Fire Damage in a Florida Rental: Who Pays and What Happens to the Lease

A fire just hit your Florida rental. Does the lease end? Who pays to rebuild? Here's how FL Statute 83.63 splits the call — and why your insurance, not your tenant's, fixes the structure.

You get the call you never want. There's been a fire at your rental. Once you know everyone's safe, two questions hit you at the same time: who pays to fix this, and is the lease still good? Fire damage in a Florida rental sits at the messy crossroads of insurance and landlord-tenant law, and the answers aren't always what landlords expect.

Quick Answer

Fire damage in a Florida rental splits along two lines. Your property insurance rebuilds the structure — not your tenant's policy. And Florida Statute 83.63 decides the lease: if the casualty makes the unit unlivable, your tenant can terminate and walk; if only part is damaged, they can vacate that part and pay reduced rent. Cause matters too. Let's break down both questions.

Who pays to repair fire damage in a Florida rental?

You do — your property policy, anyway. The landlord's dwelling coverage rebuilds the structure after a fire. Your tenant's renters insurance covers their belongings, not your building. The cause of the fire changes who can recover money later, but it doesn't change your baseline duty to restore a habitable unit.

Fire restoration isn't cheap. Nationally, fire damage restoration averages around $11,900, with most jobs landing between $3,000 and $40,000. Figure $4 to $6.50 per square foot, so a 2,000-square-foot house runs roughly $8,000 to $13,000 to put right. Smoke and soot cleanup adds $200 to $1,200 per room. Then there's the water the fire department leaves behind — another few thousand to dry out and repair. A small kitchen fire might cost a few thousand. A unit gutted to the studs runs well into the tens of thousands.

Your obligation to keep the property livable doesn't disappear because the cause was bad luck — or even the tenant. Florida Statute 83.51 requires you to maintain roofs, exterior walls, floors, and plumbing in good repair and keep the unit up to code. A fire that compromises any of that triggers your duty to repair. Even if the tenant's unattended skillet started the blaze, the structure is still yours to restore. What changes with cause is your right to chase reimbursement afterward — more on that below.

The same cause-based logic shows up in other disasters. Our guide on who pays for water damage in a Florida rental walks through the same fault analysis for burst pipes and roof leaks. Fire follows the same map: trace the source, then sort out the money.

Does the lease end after a fire in Florida?

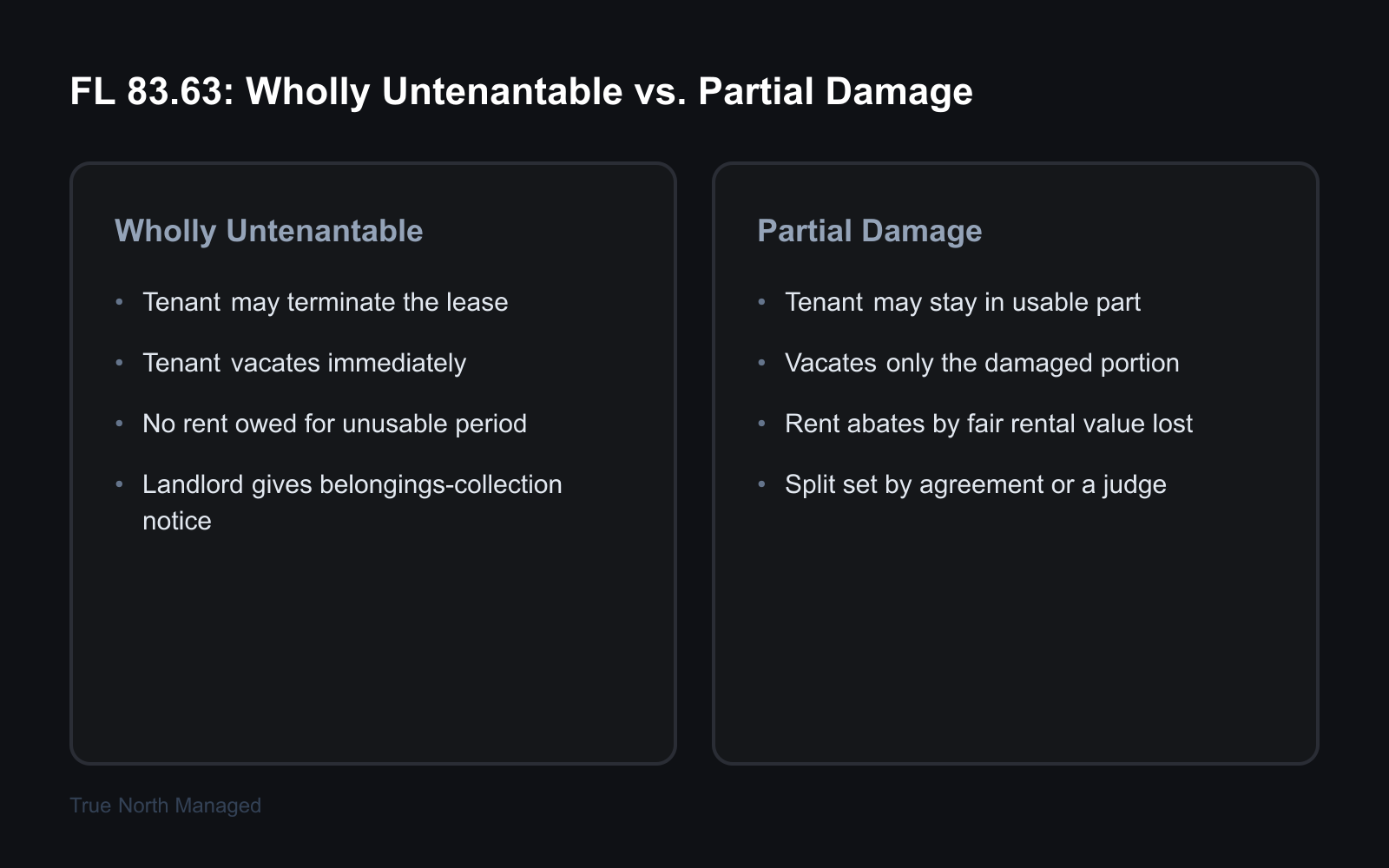

Sometimes. Florida Statute 83.63 gives the tenant the call, and it forks two ways. If the casualty wasn't the tenant's fault and it substantially impairs their enjoyment of the unit, the tenant may terminate the rental agreement and move out immediately. Or, if part of the unit is still usable, they can vacate the damaged part and pay rent reduced by the fair rental value of what they lost.

That's the whole framework, and it's worth sitting with. The statute doesn't hand the decision to you. It hands it to your tenant.

The unit is wholly untenantable. A fire that takes out the kitchen, the wiring, and half the roof leaves nothing livable. Under 83.63, the tenant can end the lease and leave — no rent owed for the period they can't use the place. You also have to give them a safe chance to collect their belongings, or written notice of when they'll be able to, within a reasonable time. That's not optional courtesy. It's in the statute.

The unit is partially damaged. Say the fire scorched one back bedroom but the rest of a three-bedroom house is fine. The tenant can keep living there and pay less. The rent drops by the fair rental value of the unusable part. If that bedroom and bath are worth, roughly, a third of a $2,100/month house, the tenant's rent falls to about $1,400 while you repair it. The exact split usually comes down to a conversation between you and the tenant — and if you can't agree, a judge sorts it out.

Here's the thing most landlords miss. The trigger is "other than by the wrongful or negligent acts of the tenant." If your tenant caused the fire through negligence, the 83.63 termination-and-walk option doesn't shield them the same way. They don't get to torch the kitchen and exit the lease clean.

Do you have to rebuild after a fire in Florida?

Maybe — and your lease decides a lot of it. If the unit is completely destroyed, the lease usually ends and nobody's rebuilding to honor a dead contract. Partial damage is murkier. Florida law isn't crisp here, so the language in your lease is what controls.

This is where a casualty or condemnation clause earns its keep. A good Florida lease says something like: if the premises are destroyed or condemned by fire, flood, or other casualty, the lease terminates as of the date of destruction. With that clause, you and the tenant both have a clean exit on a total loss. Without it, you can land in an ugly spot — the habitability duty keeps pulling you toward repair, even while a tenant is technically still entitled to occupy a half-burned house. Try coordinating a gut renovation around someone living in the building. It doesn't work.

So even when the tenant caused the fire, you're not off the hook for the structure. The repair obligation and the question of who pays for it are two different things. You restore the unit. Then you go figure out recovery.

What does insurance actually cover after a rental fire?

Three policies, three jobs. Your landlord dwelling policy rebuilds the structure. Your loss-of-rent coverage replaces the rent while the unit sits empty. The tenant's renters insurance covers their belongings and their hotel bill. Knowing which policy does what keeps you from paying for something that isn't yours to pay.

Start with loss of rent. When a covered fire makes your unit uninhabitable, fair rental value coverage reimburses the rent you'd have collected during repairs. It's typically capped at 20% of your dwelling coverage limit and pays for up to 12 months, or until the repair's done, whichever comes first. So a $300,000 dwelling policy carries roughly $60,000 in lost-rent protection. What it won't cover: your mortgage, your property taxes, your utilities — the bills that keep coming whether or not a tenant lives there. Budget for those out of pocket.

Now the tenant's side. The landlord's policy does not cover the tenant's furniture, electronics, or clothes — never has, never will. That's what renters insurance is for. A standard renters policy covers a tenant's belongings against fire and pays Additional Living Expenses, the cost of a hotel or short-term rental while they're displaced, often a set percentage of their personal-property limit. The Insurance Information Institute guide to renters insurance lays out exactly what those policies include. If your lease requires renters insurance — and it should — a displaced tenant has somewhere to land that isn't your wallet.

When are you on the hook for the tenant's losses? When the fire was your fault. Bad wiring you knew about and never fixed. A smoke detector you never installed. Landlord negligence like that can make you liable for the tenant's damaged belongings and their displacement costs. Keep up with maintenance and that exposure stays small. For the full picture on coverage gaps, our landlord insurance guide for Florida rentals breaks down what to carry.

Can you recover from a tenant who caused the fire?

It depends on your lease — and Florida is unusual here. In a lot of states, a tenant is treated as a co-insured under the landlord's fire policy, which blocks the insurer from coming after them. That's the "Sutton Rule." Florida rejects it. Florida courts read the lease to decide who carries the risk of loss for the tenant's negligence. If your lease shifts that risk to you or your insurer, the tenant is treated as a co-insured and there's no subrogation. If it doesn't, your insurer may be able to pursue the negligent tenant after paying your claim.

Translation: don't assume either way. Whether you — or your carrier — can recover from a tenant whose grease fire gutted the kitchen turns on what your lease says about insurance and risk of loss. This is a question for your agent and, if the loss is big, an attorney. It's also a reason to have a real lawyer draft your lease instead of grabbing a free template online.

If the casualty ends the lease, the security deposit still has to be handled by the book. Florida Statute 83.49 gives you 30 days from termination to send a written claim notice by certified mail if you're keeping any of the deposit, or 15 days to return it in full if you're not. Miss the 30-day window and you forfeit the claim. The same documentation rules that apply when a tenant damages your property apply here — photos, invoices, itemized deductions. A fire doesn't suspend the deposit statute.

What should you do in the first 48 hours?

Move fast and in order, even from out of state. Secure the property, document the damage, notify your insurer, give the tenant the 83.63 belongings notice, and decide the lease question. You can run most of this from a thousand miles away with the right people on the ground.

- Make sure everyone's safe and the property's secured. Board up openings, shut off utilities at the source, keep people out of unsafe areas. A local property manager or a board-up service handles this if you're not in town.

- Photograph and video everything before cleanup starts. Every room, every angle, timestamped. You'll need it for the claim and for any deposit accounting later.

- Call your insurer the same day. Open the claim, get the adjuster scheduled, and ask specifically about your loss-of-rent coverage. Don't start major repairs before the adjuster sees the loss.

- Give your tenant the 83.63 notice. Either let them collect belongings when it's safe, or send written notice of the date they can — within a reasonable time. Put it in writing.

- Decide the lease. Is the unit wholly untenantable or partially usable? That answer drives whether the tenant terminates or stays at reduced rent, and whether you're rebuilding or releasing the tenant.

A restoration company should start water extraction and smoke remediation within a day or two — fire-soaked drywall and Florida humidity are a mold problem waiting to happen. The longer it sits, the bigger the bill. If you manage remotely, this is exactly the moment a boots-on-the-ground manager pays for itself. For the broader playbook on running a Florida rental, our owner's guide pulls the pieces together.

Common mistakes landlords make after a fire

Assuming the tenant pays without checking the cause. A fire that started in your old wiring is your problem. One the tenant caused through negligence is a different conversation — but you still have to trace it, document it, and check what your lease and insurer allow before you point fingers.

Renting without a casualty clause in the lease. This is the quiet one that wrecks landlords. No termination-for-casualty language means you can get stuck owing repairs on a unit a tenant still has the right to occupy. Get the clause in before you need it.

Not requiring renters insurance. A displaced tenant with no renters policy looks to you for their belongings and their hotel. A tenant with coverage looks to their own carrier. Require it in the lease and confirm it stays active.

The Bottom Line

A fire splits into two questions, and Florida law answers both. Statute 83.63 decides the lease — wholly untenantable means the tenant can walk; partial damage means they pay less while you repair. Your insurance, not the tenant's, rebuilds the structure and replaces the rent. Trace the cause, lean on your lease, and handle the deposit by the statute if the lease ends.

Recovering from a fire is stressful enough without guessing at the rules. If you'd like a second set of eyes on your lease, your coverage, or the response when something goes wrong, our free rental analysis includes a real conversation about your property and your goals. We're here to help.