DSCR Loans for Florida Rental Investors: Qualify on the Property

A DSCR loan qualifies on the property's rent, not your paycheck or tax returns. Here's how it works for Florida investors—and why our insurance and taxes make the math tighter than you'd expect.

You found another Orlando rental worth buying. The numbers work. Then your lender asks for two years of tax returns, and your self-employed income—or your portfolio's depreciation—makes the file look ugly. Sound familiar?

Quick answer: A DSCR loan lets the property qualify itself. Instead of your W-2, pay stubs, or tax returns, the lender looks at one thing: does the rent cover the mortgage payment? That ratio is the DSCR—debt service coverage ratio. It's the workhorse loan for investors scaling a Florida portfolio, especially inside an LLC, and it's how a lot of self-employed and out-of-state buyers get to door number 11. The catch in Florida? Our property taxes and insurance live inside the payment, so they drag your ratio down in ways a lender in Ohio never thinks about.

Let's break down how it works, what it costs, and when it's the right tool.

What is a DSCR loan, and how does it work in Florida?

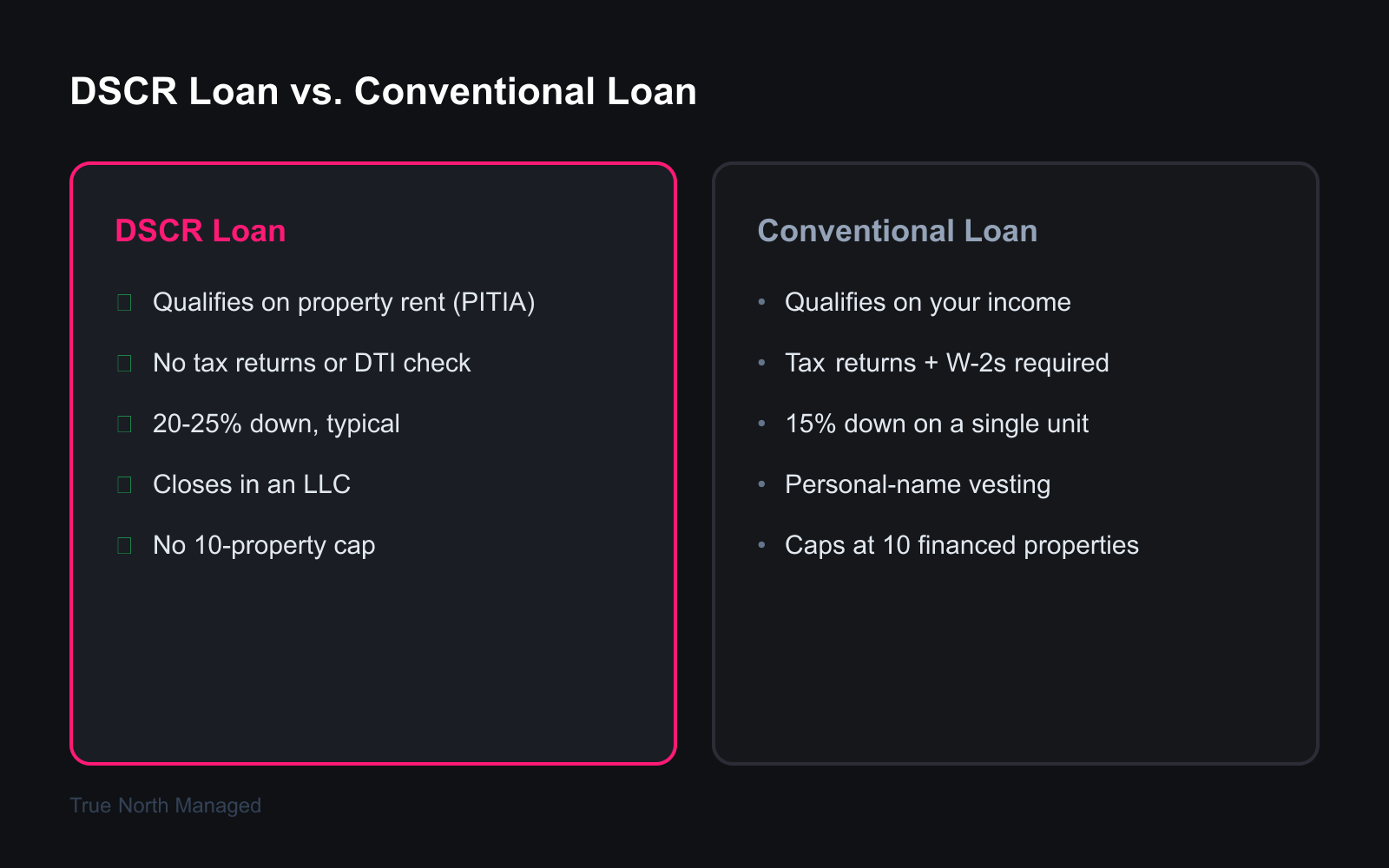

A DSCR loan is an investment-property mortgage that qualifies on the rental income the property produces, not on your personal income. No tax returns, no debt-to-income calculation, no employer verification. The lender confirms the rent covers the payment, checks your credit and reserves, and closes—often in the name of your LLC. Florida is one of the busiest DSCR markets in the country.

It's a non-QM loan, which just means it sits outside the standard Fannie Mae and Freddie Mac box. That's a feature, not a flaw. The conventional box was built for people buying a house to live in. You're buying an asset that pays its own way, and a DSCR loan treats it that way.

Three kinds of Florida investors lean on these loans hard:

- The self-employed buyer. You write off everything you legally can, so your tax return shows modest income. A conventional underwriter sees a thin file. A DSCR lender doesn't ask.

- The portfolio investor. Conventional financing caps you at 10 financed properties. DSCR loans have no such ceiling—you can keep buying, across multiple LLCs, as long as each deal pencils.

- The out-of-state owner. You live in New Jersey, you own three rentals in Tampa, and you'd rather not mail a stranger your tax returns. DSCR qualifies on the property and closes in your entity. Clean.

If you own one house you accidentally turned into a rental and you've got a steady W-2, a DSCR loan probably isn't your tool—a conventional loan will be cheaper. This is a loan for people building something.

How is the DSCR ratio actually calculated?

The DSCR is the property's rent divided by its full monthly payment. A ratio of 1.0 means the rent exactly covers the payment. Above 1.0, the property throws off a cushion. Below 1.0, you're covering a gap out of pocket. Most Florida lenders want to see 1.0 to 1.25, and a 1.25 usually unlocks the best rate and the most leverage.

Here's the formula in plain terms.

Formula: DSCR = Underwritten Gross Rent ÷ PITIA.

PITIA is the whole monthly payment: Principal, Interest, Taxes, Insurance, and Association dues (your HOA or condo fee). That last "I" and the "T" are where Florida bites—more on that below.

"Underwritten gross rent" isn't whatever number you wish you could charge. For a one-to-four-unit rental, the lender uses the lower of your actual signed lease or the appraiser's market-rent opinion, documented on a Form 1007 rent schedule. So if your lease says $2,300 but the appraiser says the market is $2,100, the lender runs the math on $2,100. (Bigger commercial buildings—five units and up—get scored on net operating income instead. For the single-family and duplex deals most Florida investors buy, it's gross rent over PITIA.)

What a lender wants to see:

- 1.25 or higher — strong. Best pricing, highest leverage.

- 1.0 to 1.24 — fine. The deal works; expect standard terms.

- Below 1.0 — the rent doesn't fully cover the payment. Some lenders still close it with a bigger down payment or a rate bump. In Florida, this comes up more than you'd think.

What does a DSCR loan look like on a real Florida rental?

A DSCR loan on a typical Orlando single-family rental often lands right around—or just under—1.0, because taxes and insurance eat into the payment. Run the numbers before you fall in love with a property. A deal that cash-flows on paper can still fail the ratio test if you ignore the full PITIA.

Let's walk through a real one.

Example: You're buying a $320,000 single-family home in east Orlando. You put 20% down ($64,000), so you finance $256,000 at a DSCR rate of 7.25% on a 30-year term.

- Principal and interest: $1,746/month

- Property taxes: about $293/month ($3,520/year at roughly 1.1% effective)

- Landlord insurance: about $200/month

- HOA: none on this one

That's a PITIA of $2,240/month. The home rents for $2,100/month—right in line with what east-Orlando single-family homes actually fetch (ZIP 32828 sat at $2,121 in April 2026 per Zillow's rent index).

DSCR = $2,100 ÷ $2,240 = 0.94.

It's below 1.0. Barely. And the reason is sitting right there in the payment: taxes and insurance add up to $493 a month. Strip those out and the loan portion alone is easy to cover. Add Florida's carrying costs back in, and the ratio slips under water.

What's good or bad? A 0.94 isn't a dead deal—plenty of Florida lenders will close a sub-1.0 with an adjustment. But you've got cleaner options. Put 25% down instead of 20% and the payment drops to about $2,131, pushing the DSCR to 0.99. Find $2,240 in rent and you hit a clean 1.0. Get to $2,800 in rent and you're at 1.25 with the best pricing on the board. Same house in coastal Tampa with $450/month insurance? The PITIA jumps to $2,490, and that $2,100 rent now scores a 0.84. Same property, worse ratio—just because of where the coast is.

This is the part of the math most out-of-state investors miss until they've already wired the deposit. The hidden carrying costs on a Florida rental aren't a rounding error. They're the difference between a loan that closes and one that doesn't.

Why do Florida's insurance and taxes hurt your DSCR?

Because both are baked into the payment the lender measures against your rent. Florida has some of the highest property insurance and a rising property-tax picture in the country, and every dollar of either one lands in the PITIA—which lowers your DSCR. A property that sails through underwriting in Georgia can choke on the ratio in Tampa.

Start with insurance. Inland landlord policies around Orlando run roughly $150 to $350 a month for a standard single-family rental. Move toward the coast and you're adding windstorm coverage, sometimes a separate flood policy, and the number climbs fast. That premium doesn't just hurt your cash flow—it sits inside PITIA and pulls your qualifying ratio down with it.

Then taxes. Your rental gets no homestead exemption, and Florida reassesses the property at full market value the year after you buy it. If the seller owned it for a decade behind an assessment cap, your tax bill can jump well past what they were paying. All of it flows into the "T" of PITIA.

So what do you do about it?

- Shop insurance before you close, not after. A newer roof can cut a premium 15–30%. The right policy can be the difference between a 0.96 and a 1.04.

- Look inland if the ratio is tight. Orlando, Lakeland, and inland Hillsborough carry lower insurance than the Gulf coast for otherwise similar homes.

- Buy the rate down or put more down. Both lower the payment, both raise the DSCR.

- Budget the real tax bill, not the seller's. Pull the reassessment math before you sign, not after the first tax bill lands.

Florida's carrying costs are also why our state shows up differently from a lot of others on a head-to-head rental-investment comparison. High insurance and reassessed taxes are the price of admission here. DSCR underwriting just makes that price impossible to ignore.

How much does a DSCR loan cost compared to a conventional loan?

A DSCR loan costs more than a conventional mortgage—you trade some price for the no-income-docs convenience and the LLC flexibility. Expect a rate roughly half a point to a point and a half above conventional, higher closing costs, a reserve requirement, and often a prepayment penalty. For the right investor, the trade is worth it. For others, it's not.

Here's what to budget for, with the usual caveat that every number below is a typical range, not a quote—DSCR terms swing by lender, credit, and the deal itself:

- Down payment: typically 20–25% (sometimes 30% on a thin DSCR or a high loan amount).

- Credit: most lenders want a 640–660 floor; 700-plus gets you better terms; 740-plus gets the best pricing.

- Rate: generally 0.5 to 1.5 points above conventional. In mid-2026 that's put many DSCR rates in the 6.25–8.0% range against a conventional 30-year averaging around 6.5%.

- Closing costs: often 1.5–3% of the loan amount—a bit steeper than conventional.

- Reserves: commonly 3–6 months of PITIA in the bank after closing.

- Prepayment penalty: very common, usually a 5-4-3-2-1 step-down. Pay the loan off in year one and you owe 5% of the balance; year two, 4%; and so on until it disappears after year five. Accepting a longer penalty period usually buys you a lower rate.

- Interest-only option: many lenders offer an interest-only stretch (often the first 10 years), which lowers the payment and can rescue a tight DSCR.

Now the conventional side. A Fannie Mae investment loan needs as little as 15% down on a single-unit rental—but it wants your tax returns, your W-2s, a debt-to-income ratio under the line, and it stops cold at 10 financed properties. If you've got a clean W-2 and you're buying your first or second rental, conventional is usually cheaper, and you should take it.

The choice looks a lot like the HELOC-versus-cash-out-refi decision: there's no universally "best" loan, only the right tool for where you are. DSCR earns its premium when conventional won't work or won't scale.

When is a DSCR loan the right tool for your Florida portfolio?

A DSCR loan is the right tool when the property qualifies but you don't—or when you've outgrown conventional financing. If you're past 10 properties, buying in an LLC, self-employed with a lean tax return, or managing from out of state, this is your loan. If you qualify conventionally with room to spare, it usually isn't.

The green lights:

- You've hit the 10-property conventional cap. DSCR has no limit. This alone sends most serious investors here eventually.

- You're buying in an LLC. DSCR closes in the entity, which is exactly what you want if you've set up an LLC to hold your Florida rentals. Conventional usually forces personal-name vesting.

- Your income is hard to document. Self-employed, 1099, heavy write-offs, or income that's real but messy on paper.

- You're investing from out of state. No income docs and entity vesting make remote buying far simpler.

The red lights:

- You're flipping or selling soon. That 5-4-3-2-1 prepayment penalty can take a real bite if you exit in year one or two.

- The DSCR is thin and the property is coastal. A 0.95 on a Gulf-coast house with rising insurance is a deal that gets harder every renewal.

- You qualify conventionally and you're not scaling. Don't pay the DSCR premium for convenience you don't need.

Common mistakes Florida investors make with DSCR loans

A few errors show up again and again. Most are avoidable if you run the full math before you make an offer.

- Underestimating Florida insurance in the PITIA. Investors plug in a national-average premium and get a nasty surprise at underwriting. Get a real quote on the actual property before you assume the ratio.

- Taking a long prepay penalty on a property you'll flip. The lower rate looks great until you sell in year two and hand back 4% of the balance. Match the prepay term to your hold plan.

- Assuming a sub-1.0 is an automatic decline. It's not. Many Florida lenders will close a 0.90s deal with more down or a rate adjustment. Ask before you walk.

- Forgetting the reserve requirement. You scraped together the down payment and closing costs—then the lender wants six months of PITIA sitting in the bank too. Plan for it early.

- Skipping the rate-versus-prepay trade. A longer penalty can shave a point off your rate. On a buy-and-hold you never plan to sell, that's close to free money. Run both versions.

The bottom line

A DSCR loan flips the question every investor dreads. Instead of "can you prove your income," it asks "does this property pay for itself." For Florida investors building a portfolio—especially in an LLC, especially past the conventional cap—that's the loan that keeps the buying going. It costs a little more, it usually carries a prepayment penalty, and it asks for real reserves. In exchange, the property qualifies itself and your tax returns stay in the drawer.

Just respect the Florida math. Our insurance and reassessed taxes live inside the payment the lender measures, so a deal that pencils everywhere else can land under 1.0 here. Run the full PITIA—taxes, insurance, the works—before you write the offer. For the bigger picture on financing and holding Florida rentals, the Florida Owner's Guide pulls the pieces together.

If you're buying in Orlando or Tampa and you want a second set of eyes on the numbers—real rent, real taxes, real insurance, and what your DSCR would actually be—a free rental analysis is a good place to start. We run these for investors weighing their next door. No pressure, just clarity on whether the deal works.