Do You Pay Income Tax on Rental Income in Florida?

Florida has no state income tax, so a lot of new landlords think rental income is tax-free. It is not. Here is what you actually owe, and why the number is usually smaller than you fear.

You started renting out a house in Orlando or Tampa, the rent checks are landing, and now there's a question keeping you up: do you owe tax on this money? Most new Florida landlords assume the answer is no — because Florida has no state income tax. That assumption is half right, and the half that's wrong can cost you.

Do you pay income tax on rental income in Florida?

Yes. There's no tax on rental income in Florida at the state level — Florida has no personal income tax — but rental income is taxed by the federal government. You report it on Schedule E with your Form 1040, and you're taxed on your net profit at your ordinary federal income-tax rate, not on the full rent you collect.

So the rent isn't tax-free. It's just that the tax bill comes from the IRS, not from Tallahassee. And here's the part that surprises people in a good way: because of how rental deductions work, the amount you actually pay tax on is often far smaller than the rent you banked. Sometimes it's close to zero in the early years.

Let's break down exactly how that works, where the confusion comes from, and what a real Florida rental looks like at tax time.

Florida has no income tax. So why do I owe anything?

Florida charges no state income tax — that part is real and permanent. But income tax in the United States comes from two layers: the state and the federal government. Florida skips the state layer. The federal layer applies to every landlord in the country, including yours. So you owe federal tax on rental profit, just not a separate Florida tax.

Florida is one of nine states with no personal income tax, and the Florida Department of Revenue confirms that residents, part-year residents, and nonresidents are not required to file a Florida individual income tax return. That's a genuine advantage. A landlord in California or New York pays state tax on rental profit on top of the federal bill. You don't.

But the IRS treats rent the same whether your property sits in Miami or Manhattan. The IRS rental income rules are federal, so the no-state-income-tax perk doesn't change what you report on your federal return.

One quick thing to clear up, because it trips up almost everyone: this is income tax, not property tax. Income tax is on your rental profit. Property tax is the annual county bill on the real estate itself, and it works very differently. If that's what you're trying to sort out, our guide to what Florida landlords pay and deduct in property tax covers the county side. This post is strictly about income tax on the rent.

How is rental income actually taxed?

You're taxed on your net rental income, not your gross rent. The formula is simple: gross rent minus deductible expenses equals taxable income. Then that taxable number gets added to your other income and taxed at your ordinary federal rate. Two landlords collecting the same rent can owe wildly different amounts, depending on their expenses.

Here's the formula, the example, and what the result tells you.

Formula: Gross rent − deductible operating expenses − depreciation = taxable rental income.

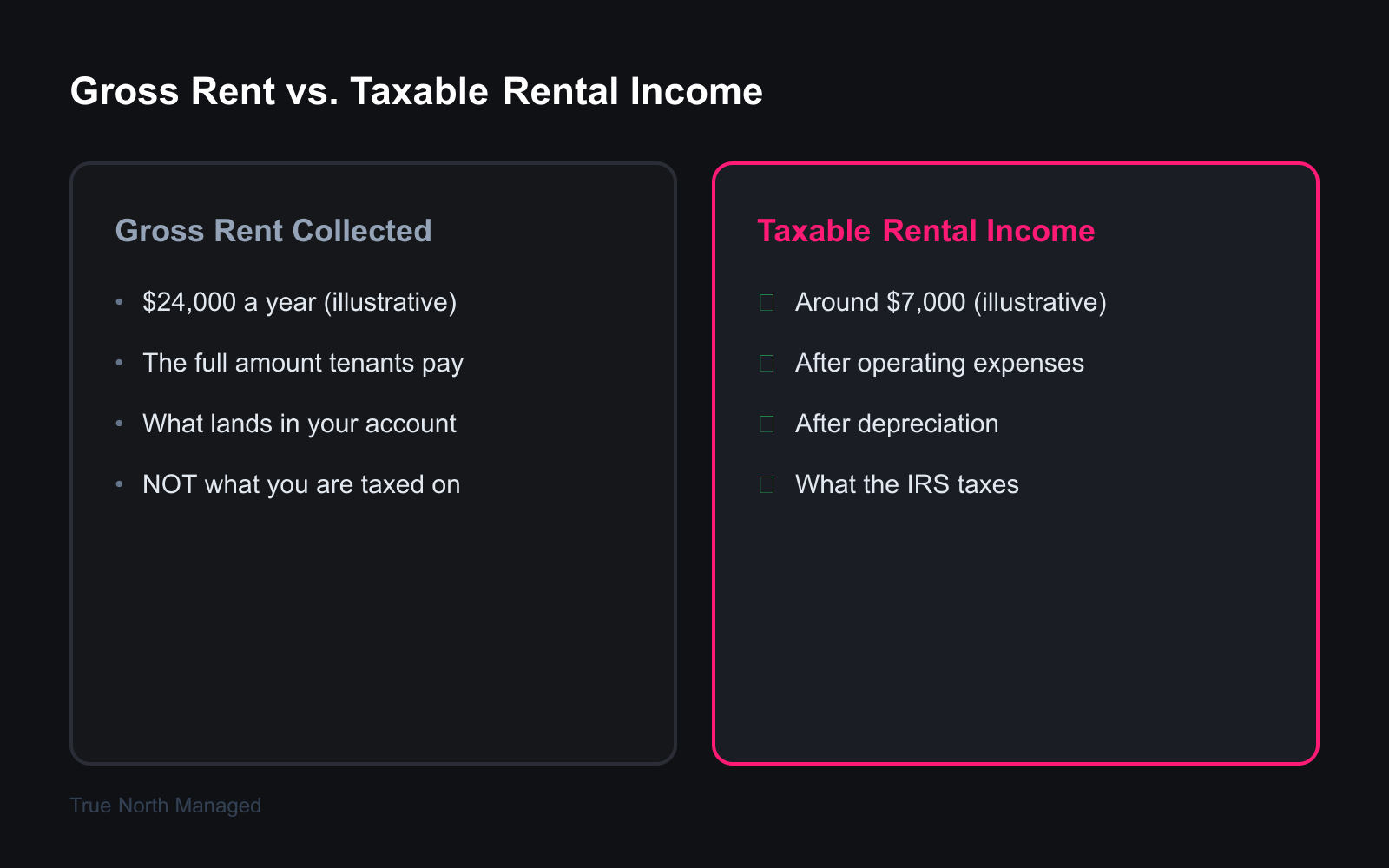

Example (illustrative — your numbers will differ): Say a Florida single-family rental brings in $24,000 a year (a round $2,000-a-month figure, used here just for the math). Your operating expenses — mortgage interest, county property tax, landlord insurance, repairs, and management fees — come to $9,000. That drops you to $15,000. Then depreciation, a paper deduction we'll explain next, knocks off roughly $8,000. Your taxable rental income lands around $7,000, not $24,000.

What that means: You collected $24,000 in cash, but you're only taxed on about $7,000 of it. At your marginal federal rate, that's the number the IRS cares about. In a property's early years, with a fresh mortgage throwing off heavy interest and full depreciation running, that taxable figure can drop to near zero — even though you're pocketing rent every month.

The expenses that get you there are the ordinary costs of running the rental, and you list them on Schedule E. The IRS guidance on rental real estate income and deductions spells out what qualifies: mortgage interest, property tax, insurance, repairs, management fees, advertising, travel, legal fees, and depreciation. We go line by line in our breakdown of the rental tax deductions most CPAs miss — the deductions are where a Florida rental's tax bill is won or lost, since the state itself taxes nothing.

One thing that is not income: a security deposit you might have to return. The IRS does not count a refundable deposit as rental income the year you receive it. If you keep part of it for damages later, that kept portion becomes income then. Don't report the deposit as rent up front.

How does depreciation shrink your tax bill to near zero?

Depreciation lets you deduct a slice of your building's cost every year, even though you didn't spend that money this year. The IRS treats a residential rental as wearing out over 27.5 years, so you write off roughly 1/27.5 of the building's value annually. It's a non-cash deduction — real on your return, invisible in your bank account.

This is the single biggest reason a profitable rental can show little or no taxable income. You deduct the building (not the land — land doesn't wear out) over 27.5 years using a straight-line method, per IRS Publication 527. On a building worth $220,000, that's roughly $8,000 a year coming straight off your taxable rental income, no checkbook required.

That's the deduction in our example above doing the heavy lifting. Collect $24,000, deduct your real costs, then deduct depreciation on top — and your taxable number shrinks dramatically.

Now the honest part a lot of blogs skip: depreciation isn't free money, it's deferred. When you sell, the IRS recaptures the depreciation you claimed and taxes it. So depreciation lowers your tax now and trades it for a bill later. That's usually still a good deal — paying later, often at a favorable rate, beats paying now — but you should know it's coming. Our Florida rental depreciation guide walks through the math, the basis calculation, and how recapture works at sale.

Do you pay self-employment tax on rental income?

Usually not. The IRS generally treats rental income as passive, which means it's exempt from the 15.3% self-employment tax that hits freelancers and sole proprietors. You pay regular income tax on rental profit, but you skip the Social Security and Medicare self-employment portion. That's a meaningful break for landlords.

The IRS Schedule E instructions keep most rentals out of self-employment territory because collecting rent isn't running a service business. There are two exceptions worth knowing. First, if you provide substantial services to tenants — think hotel-style cleaning, meals, concierge — the IRS may treat it as a business, and the income moves to Schedule C and gets hit with self-employment tax. Second, qualifying as a real estate professional changes how losses are treated (more on losses next). For a standard long-term rental in Orlando or Tampa where you collect rent and handle repairs, you're passive, and you skip the SE tax.

What if my rental loses money — can I deduct the loss?

Sometimes, but not always against any income you want. Because rentals are passive, a rental loss generally only offsets other passive income, not your W-2 salary. There's a key exception: if you actively participate and your income is under the threshold, you can deduct up to $25,000 of rental losses against your regular income.

The IRS passive activity rules in Publication 925 lay out the $25,000 special allowance. To use it you have to actively participate — approving tenants, setting rent, okaying repairs counts — and your modified adjusted gross income has to be under $100,000 to take the full amount. Between $100,000 and $150,000 the allowance phases out, and above $150,000 it's gone for most landlords.

So what happens to a loss you can't use this year? It doesn't vanish. Suspended passive losses carry forward to future years, and they free up entirely when you sell the property. A paper loss from depreciation today can become a real tax break down the road. This is the kind of thing worth getting right on the return itself — our Florida landlord tax filing guide for 2025 walks through how the forms actually fit together.

What about higher earners and the 3.8% net investment income tax?

If you're a higher earner, watch for an extra 3.8% on top. The net investment income tax applies to net rental income once your modified adjusted gross income passes $200,000 (single) or $250,000 (married filing jointly). It's separate from your regular income tax, and it catches a lot of out-of-state investors with strong W-2 jobs back home.

The IRS net investment income tax rules tax the smaller of your net investment income or the amount your MAGI exceeds the threshold, at 3.8%. Rental profit counts as net investment income. If your income sits below those lines, this doesn't apply to you at all.

This is the spot where Florida's no-state-income-tax perk has a limit worth naming. If you live in another state and own a Florida rental, Florida taxes nothing — but your home state may still tax that rental profit on your resident return, and the federal bill (plus possibly this 3.8%) applies regardless. The Florida advantage is real; it just doesn't erase your home-state or federal obligations.

Common mistakes Florida landlords make on rental income taxes

A few errors show up over and over, and every one of them costs money or invites an audit.

Assuming "no state income tax" means "no tax." The most common one. Florida skips the state layer, but the federal layer is alive and well. Reporting nothing because you thought rent was tax-free is how landlords end up with IRS notices.

Reporting gross rent instead of net. You're taxed on profit, not collections. Landlords who forget to deduct depreciation, mortgage interest, and management fees overpay — sometimes by thousands. The deductions are the whole game.

Treating the security deposit as income. A refundable deposit isn't rent. Counting it as income inflates your taxable number for no reason.

Throwing away receipts. Reconstructing expenses at tax time is where deductions get lost. Track every cost as it happens — repairs, mileage to the property, the plumber's invoice. If you can't prove it, you can't deduct it.

Skipping a pro on year one. The first return on a converted home or a new purchase sets your depreciation basis and your whole tax posture for years. Getting it right once beats fixing it later.

Know your real number before tax season

Florida's no-income-tax reputation is one of the best reasons to own a rental here — but the federal bill is real, and the size of it depends entirely on how well you track expenses and structure the property. The landlords who pay the least aren't the ones collecting the lowest rent. They're the ones who know what's deductible and report the right number.

If you'd rather not guess, request a free rental analysis and we'll walk through what your Orlando or Tampa property could earn — and what running it cleanly looks like, tax records included. The numbers are easier to handle when someone's tracking them for you from day one.

This article is general information, not tax advice. Tax rules change and your situation is specific — confirm the details with a CPA before you file.