Mortgage Rates and Florida Rental Demand in 2026: Why Renters Aren't Buying

High mortgage rates are putting a floor under Florida rental demand. Here's why your single-family rental keeps leasing even as the apartment market softens — and why you shouldn't panic-cut rent.

Mortgage Rates and Florida Rental Demand in 2026: Why Renters Aren't Buying

If you've been reading the headlines about a "softening" Florida rental market and you're nervous about your own property, here's the part the headlines leave out: high mortgage rates are quietly working in your favor.

The link between Florida rental demand and mortgage rates in 2026 is the most important thing most landlords aren't thinking about. The 30-year fixed sits at 6.52% as of the week of June 11, 2026, per Freddie Mac's weekly rate survey. At that rate, plus Florida's home prices and the highest insurance costs in the country, the math to buy a home is brutal. So the people who would normally buy keep renting instead. That's not a temporary blip. While rates stay elevated, it's a floor under your tenant demand.

Let's break down what's actually happening, why your single-family rental keeps leasing even in a "soft" market, and what it means for your rent and renewal decisions this year.

What does a 6.5% mortgage rate have to do with rental demand?

A 6.52% mortgage rate keeps Florida rental demand strong because it prices would-be buyers out of homeownership and back into the rental pool. At that rate, the monthly cost to buy a typical Florida home runs well above the cost to rent a comparable one. Households that can't clear the buy hurdle stay renters — and that keeps your units occupied.

Here's the chain of cause and effect. A buyer shopping a $400,000 home today isn't looking at the same payment they'd have seen in 2021. They're looking at a payment built on a rate that's roughly doubled, on a price that climbed through the pandemic, plus a Florida insurance premium that's the steepest in the nation. For a lot of those households, the number simply doesn't work.

When buying doesn't work, those households don't vanish. They rent. Nationally, renters drove about four of every five new household formations in 2025 (79.3%), pushing the U.S. renter count to a record 46.1 million, according to Arbor and Chandan Economics' analysis of Census data. The biggest reason is the one sitting in your favor: elevated rates have kept homeownership out of reach for millions of would-be buyers.

That's the demand floor. It's the reason your phone still rings when you list a well-priced rental, even in a year everyone's calling soft.

How much more does it cost to buy than rent in Florida right now?

Buying a typical Florida home costs hundreds of dollars more per month than renting a comparable one — often $500 to $800 more once you load in taxes and insurance. Nationally, the median mortgage payment now runs about 20% higher than the median rent, a full reversal from the 2010s when buying was usually cheaper.

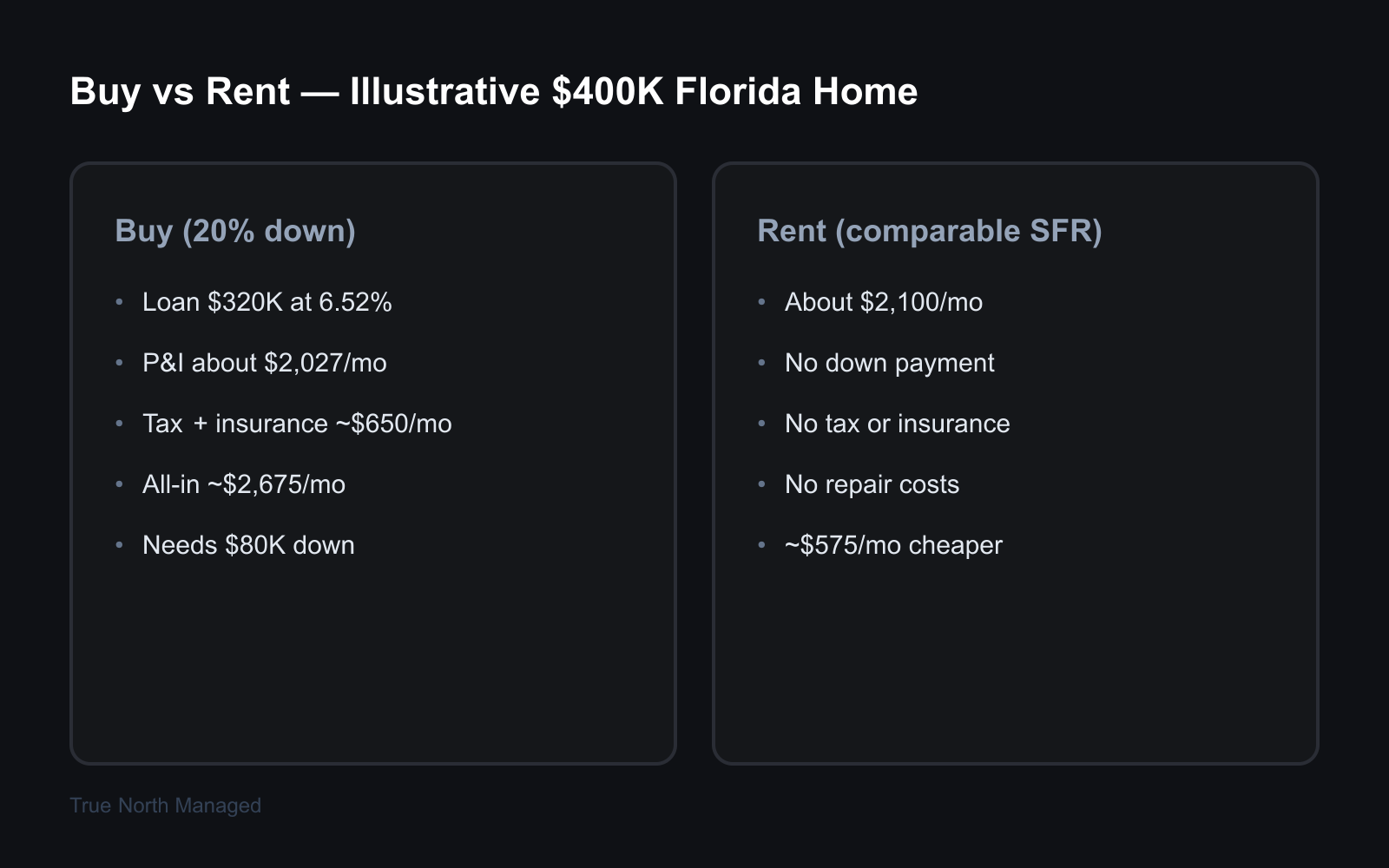

That national figure comes from Zillow's 2026 rent-versus-buy research, and Florida sits on the harder end of it because of insurance. Let's make it concrete with a single illustrative example. (These are illustrative numbers to show the gap — your specific deal will differ.)

The buy side — illustrative $400,000 single-family home (near Orlando's median):

- 20% down ($80,000), leaving a $320,000 loan

- At 6.52% on a 30-year fixed, principal and interest run about $2,027/month

- Add property tax ($330/month) and Florida homeowners insurance ($320/month)

- All-in monthly cost: roughly $2,675 — before a dollar of maintenance

The rent side — comparable single-family rental:

- Renting that same kind of house: roughly $2,100/month (illustrative, in line with several Florida single-family ZIPs we track)

The gap: about $575 more per month to own — and that's for the rare renter who actually has $80,000 sitting in the bank for a down payment. Most don't. Take away the 20% down and the buy payment climbs higher still.

So picture a household earning $90,000. They can comfortably handle $2,100 in rent for a nice house in a good school zone. They cannot comfortably handle a $2,675-plus mortgage payment plus repairs and a roof they're now responsible for. They stay your tenant. Multiply that household by thousands across Orlando and Tampa, and you've got your occupancy.

If you want to see where local rents actually land, we keep current figures in our guides to average rent across Orlando neighborhoods and what rent costs across Tampa.

Why is the apartment market soft if rental demand is strong?

Both things are true at once because the softness is a supply story, not a demand story. Orlando and Tampa got flooded with new apartment construction, so vacancy climbed and Class-A rents dipped — even while underlying demand for housing stayed strong. The renters are still there. There are just temporarily more brand-new luxury units chasing them.

This is the piece that confuses landlords, so it's worth slowing down on. Tampa's multifamily vacancy topped 10% for the first time in 15 years — about 10.7%, the highest since CoStar began tracking the metro in 2000. Average effective rent slipped to around $1,768 per CoStar, and more than a third of complexes started running concessions like a free month. Orlando's apartment vacancy has hovered near 9 to 10%, with rents roughly flat to slightly down year over year.

But look at what drove that: Tampa delivered a record wave of new apartments, and Orlando saw the same surge. That's the apartment glut digesting itself, and it'll take 12 to 18 months to clear. We dug into the supply side of this in our breakdown of Florida's rental construction surge and what it does to rents.

Here's the distinction that matters for you. The apartment softness is concentrated in big Class-A complexes in submarkets where developers overbuilt. A 3-bedroom single-family home in a good school zone is not competing head-to-head with a brand-new downtown apartment tower. Different product, different renter, different demand curve. The "soft market" headline is mostly about the towers — not about your house.

What does this mean if you only own one rental?

If you own a single property — maybe a home you couldn't sell, inherited, or moved out of — the rate environment is your safety net, not your threat. The would-be buyers who can't buy are exactly the people who want to rent a house like yours. That's why your home keeps leasing even when the news sounds grim.

Most landlords didn't set out to become landlords. Life handed you a property, and now you're watching market headlines wondering if you're about to get stuck with an empty house. So let's be direct: a single-family home priced right, in a decent neighborhood, is one of the most resilient rental assets in this market. The demand floor we've been describing protects it.

That doesn't mean you can ignore the basics. It means the macro wind is at your back, so your job is to not fumble the controllable stuff — pricing, condition, and tenant quality. Get those right and the rate environment does the heavy lifting on demand.

Should I lower my rent because the market looks soft?

Usually no — panic-cutting rent on a single-family rental is the most common mistake we see right now. The demand floor means well-positioned houses still lease at or near market. Cutting rent reflexively because of an apartment-market headline leaves money on the table and is hard to claw back at renewal.

Here's the better way to think about it. Your rent should answer one question: what will a real, qualified tenant pay for this specific house, in this specific neighborhood, today? Not what a downtown apartment tower is doing with concessions. Price to your comps — actual single-family rentals in your area — and you'll usually find the number holds up.

The local data backs this. Single-family rents across the metros have largely held flat to slightly positive even through the apartment glut. To put numbers on it, here are a few single-family-heavy ZIPs from our Zillow-sourced rent tracker (figures as of April 2026):

- Avalon Park (32828), Orlando: about $2,121, up 0.3% year over year

- New Tampa (33647): about $1,841, down 2.0%

- Brandon (33510): about $1,732, down 3.0%

- Kissimmee (34741): about $1,828, down 0.8%

Modest moves in both directions — not a collapse. A small dip in one ZIP isn't a signal to slash. If your house has been sitting unleased for three-plus weeks with steady showings and no applications, that's a pricing or condition problem worth a small, deliberate adjustment. A market-wide panic cut is not the answer.

What you don't want to do is forget the costs that quietly eat your margin while you're staring at the rent number. We walk through those in our guide to the real costs of owning a Florida rental — because protecting your rent only helps if you also protect your expenses.

How should I handle lease renewals in this environment?

Lean toward retention. With the buyer-to-renter pipeline keeping demand steady, a good tenant who renews saves you the single biggest cost in this business — turnover. A modest renewal increase that keeps a paying tenant in place usually beats a bigger increase that triggers a move-out and a vacancy.

Run the math the way we always recommend. A turnover isn't just lost rent during vacancy. It's make-ready costs, marketing, screening time, and the risk of a worse tenant. Even one month of vacancy plus a typical make-ready can wipe out a year's worth of an aggressive rent bump.

So the play in a demand-floor market is this: keep your good tenants with reasonable, justifiable increases, and reserve your aggressive pricing for genuine turnovers where you're resetting to market anyway. The strong underlying demand means you'll re-lease — but it also means you don't have to churn good tenants to capture market rent.

This is also where the rent-versus-strategy question comes in. If you've been weighing whether to chase higher short-term-rental income instead, the demand floor is part of that calculus too — we compared the two paths in our look at short-term versus long-term rentals in Florida.

Where's the real risk if rates stay high?

The risk isn't single-family demand — it's owning the wrong product in the wrong submarket. If you hold a Class-A unit in an over-built apartment node, the demand floor won't fully protect you, because you're competing with new towers offering concessions. The floor protects workforce and single-family housing far better than luxury apartments.

Be honest about what you own. CBRE's 2026 multifamily outlook pegs the monthly premium to buy versus rent at about 105% nationally — roughly twice the cost to own as to rent. That spread is the demand floor — but it routes renters toward affordable, practical housing, not toward $2,800-a-month luxury units competing with brand-new product.

So the risk map looks like this. Single-family homes and modest multifamily in established neighborhoods: well-protected by the floor. New Class-A apartments in submarkets that got overbuilt: exposed to the glut until supply absorbs over the next year-plus. If you own the second kind, the strategy is patience and competitive positioning, not assuming the macro tailwind covers you.

For a fuller framework on managing through this and protecting your returns, our Florida owner's guide pulls the financial and operational pieces together in one place.

The bottom line for Florida landlords

Mortgage rates at 6.52% are doing something useful for you, even if it doesn't feel that way from the headlines. They're keeping a large pool of would-be buyers in the rental market, and that demand floor is why a well-run single-family rental keeps leasing in 2026.

Three things to take away. First, don't confuse the apartment-market glut with your single-family demand — they're different markets. Second, resist the reflex to panic-cut rent; price to your real comps and the number usually holds. Third, watch your true risk, which is product and location, not demand.

Rates will move — they always do, and 6.52% is a snapshot of this week, not a permanent fixture. But while they stay elevated, the buyer-to-renter pipeline is a tailwind worth managing around instead of worrying about.

If you'd like a clear read on what your specific property should rent for in today's market — and how to position it so the demand floor works for you — get a free rental analysis. We'll give you real numbers for your house, your neighborhood, and this market.