Florida's 2026 Property-Tax Amendment: What the 10%-to-5% Cap Means for Landlords

The headline is a bigger homestead exemption — which won't touch your rentals. The part that does is a quieter cap change. Here's what the 2026 amendment means for landlords.

Every Florida landlord knows the line item that ruins a budget: the property-tax bill that climbs faster than the rent. You set a rent in January, and by the next assessment your taxable value has jumped double digits. So when "the biggest property-tax cut in Florida history" started making headlines this summer, it was fair to wonder whether relief was finally coming for rentals, too.

Mostly no on the headline — but yes on a quieter piece buried inside it. The marquee change — a much bigger homestead exemption — does nothing for property you rent out, because rentals aren't homesteaded. The part that actually reaches landlords is a change to how fast your rental's assessed value can rise each year. Let's separate the two so you know what to plan for.

What is Florida's 2026 property-tax amendment?

It's a constitutional amendment (CS/HJR 1-F) on the November 2026 ballot that would expand the homestead exemption for owner-occupants and, separately, lower the annual assessment cap on non-homestead property from 10% to 5% starting January 1, 2027. On your ballot it carries the Legislature's own title — "Save Our Homes from Excessive Property Taxes" — and the Division of Elections assigns its amendment number before November. It needs 60% voter approval to pass. Nothing changes unless voters say yes in November.

The Legislature approved putting it on the ballot on June 2, 2026 — the House 75–26, the Senate 30–9, both clearing the three-fifths threshold a joint resolution requires. You can read the resolution itself on the Florida House's HJR 1-F page, and Ballotpedia's summary lays out the full text. The measure bundles a few things together, but for a landlord, only one of them matters — and it's not the one in the headlines.

Does the bigger homestead exemption help your rental?

No. The headline change raises the homestead exemption to $150,000 in 2027 and $250,000 in 2028, but a homestead exemption only applies to a property the owner lives in as a permanent residence. A house you rent to a tenant isn't your homestead, so none of that exemption flows to it. If you own the home you live in, you'll benefit personally — but your rentals are untouched by that part.

This trips up a lot of owners, so it's worth being blunt. When a neighbor says "my property taxes are getting cut $2,000," they're talking about the house they live in. Your rental down the street doesn't get the exemption, doesn't get the new-resident break, and doesn't share in the marquee number. The amendment treats your home and your investment property as two different animals — because the law always has.

What actually changes for landlords? The 10%-to-5% cap

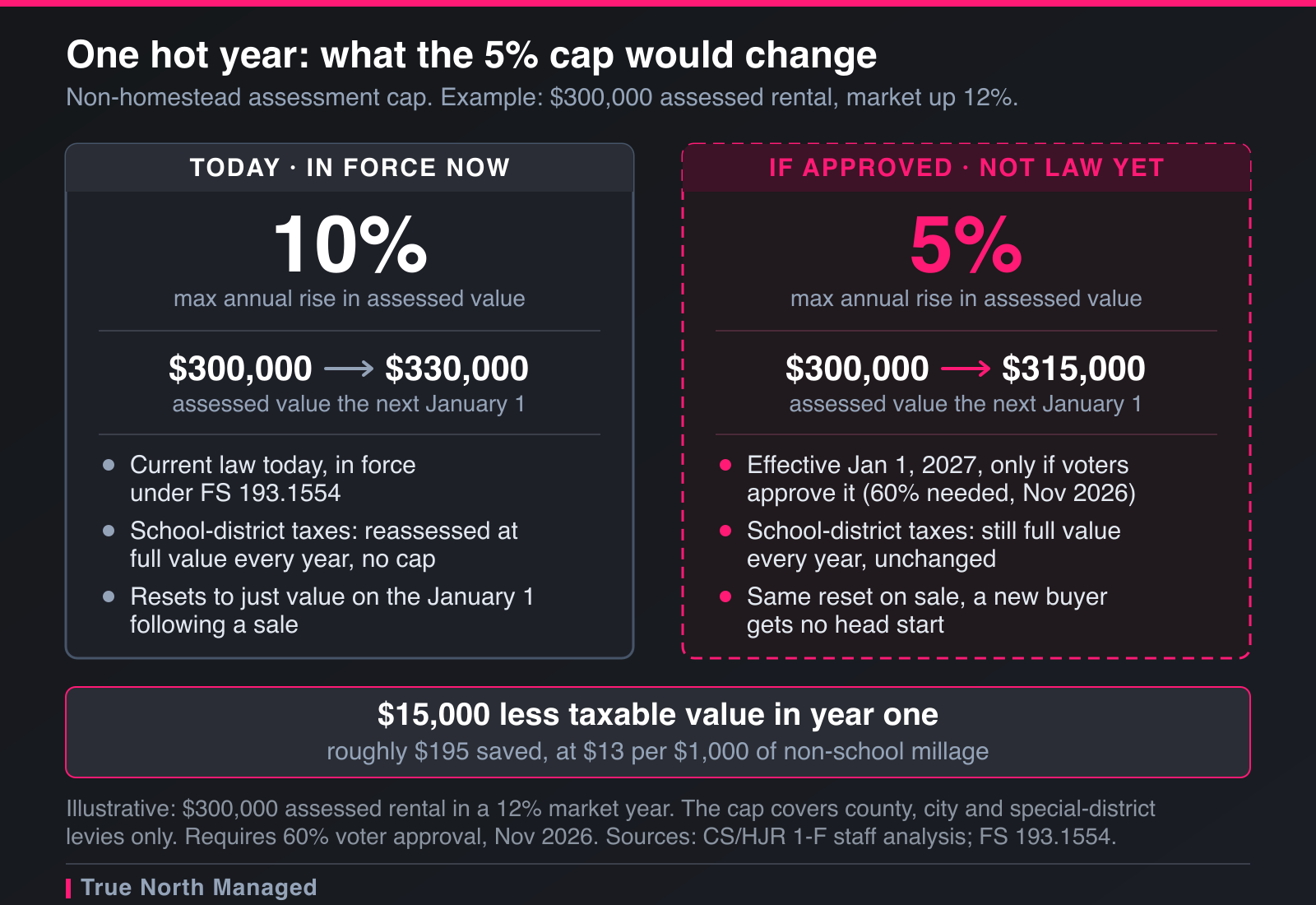

The piece that reaches your rentals is the non-homestead assessment cap. Today, the assessed value of a non-homestead property can rise up to 10% a year. The amendment would cut that ceiling to 5% beginning January 1, 2027. It limits how fast the taxable value grows — not the tax rate itself.

Florida already caps non-homestead assessment growth under Statute 193.1554 (and 193.1555 if you own commercial property or a building with 10-plus units). Every January 1, the county reassesses your rental, and the assessed value can't jump more than the cap over the prior year — even if the market ran hot. Drop that ceiling from 10% to 5% and your taxable value climbs at half the pace in a strong appreciation year. Over a stretch of hot years, that gap compounds.

Two details matter before you get excited. First, the cap has always excluded school-district taxes, and that doesn't change — the 5% ceiling applies to county, city, and special-district millage, but the school portion of your bill is reassessed at full value every year. Second, the cap resets on a sale. Buy a rental and it gets reassessed at just value on the January 1 following the closing — your 5% clock starts over from that new, higher base. Call it "The Reset Trap": the landlord who has held a rental for ten years gets real protection from the lower cap, while the one who just closed gets none, and starts again from the top of the market.

Isn't there already a cap? How this differs from Save Our Homes

Yes, but the one you've heard of doesn't cover rentals. "Save Our Homes" caps assessment growth at the lesser of 3% or the year's change in the Consumer Price Index (FS 193.155) — and only on a homesteaded primary residence. In a low-inflation year the real ceiling lands well under 3%. Rentals never got that protection. The 10% non-homestead cap (which this amendment lowers to 5%) is the separate, weaker ceiling that applies to investment property.

It helps to see the three tiers side by side. Owner-occupied homes have the tightest cap at 3% under Save Our Homes, a 1990s protection that's why your neighbor who's lived in their house for twenty years pays so little. Non-homestead residential and commercial property got nothing until 2008, when voters added a 10% cap through Amendment 1. This 2026 measure tightens that newer, looser cap to 5% — closing part, but not all, of the gap between what homeowners and landlords are protected from. Your rental still won't enjoy the 3% homeowner ceiling, and it still loses its capped base entirely when you sell. But a 5% annual limit is a real improvement over 10% for anyone planning to hold.

How much could the 5% cap actually save you?

In a single year, the savings are modest — tens to a couple hundred dollars on a typical rental. The cap's real value shows up across several hot years in a row, when it keeps your taxable value from compounding upward at 10% a year. It's a slow-acting shield, not a rebate.

Here's the math in plain terms.

Formula: (Assessed value under 10% cap − assessed value under 5% cap) × your non-school millage rate = the year's savings.

Example: Your Tampa rental is assessed at $300,000, and the market jumps 12% this year. Under the old 10% cap, the assessed value can rise to $330,000. Under the new 5% cap, it stops at $315,000 — $15,000 less taxable value. If your non-school millage runs about $13 per $1,000 of value, that's roughly $195 saved this year.

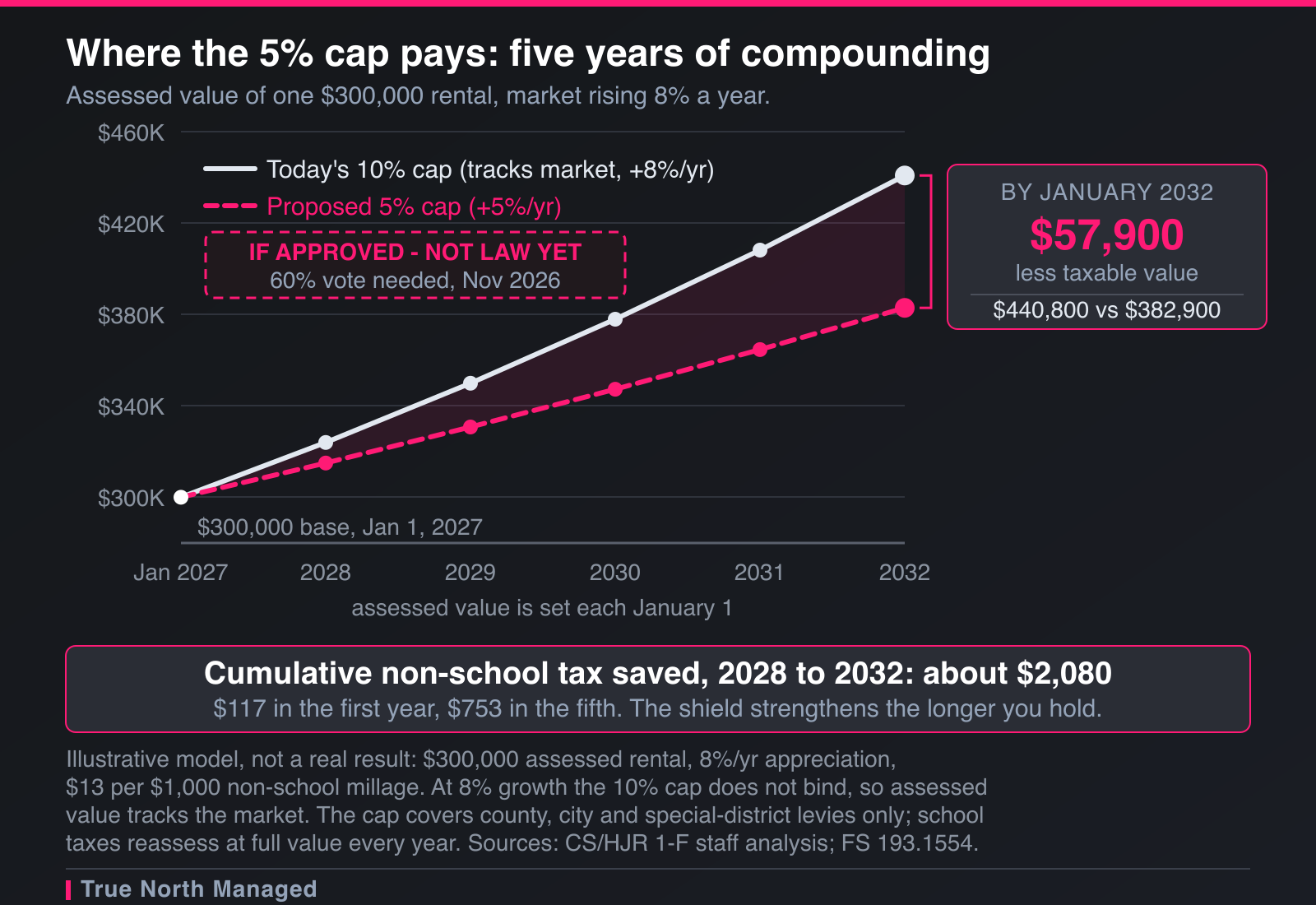

What's good or bad? One year of $195 won't change your returns. Run it forward and the gap widens. Take that same $300,000 rental in a market rising 8% a year: by January 2032 the 5% cap would hold your assessed value near $382,900 against roughly $440,800 without it — about $57,900 less taxable value, and roughly $2,080 in cumulative non-school tax saved over those five years. It starts at $117 in year one and reaches $753 by year five. The shield strengthens the longer you hold — which is the whole point, and exactly why it does nothing for the landlord who just closed. For a long-term hold in an appreciating submarket like Lake Nona or Seminole Heights, the lower cap is quietly worth real money over a decade. For a property you plan to flip in two years, it barely registers.

What won't the 5% cap do?

It won't cut your tax bill on its own. The cap limits assessed value, but your actual tax is assessed value times the millage rate — and local governments set the millage. And the hole here is not small. The House's own staff analysis puts the hit to local government revenue at more than $8 billion in FY 2027-28, and more than $14 billion in FY 2028-29. Money that size does not simply evaporate from a county budget — it gets found somewhere, through millage, fees, or both. One wrinkle worth knowing: the same amendment also restricts what counties and cities may spend ad valorem revenue on (public safety, schools, infrastructure, natural resources, debt service, retirement obligations). It constrains how the money is used — it does not stop them from raising the rate. The Tax Foundation flagged exactly this: the amendment shifts the tax burden rather than erasing it, often toward sales taxes and local fees.

So treat the 5% cap as protection against runaway assessments, not as a guaranteed lower bill. Your assessed value rising slower is good. But if your city bumps its millage two years from now, you could still pay more in total — just less than you would have without the cap. Both things can be true at once, and a landlord who budgets for "lower taxes" instead of "slower-growing assessments" is setting up a nasty surprise.

One more piece the cap can't reach: school taxes. The school-district portion is usually the single largest line on a Florida property-tax bill — commonly around a third of your total millage, though it varies by county — and the assessment cap has never applied to it. Your rental's school taxes get reassessed at full market value every January, 5% cap or not. So even in a year the cap kicks in, it only slows the county, city, and special-district share of your bill. That's real protection — but on part of the bill, not all of it.

What do landlords get wrong about this amendment?

Assuming the headline applies to rentals. The $250,000 exemption is for homesteads. Your rental gets the cap change and nothing else. Budget accordingly.

Banking the savings before November. It's a ballot measure that needs 60% to pass, and it doesn't take effect until January 1, 2027 even if it does. Don't price next year's rent around a tax cut that hasn't happened.

Forgetting the reset on purchase. If you buy in 2026 or 2027, your rental gets reassessed at full market value and the cap clock restarts. The benefit accrues to long-term holders, not fresh buyers — so factor a full-value assessment into your first-year numbers on any acquisition. And if you think your current assessment is already too high, the cap won't fix that — no ceiling on next year's increase repairs a base that is already wrong. That is the Reset Trap biting a recent buyer, and the cure is not a cap, it's an assessment appeal is for.

What should a Florida landlord do before November?

Four things, and only one of them is about the vote. The amendment is a 2027 question. Your 2026 tax bill is being decided right now, and the deadline that can actually cost you money lands in about four weeks.

- August — read your TRIM notice the day it arrives. Counties mail the Notice of Proposed Property Taxes in mid-to-late August. It shows the assessed value your rental will be taxed on and the millage each authority proposes. It is not a bill, so it gets ignored — and that is the mistake. It is the only document that tells you what is coming while you can still fight it.

- 25 days later — the appeal deadline, and it is unforgiving. Under FS 194.011(3)(d) a petition to the Value Adjustment Board must be filed with the clerk on or before the 25th day after your TRIM notice was mailed. Received, not postmarked — a petition that arrives on day 26 is late. Because counties mail on different dates, there is no statewide deadline: yours is printed on the notice. Our guide to appealing a Florida property assessment walks the filing. Miss it and you carry the wrong assessed value for a full year — and remember the Reset Trap: if you bought recently, this is the year your base was reset to market, which is exactly when an assessment is most likely to be wrong.

- September — the millage hearings. The cap limits your assessed value. It does nothing about the rate. With more than $8 billion coming out of local budgets in the amendment's first year, the rate is where counties and cities will look. The hearings are public and the dates are on your TRIM notice.

- November — you vote, and it needs 60%. A simple majority is not enough. If it fails, the 10% cap stays and nothing about your 2027 assessment changes.

If you own from out of state, two extra things. Your TRIM notice goes to the mailing address on file with the county property appraiser — if that is still the rental, the notice reaches your tenant and the 25-day clock runs without you. Confirm the address now, not in August. And you do not get a vote on this one. Your tenant might.

Plan for the bill you'll actually get

The smartest move isn't to wait on November — it's to model both outcomes now. Run your 2027 numbers with the current 10% cap and again with a 5% cap, so whichever way the vote goes, your rent and reserves already account for it. Property tax is one of the three expenses that quietly decide whether a Florida rental cash-flows, alongside insurance and maintenance, and the owners who forecast it accurately are the ones who don't get squeezed. Our guide to the property-tax basics for Florida rentals walks through how your bill is built, and the deductions most CPAs miss can offset what the cap doesn't.

If you'd rather have someone watch the assessment, the millage votes, and the renewal math for you, that's what we do. Start with a free rental analysis and we'll show you what your Orlando or Tampa property should earn — and what it should really cost to hold.