Cost Segregation for Florida Rental Properties: Is It Worth It?

A cost-segregation study can move years of depreciation into your first year of ownership. But it isn't for every Florida landlord. Here's the honest math on when it pays and when it doesn't.

If you own a higher-value rental in Orlando or Tampa, someone has probably mentioned cost segregation to you, usually a CPA or a guy at a real estate meetup who got very excited about it. The pitch sounds too good to ignore: take years of future tax deductions and pull them into your first year of ownership.

Here's the honest version. Cost segregation on a rental property in Florida is real, it's legal, and for the right property it can save tens of thousands in federal tax. It's also oversold, misunderstood, and flat-out wrong for plenty of landlords. This guide breaks down what it actually does, when the study pays for itself, the Florida-specific angle, and the catch nobody puts in the brochure: depreciation recapture.

If you're still fuzzy on how rental depreciation works in the first place, start with our Florida rental depreciation guide. This post assumes you've got the basics and want to know whether to accelerate.

What is cost segregation for a rental property?

Cost segregation is an engineering-based study that breaks your building into shorter-life components so you can depreciate them faster. Instead of writing off the whole building over 27.5 years, you carve out the parts that wear out sooner, appliances, flooring, fencing, landscaping, and depreciate those over 5, 7, or 15 years instead.

Normally, the IRS makes you depreciate residential rental property on a 27.5-year straight-line schedule, claiming about 3.636% of your building's value each year (land never depreciates). That's the baseline in IRS Publication 946, the rulebook for depreciating property.

A cost-seg study doesn't change the total amount you get to deduct. It changes the timing. Think of it less like finding a new deduction and more like borrowing your own deductions from the future and spending them now. We call this "The Front-Loaded Depreciation Trade," and the word trade matters, because what you pull forward, you may owe back later.

A qualified study, the kind the IRS Cost Segregation Audit Techniques Guide actually respects, uses an engineer to walk the property, read the construction records, and assign costs to each component. Most studies reclassify somewhere between 20% and 35% of the building's cost into those shorter-life buckets. The rest stays on the slow 27.5-year track.

How does cost segregation work with bonus depreciation?

Bonus depreciation is what turns cost segregation from "modestly helpful" into "potentially huge." Right now, qualifying property gets 100% bonus depreciation, meaning the entire short-life portion a study identifies can be written off in year one.

This is the part where timing matters, so read carefully. Under the One Big Beautiful Bill Act, the IRS confirmed a permanent 100% first-year bonus depreciation for qualified property acquired after January 19, 2025. The official IRS guidance on the OBBBA bonus rules (Notice 2026-11, released January 14, 2026) spells it out.

That's a reversal of the old schedule. The 2017 tax law had bonus depreciation phasing down, 40% in 2025, 20% in 2026, gone by 2027. If you read an older article quoting those numbers, it's stale. For property you buy now, the current rule is 100%, and it's permanent. (Property acquired on or before January 19, 2025 stays under the old phase-down, and there's an election to take 40% instead of 100% in the first year. That's a CPA conversation.)

Here's why this pairs so well with a study: bonus depreciation applies to property with a recovery period of 20 years or less, exactly the 5-, 7-, and 15-year components a cost-seg study pulls out of your building. The study finds the short-life assets; bonus depreciation lets you deduct all of them at once.

What does cost segregation look like in real numbers?

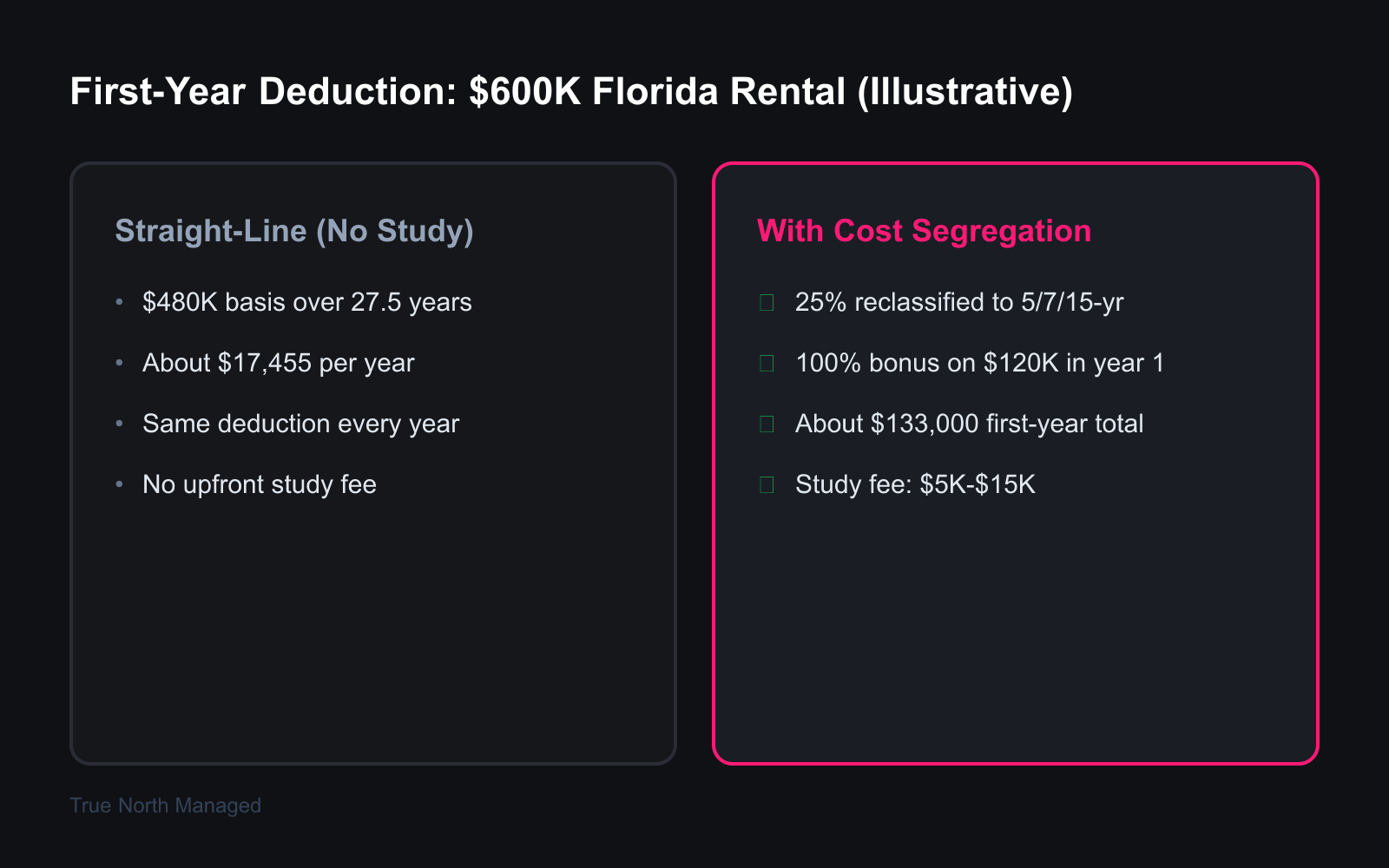

For a $600,000 rental with $480,000 of depreciable basis, a study can turn a roughly $17,000 first-year deduction into something north of $130,000. The acceleration is dramatic, but it's a shift, not free money.

Let's walk through it. These numbers are illustrative, rounded for clarity, not a real client and not a promise about your property. Your actual results depend on the study, your basis, and your tax situation.

Say you buy a $600,000 small multi-family in Orlando. Land is worth $120,000 (not depreciable), so your depreciable basis is $480,000.

- Straight-line, no study: $480,000 ÷ 27.5 ≈ $17,455 per year. Same deduction, year after year.

- With cost segregation: the study reclassifies 25%, $120,000, into 5/7/15-year property. With 100% bonus depreciation, that entire $120,000 is deductible in year one. The remaining $360,000 of structure keeps depreciating over 27.5 years (about $13,091/year). First-year deduction: roughly $133,000.

That's about $115,000 of extra deductions in year one versus straight-line. At a 32% federal marginal rate, that's around $36,800 of federal tax deferred, against a study fee that typically runs a few thousand to maybe ten thousand dollars. On paper, the return is obvious.

The catch words are "deferred" and "on paper." Two things decide whether you actually see that benefit: whether you can use the deduction this year, and what happens when you sell.

Can I actually use the deduction? The passive loss trap

For most landlords, that giant year-one deduction is a passive loss, and passive losses can't offset your W-2 salary. They sit suspended until you have passive income or you sell. This is the single most common reason a cost-seg study disappoints.

The IRS treats rental real estate as a passive activity by default. A passive loss can only offset passive income, other rental profits, for example. It can't reduce your wages, your business income, or your stock dividends. So if your $600,000 rental throws off a $115,000 paper loss but you have no other passive income, that loss doesn't vanish, but it doesn't help you this year either. It carries forward.

There are two real exits, and both have strict rules:

- Real Estate Professional Status (REPS). If you spend more than 750 hours a year in real property work, and that's more than half your total working time, your rental losses can become non-passive. For someone with a full-time W-2 job, this is nearly impossible to claim honestly. For a full-time investor or a spouse who manages the portfolio, it can work.

- The short-term rental path. If your average guest stay is seven days or less and you materially participate (often 100+ hours a year), the activity may fall outside the "rental" definition entirely, which can make the loss non-passive, deductible against ordinary income including W-2 wages. This is why cost segregation gets talked about so much in the Airbnb and vacation-rental world around Orlando's theme-park corridor and the Gulf beaches.

I'm being deliberately careful here. These rules are real but fact-specific, and the IRS scrutinizes them. Don't structure a six-figure deduction off a blog post. Get a CPA who does this for a living to confirm your situation first.

What's the catch? Depreciation recapture on sale

When you sell, the IRS wants some of those accelerated deductions back, and the components a study reclassified get taxed at higher ordinary-income rates instead of the gentler 25% real-estate rate. That's the back end of the front-loaded trade.

Depreciation recapture works in two buckets:

- Section 1250 covers the building structure itself, the 27.5-year stuff. On sale, the depreciation you took here is "unrecaptured 1250 gain," taxed at a maximum federal rate of 25%.

- Section 1245 covers personal property, the 5- and 7-year components your study pulled out. This gets recaptured at your ordinary income rate, which for a high earner can run well above 25%.

See the problem? Cost segregation moves a chunk of your building out of the 1250 bucket (max 25% recapture) and into the 1245 bucket (ordinary rates). You got a bigger, earlier deduction, but you may pay a higher rate on it when you sell. For a landlord in a top bracket who sells quickly, the math can partially unwind.

Two things soften this. First, time value of money still favors you, a deduction today is worth more than the tax bill years from now. Second, a 1031 exchange on a Florida rental can defer the recapture entirely if you roll the proceeds into another property. Many investors who use cost segregation aggressively plan to 1031 their way out rather than ever triggering recapture.

Why does Florida make cost segregation more attractive?

Florida has no state income tax, so every dollar of federal depreciation you claim is a dollar you keep, with no state add-back clawing part of it back. The benefit is federal-only, and that's a feature, not a limitation.

In a state like California or New York, a landlord faces both federal and state income tax, and some states force you to add depreciation back or recapture it at the state level too. Florida landlords skip all of that. There's no Florida income tax line, no state recapture, no state add-back. Whatever federal benefit your study produces, you keep 100% of it.

This is the same logic that makes Florida attractive for rental investing generally, and it's worth understanding alongside the basics of how rental income is taxed in Florida. Cost segregation simply concentrates the federal benefit, which in a no-state-tax state is the whole benefit.

One more Florida-flavored point: a lot of our coastal and theme-park-adjacent inventory runs as short-term rentals. That STR designation, as covered above, is often the cleanest route to actually using accelerated depreciation against ordinary income. The strategy and the local market fit together here in a way they don't in much of the country.

When is cost segregation on a rental property in Florida worth the cost?

A study is usually worth it when your depreciable basis is above roughly $300,000, you'll hold the property at least five years, and you have a way to actually use the deduction. Below that, the fee often eats the benefit.

Engineering-based studies typically run $5,000 to $15,000, depending on property size and complexity. Some firms now offer cheaper algorithm-driven studies for smaller residential properties, but the IRS audit guide gives the most weight to a detailed engineering study performed by someone who understands both construction and tax law. On an audit, that distinction matters.

Cost segregation tends to pay off when:

- Your depreciable basis is $300,000+ (many pros consider $500,000+ a strong candidate).

- You plan to hold for 5+ years, so recapture is far off and time value works in your favor.

- You have passive income, REPS, or a qualifying short-term rental to absorb the loss.

- You're in a high marginal bracket, where the deduction is worth more.

- You bought the property recently, or want to do a look-back study (more on that below).

Who should not bother with cost segregation?

If you own one accidental rental, you're in a low tax bracket, or you might sell within a few years, skip it. The study fee will likely cost more than it saves you.

This is the section the property-management firms pushing cost segregation tend to leave out, so let me say it plainly. Cost segregation is the wrong move for:

- The single-property accidental landlord. If you relocated, couldn't sell your house, and now rent it out, your property value is probably modest, your tax bracket may be ordinary, and you have no passive income to absorb a big loss. A $5,000 study to generate a suspended deduction you can't use is money lit on fire.

- Anyone selling soon. Sell within five years and recapture claws back much of the benefit at ordinary rates. The juice isn't worth the squeeze.

- Low-bracket owners. A deduction is only as valuable as the rate it offsets. In a 12% or 22% bracket, the savings shrink fast.

- Sub-$300K properties. The reclassified portion is too small to clear the study fee.

If that's you, you're better off claiming the everyday deductions you're already entitled to. We cover those in our breakdown of the Florida landlord tax deductions most CPAs miss.

What if I already own the property?

You don't have to do a study the year you buy. A look-back study lets you catch up missed acceleration on your current return without amending old ones, using IRS Form 3115 and a Section 481(a) adjustment.

This surprises a lot of landlords. If you bought an Orlando duplex three years ago and never did a study, you haven't lost the chance. A look-back study quantifies the depreciation you should have accelerated, and a Section 481(a) adjustment lets you claim that catch-up amount in the current tax year, all at once. You file Form 3115 to make the accounting-method change. No amended returns required, the IRS specifically wants you to use Form 3115 rather than reopen prior years.

For a property that's appreciated and where you've got a way to use the deduction, a look-back study can be even more powerful than doing one at purchase, because you're catching up several years of acceleration in a single year.

The bottom line on cost segregation in Florida

Cost segregation is a timing strategy, not a magic deduction. For a higher-value Florida rental, held long-term, owned by someone who can actually use the loss, it can defer serious federal tax, and in a no-state-income-tax state, you keep all of it. For a single modest rental held by a W-2 earner in a middle bracket, it's usually an expensive mistake.

The honest test is three questions: Is my basis big enough? Can I use the deduction this year? Am I holding long enough that recapture doesn't undo it? If all three are yes, talk to a CPA who runs these studies. If any is no, your tax dollars are better spent elsewhere.

Whether you're deciding to buy, hold, or restructure your Florida rentals, the tax strategy should follow the bigger plan, not drive it. If you'd like a clear read on what your Orlando or Tampa property could actually earn and how it fits your goals, get a free rental analysis from our team. And for the full library of Florida landlord tax and ownership guides, start at the Florida Owner's Guide.

This guide is educational and not tax advice. Cost segregation, bonus depreciation, passive activity loss rules, and recapture are fact-specific and change with the law. Confirm your situation with a qualified CPA before acting.