

Application fee vs. holding deposit vs. security deposit: what's the difference?

These are three different things with three different legal treatments. An application fee is non-refundable and covers screening. A holding deposit is refundable and reserves the unit while you finish processing. A security deposit is fully refundable and protects against damage and unpaid rent. Mixing them up is one of the most common Florida landlord mistakes.

The distinction matters because Florida Statute 83.49 governs how you handle deposits, and it has teeth. Any money you take "as security" for the lease, or as advance rent for a period beyond the next immediate rental period, has to be held in a separate account. You can't commingle it with your own funds or spend it before it's actually due to you.

Here's how the three break down:

- Application fee. Pays for credit and background screening. Non-refundable. Not held under 83.49 because it isn't security or rent. It's a payment for a service.

- Holding (good-faith) deposit. Takes the unit off the market while you finish screening. If you market it as refundable on denial, it's refundable. If the lease signs, it typically converts to rent or the security deposit. If it secures the unit or gets applied to rent, the deposit-handling rules can reach it.

- Security deposit. Protects against damage and unpaid rent. Always fully refundable when the tenant meets the lease and leaves the place in good shape. Florida does not let you label any part of a security deposit as non-refundable. It must be held separately, and you owe the tenant written notice of any claim within 30 days of move-out (the tenant then has 15 days to object), or a full return within 15 days if you make no claim. The written-disclosure requirement applies to landlords who rent five or more units, so a single-property owner is exempt from that notice piece, though the separate-account and return-timeline rules still apply.

There's also a fourth option worth knowing. Under Florida Statute 83.491, for leases signed or renewed on or after July 1, 2023, you may offer a tenant the choice to pay a recurring, non-refundable fee instead of a traditional security deposit. There's no cap on that fee either, and it's non-refundable by design, but it comes with its own notice rules: you have to tell the tenant within 30 days after the tenancy ends if any costs are owed. For the full picture on deposits and how 83.49 timelines work, see our Florida security deposit law guide.

The takeaway: name each charge accurately, hold deposits the way the statute requires, and never treat a deposit like income.

What do FCRA and fair housing require when you charge a fee and screen?

If you charge an application fee, you're almost certainly pulling a credit or background report, and that triggers two federal laws: the Fair Credit Reporting Act (FCRA) and the Fair Housing Act. Both apply in Florida regardless of your fee amount. Ignoring either is far riskier than charging the "wrong" fee.

The Fair Credit Reporting Act. Before you run a consumer report, you need a permissible purpose and you must certify to the screening company that you'll use the report only for the housing application. You generally need the applicant's written authorization first. The bigger obligation comes if you say no: under the FCRA's adverse action rules for landlords, if you deny an applicant, require a co-signer, or demand a higher deposit based even in part on a report, you have to give an adverse action notice. That notice tells the applicant which reporting agency was used, makes clear the agency didn't make the decision, and explains their right to a free copy of the report and to dispute errors. Willful violations expose you to actual damages or statutory penalties up to $1,000 per instance, which is why a written adverse action notice (not a verbal "you didn't qualify") is the only safe practice.

Fair housing. Whatever you charge, charge it the same way to everyone. The Fair Housing Act's protections require that your fee and your screening criteria apply uniformly to every applicant, regardless of race, color, national origin, religion, sex, familial status, or disability. Waiving the fee for one applicant, charging another more, or applying your standards loosely for some and strictly for others, that's the behavior that produces complaints. Write your criteria down, set the fee once, and apply both consistently to every single applicant.

These two laws are the real ceiling on application fees in Florida. The dollar amount is up to you. How you screen and how you decide is not.

Do local Orlando or Tampa rules change any of this?

No. Since July 1, 2023, Florida law preempts local governments from regulating residential tenancies, including application fees. Florida Statute 83.425 expressly reserves "rental application terms and associated fees," the screening process, and required disclosures to the state. Orange County, Hillsborough County, Orlando, and Tampa cannot add their own application-fee rules on top of state law.

This wiped out a wave of local tenant-protection ordinances. Hillsborough County's Tenant Bill of Rights, which had required certain written disclosures before an applicant applied, was among the rules superseded by the preemption. For a standard residential rental, the state framework is the whole framework.

One real exception applies to condos. If your rental sits in a condominium where the association's approval is required to lease, the Florida Condominium Act (Chapter 718) caps what the association can charge for its own screening or transfer fee. As of 2025 that association cap is $150 per applicant, with spouses and dependents counted as one, and the figure is indexed and reviewed periodically. That's a limit on the association's fee, not on your application fee as the unit owner. The two are separate charges, and an applicant for a condo rental could face both.

If you own outside an HOA or condo, none of this applies. You set the fee, you follow FCRA and fair housing, and you're done.

Common application-fee mistakes Florida landlords make

The fee itself is rarely the problem. How landlords handle the money and the paperwork around it is. After screening hundreds of applicants across Orlando and Tampa, these are the three we see most.

Calling a deposit a "fee" to keep it. A landlord takes $400 to hold the unit, the deal falls through, and they pocket it as a "non-refundable fee." If that money was actually securing the property, it walks and talks like a deposit, and trying to keep it can land you in a deposit dispute under Florida Statute 83.49. Keep your screening fee small, separate, and clearly labeled. Put any holding money in its own written agreement.

Skipping the adverse action notice. You deny an applicant because of something on their credit report and just tell them "it didn't work out." That's an FCRA miss. Any denial driven even partly by a report needs a written adverse action notice. Building that into your screening workflow is far cheaper than a statutory-damages claim. Our Florida tenant screening process guide lays out where the notice fits in the sequence.

Bending the rules for applicants you like. Waiving the fee for a friendly applicant, or running a softer screen for one and a stricter one for another, feels harmless. It's a fair-housing landmine. Uniform criteria and a uniform fee protect you. If you're not sure what disqualifying information looks like, our guide to rental application red flags and our breakdown of rental application fraud in Florida show how to apply the same standard to everyone, fairly.

The pattern is clear: the fee is legal, the freedom is real, but the discipline around the money and the decision is where you protect yourself. For the bigger picture on screening, leasing, and compliance, our Florida owner's guide ties it all together.

Charging an application fee correctly is one small piece of running a Florida rental well. If you'd rather not manage the screening, the notices, and the compliance yourself, get a free rental analysis and we'll show you what your property can earn and how we handle the details.