The Florida Landlord Tax Deductions Most CPAs Miss

Most Florida landlords with 1–4 units leave $3,000–$8,000 in deductions on the table every year. Here are the five most commonly missed — and the Florida-specific rules your CPA probably doesn't know about.

The Florida Landlord Tax Deductions Most CPAs Miss

You filed your return. You claimed mortgage interest, property taxes, and a few repair receipts you remembered to save. Your CPA nodded, ran the numbers, and moved on to the next client.

And you probably left $3,000–$8,000 on the table.

It's not that your CPA is bad at their job. It's that most tax professionals handle a mix of W-2 employees, small business owners, freelancers, and a handful of landlords. Rental property tax law has specific rules that don't apply to any other asset class — and unless your CPA specializes in real estate, they're likely applying general rules to a situation that has very specific ones.

Here are the five deductions Florida landlords with 1–4 units miss most often — and why they matter more than you think.

Want the full reference? Download the Florida Landlord Tax Cheat Sheet — every deduction on one page, a repairs-vs-improvements guide, and a fill-in depreciation worksheet you can hand to your CPA.

What Depreciation Deduction Are Most Florida Landlords Missing?

Depreciation is the single largest legal deduction available to rental property owners, and it doesn't require you to spend a dollar. The IRS lets you deduct a portion of your building's value every year for 27.5 years — reflecting the building's theoretical wear and tear, even while it appreciates in market value.

Here's a worked example with Florida numbers:

- Purchase price: $350,000

- Land value (from county tax assessment): $70,000

- Depreciable basis: $280,000

- Annual deduction: $280,000 ÷ 27.5 = $10,181/year

That's over $10,000 knocked off your taxable rental income every single year. At a 24% tax rate, it saves you $2,443 annually. At 32%, it's $3,258.

The most common mistake: not claiming depreciation at all, or depreciating the full purchase price (including land). Land is never depreciable. Your county property appraiser's website shows the land/improvement split — Orange County at ocpafl.org, Hillsborough at hcpafl.org.

For properties worth $500K+: Ask your CPA about a cost segregation study. This engineering-based analysis reclassifies 20–40% of your building's cost into shorter-life assets (5, 7, or 15 years). With 100% bonus depreciation restored through 2029 under the One Big Beautiful Bill Act, those reclassified amounts can be deducted in full in year one. Studies cost $5,000–$20,000 but typically return 5:1 to 25:1 in tax savings. For a deeper walkthrough of how this works with Florida properties, see our Florida depreciation tax guide.

Are You Tracking Mileage to Your Rental Properties?

The 2026 IRS standard mileage rate is 72.5 cents per mile. That sounds small until you do the math.

If you drive to your rental property once a week — a 15-mile round trip — that's 780 miles per year. At 72.5¢, you're looking at a $565 deduction. Own two properties? Double it. Make extra trips for contractor meetings, tenant showings, and hardware store runs? You could be looking at $1,000–$2,000 in deductions from mileage alone.

But there's a catch: the IRS requires a contemporaneous mileage log. Not a log you reconstruct in April when your CPA asks for it — a log you write on the day you drive. Date, starting location, destination, miles, and business purpose. No log, no deduction. Period.

The home office shortcut most landlords miss: If you use a dedicated space at home exclusively for rental management — bookkeeping, tenant communication, lease review — your home qualifies as your principal place of business. That means every trip from home to a rental property is a deductible business trip, not a commute. Without the home office designation, trips from home to a single rental are technically commuting miles and aren't deductible.

For a complete walkthrough of what's deductible on Schedule E, check our rental tax deductions checklist for Florida landlords.

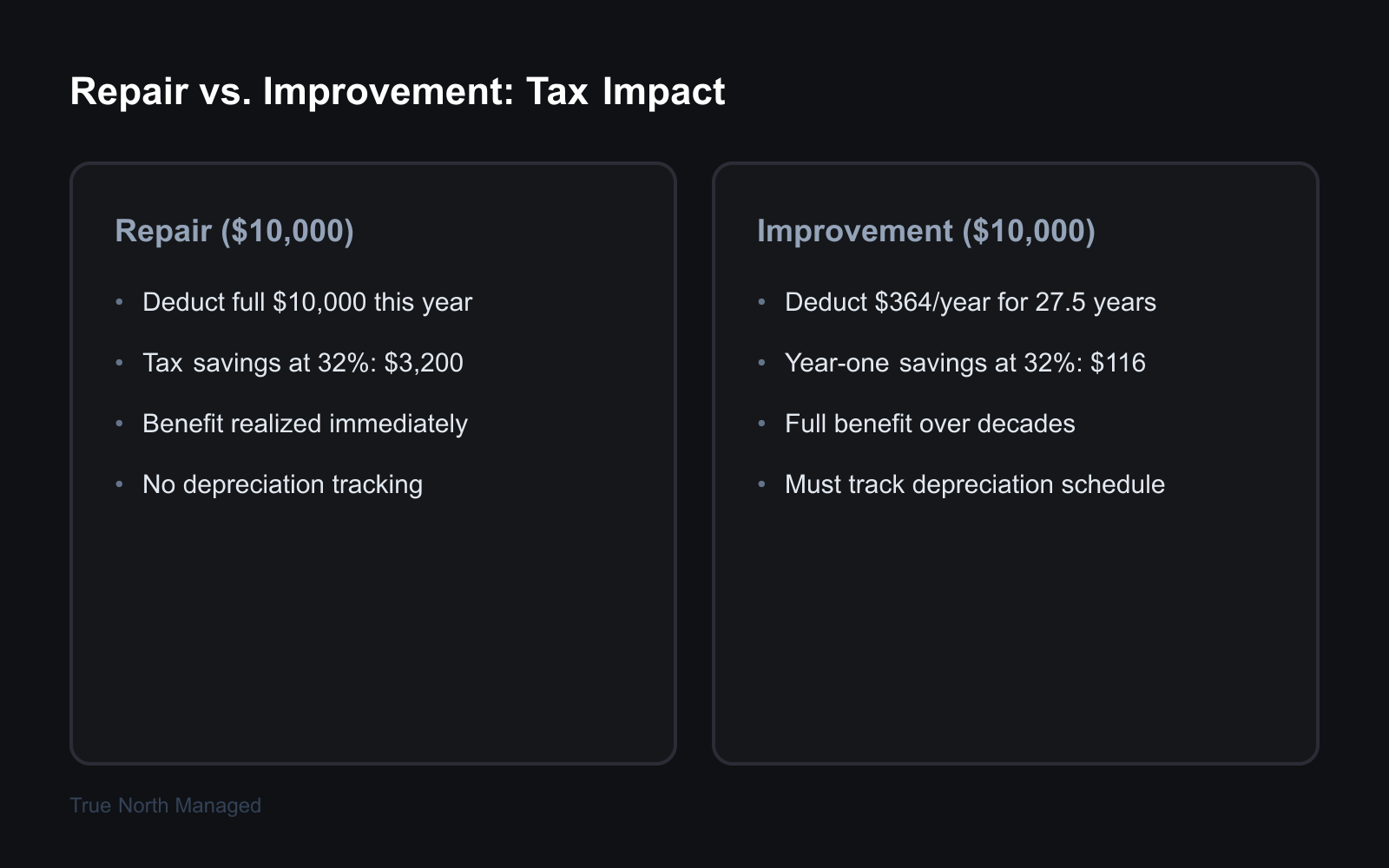

Does Your CPA Know About the De Minimis Safe Harbor?

Here's the rule: any single expense of $2,500 or less can be deducted immediately as a repair — even if it would technically qualify as an improvement under normal IRS rules. This is the De Minimis Safe Harbor election (Treas. Reg. § 1.263(a)-1(f)).

In practice, this means:

- A $2,400 refrigerator? Current-year deduction.

- A $1,800 water heater? Current-year deduction.

- Ten $800 items across your properties? $8,000 deducted this year.

Without this election, your CPA might default to capitalizing each appliance and depreciating it over 27.5 years — giving you roughly $87/year instead of $2,400 this year. On a $2,400 item at a 24% tax rate, that's a difference of $555 in year-one tax savings versus $21.

The catch: you must file a written election with your tax return each year to claim the safe harbor. It's a one-line statement on your return, but if it's not there, the IRS can recharacterize your deduction.

The cousin rule most people miss: The Routine Maintenance Safe Harbor says any maintenance activity you'd expect to perform at least twice in 10 years is automatically a deductible repair — regardless of cost. HVAC servicing, exterior painting on a 5-year cycle, carpet replacement, gutter cleaning — all deductible as repairs.

Our Florida landlord tax guide breaks down how these safe harbors interact with the standard repair-vs-improvement rules.

What Florida-Specific Tax Rules Does Your CPA Need to Know?

Florida has no state income tax. That's the good news — your rental income is taxed only at the federal level. But Florida has three tax traps that national CPAs consistently miss:

1. Homestead exemption risk. If you're converting your primary residence to a rental, this is the biggest financial risk you face. Florida's homestead exemption provides up to $50,000 in property tax savings plus the Save Our Homes cap that limits annual assessment increases. If you rent out the property "all or substantially all" for more than 30 days per year for two consecutive years, the county can revoke the exemption retroactively. Penalties include up to 10 years of back taxes, a 50% penalty per year, and 15% interest (FL Stat. § 196.061). Contact your county property appraiser before you list a homesteaded property for rent.

2. Tangible personal property (TPP) tax. Appliances, furnishings, and equipment in your rental units are taxable personal property in Florida. You must file Form DR-405 with your county property appraiser by April 1. The first $25,000 is exempt — but only if you file on time. Miss the deadline and you lose the exemption and face a 25% penalty. Many landlords don't know this filing exists.

3. Documentary stamp tax on deed transfers. If you transfer your rental property to an LLC, you'll owe $0.70 per $100 of property value in documentary stamp tax (FL Stat. § 201.02). On a $300,000 property, that's $2,100. Factor this into any entity restructuring decisions.

Are You Filing 1099s for Your Contractors?

If you paid any unincorporated contractor $600 or more during the year — plumber, handyman, painter, lawn service — you're required to file a 1099-NEC by January 31. Not filing can result in penalties starting at $60 per form, and the IRS can disallow the deduction for the expense itself if you can't prove you met the reporting requirements.

The fix is simple: collect a W-9 from every contractor before you pay them the first time. Track payments by contractor throughout the year. On January 31, file 1099-NEC forms with the IRS and send copies to each contractor.

Who's exempt: Contractors organized as corporations (Inc., Corp., LLC taxed as S-Corp or C-Corp) generally don't need a 1099. Sole proprietors, partnerships, and single-member LLCs do. The W-9 tells you — look for the entity type in Box 3.

Florida landlords who self-manage tend to miss this more than those with property managers, because PM companies handle 1099 filing for their vendors. If you're self-managing and paying contractors directly, this is on you.

Tax season doesn't have to mean guessing. The deductions are specific, the rules are documented, and the money is real. The difference between a $2,000 tax bill and a $200 one is often just knowing which boxes to check.

Download the Florida Landlord Tax Cheat Sheet — every Schedule E deduction on one page, a repairs-vs-improvements table with 10 examples, a fill-in depreciation worksheet, and the full deadline calendar. Print it, hand it to your CPA, and stop leaving money on the table.

If you want a property manager who tracks every expense, categorizes every receipt, and hands you a clean annual statement ready for Schedule E — get a free rental analysis and see what professional management looks like for your property.