Cap Rate vs. Cash-on-Cash Return: Which Matters for Florida Rentals?

Cap rate grades the property. Cash-on-cash grades your deal. Here's when each one matters for an Orlando or Tampa rental — and why both lie if your NOI uses out-of-state numbers.

Two numbers show up in every conversation about a rental deal: cap rate and cash-on-cash return. New investors treat them like rivals, as if one is right and the other is wrong. They're not rivals. They answer two different questions, and if you only ask one, you'll buy the wrong property or talk yourself out of the right one.

Here's the short version of cap rate vs cash on cash return: cap rate grades the house. Cash-on-cash grades your deal. One tells you whether the property is a good asset. The other tells you whether the way you bought it earns money. You need both, and in Florida you need to feed both the right numbers — because the two costs that wreck a Florida rental's math, insurance and property tax, are exactly the two that an out-of-state spreadsheet gets wrong.

Let's break down what each one actually measures, when to lean on it, and how the same Lake Nona or Riverview property can look great on one line and ugly on the next.

What is cap rate, and what does it actually tell you?

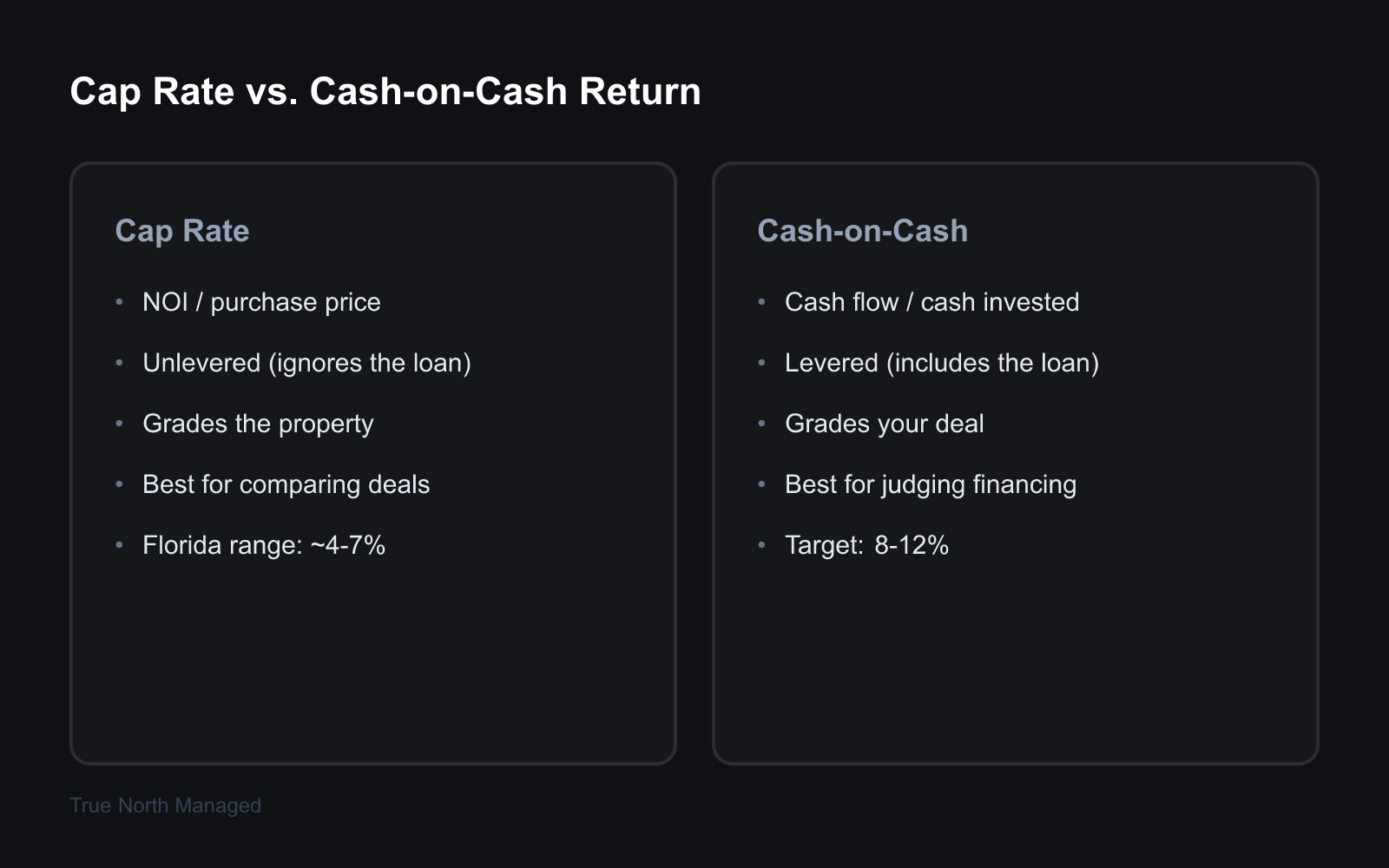

Cap rate is the return a property earns if you paid all cash, with no mortgage. You calculate it by dividing net operating income by the purchase price. It's an asset metric: it grades the property on its own, stripped of how anyone financed it.

Formula: Cap Rate = (Net Operating Income ÷ Property Value) × 100

Net operating income, or NOI, is your gross rent minus operating expenses — property taxes, insurance, maintenance, management, and any utilities you cover. NOI leaves out three things on purpose: your mortgage payment, big one-time projects like a roof, and income tax. That's the point. By ignoring the loan, cap rate lets you set two properties side by side and compare the assets, not the financing.

Example: You're looking at a duplex in Riverview listed at $354,000. It rents for $1,976 a month, or $23,712 a year. After you subtract real operating costs — taxes, a Florida landlord insurance policy, maintenance, management, and a vacancy allowance — you're left with about $16,300 in NOI. Cap rate: 4.6%.

What's good or bad? Florida residential and small-multifamily cap rates usually run 4% to 7%. In 2025, Orlando deals tend to land around 6.5–7%, Tampa a bit lower depending on the submarket and the building's condition. Below 4% means you're paying up for appreciation or a premium location. Above 7% often signals something — an older building, a rougher block, or deferred maintenance the seller is quietly pricing in. A 4.6% on a clean duplex in a growing submarket is reasonable; it just won't make you rich on cash flow alone.

Cap rate's whole job is comparison. It answers "is this a good property at this price?" without caring how you'll pay for it. That makes it the right tool for screening — and the wrong tool for judging your personal return.

What is cash-on-cash return, and how is it different?

Cash-on-cash return measures what the actual cash you put into a deal earns in a year. You divide your annual pre-tax cash flow by the total cash you invested. Unlike cap rate, it includes your mortgage, so it reflects your financing and your down payment — your deal, not just the property.

Formula: Cash-on-Cash = (Annual Pre-Tax Cash Flow ÷ Total Cash Invested) × 100

Annual cash flow is NOI minus your debt service — the principal and interest you pay the lender. Total cash invested is your down payment plus closing costs plus any upfront rehab. So while cap rate pretends you paid all cash, cash-on-cash deals with the loan you actually signed.

Example: Same Riverview duplex, $354,000, with $16,300 in NOI. You put 25% down — $88,500 — plus about $11,500 in closing and minor turn costs, for $100,000 of cash in. At a 30-year fixed rate of 6.75% (the going rate in mid-July 2025, per Freddie Mac's weekly survey), your loan of $265,500 costs roughly $20,650 a year in principal and interest. Cash flow: $16,300 − $20,650 = −$4,350. Cash-on-cash: negative.

That's the part new investors miss. The property is a perfectly decent asset at a 4.6% cap rate, but at 6.75% financing with 25% down, the deal bleeds cash. Drop the rate, put more down, or buy at a lower price, and the same property flips positive. Nothing about the building changed — only the deal did. That's why you can't judge financing on cap rate.

What's good or bad? Investors generally want cash-on-cash in the 8% to 12% range, though plenty will accept 5–6% on a low-risk property in a strong location where appreciation does the heavy lifting. A negative cash-on-cash isn't automatically a no — some buyers accept early break-even for long-term appreciation in a place like Lake Nona — but you should choose that on purpose, not discover it after closing.

When does cap rate matter more than cash-on-cash?

Cap rate matters more when you're comparing properties or checking whether a seller's price is fair. Because it ignores financing, it's the only clean way to line up a Carrollwood fourplex against a Lake Nona duplex and ask which asset earns more per dollar of price.

Reach for cap rate first when you're:

- Screening a list of deals. You can rank ten properties by cap rate in minutes without modeling ten different loans.

- Sanity-checking the asking price. If similar duplexes in the submarket trade at 5.5% caps and this one prices at a 4% cap, the seller is asking a premium — maybe justified, maybe not.

- Buying with cash, or planning to. No loan means cap rate basically is your return.

- Comparing across markets. A 6.8% cap in Tampa versus a 5% cap in a pricier metro tells you where the income is, before financing muddies it.

Cap rate is the screen. It's fast, it's property-focused, and it keeps you from wasting time modeling the financing on a deal that's overpriced as an asset. But a great cap rate with terrible financing is still a deal that loses money every month — which is where the second number comes in.

When does cash-on-cash return matter more?

Cash-on-cash matters more once you've decided a property is worth modeling and you're working out whether your specific purchase makes money. It's the metric that lives or dies on your down payment, your interest rate, and your closing costs — the levers that are yours, not the property's.

Lean on cash-on-cash when you're:

- Financing the purchase. The moment a mortgage enters the picture, cap rate stops describing your return and cash-on-cash takes over.

- Comparing financing structures. Same property, 20% down versus 25% down, gives you two very different cash-on-cash numbers. This is how you decide how much to put in.

- Judging whether to keep your own cash or borrow more. A higher down payment lowers your debt service and raises cash flow, but ties up more money — cash-on-cash shows the tradeoff in one number.

- Setting a personal return target. If you need 8% on your cash and the deal pencils to 4%, you have your answer.

If cap rate answers "is this a good property?", cash-on-cash answers "is this a good deal for me?" The first is about the asset. The second is about your wallet. Smart Orlando and Tampa investors run both on every property, in that order — and they don't trust either one until the NOI is built on real Florida costs. To see how financing order changes the picture before you ever calculate cash-on-cash, our guide on how to finance your first Florida rental property walks through the loan side.

Why do both numbers lie if your NOI uses out-of-state assumptions?

Both metrics sit on top of NOI, so both are only as honest as the operating costs underneath them. In Florida, two of those costs — landlord insurance and property tax — behave differently than they do almost anywhere else, and they're the two that out-of-state pro-formas get wrong. Plug in national assumptions and your cap rate and cash-on-cash both come out too high.

This is the trap behind the old 1% rule (rent should equal 1% of price). It only looks at gross rent and ignores operating costs entirely — so the 1% rule lies in Florida, where insurance and reassessed taxes can swing NOI by thousands. A deal that "passes" on gross rent can still bleed once real Florida costs hit the page. The fix is what we call the Florida Carry Test: before you trust any return metric, rebuild NOI with a real landlord insurance quote, the reassessed property-tax bill, and honest vacancy and maintenance reserves.

The insurance line nobody outside Florida budgets for

A long-time owner might carry a policy at a grandfathered rate. The new DP-3 landlord policy you buy in 2025 won't match it. Florida landlord premiums average around $2,200 a year and routinely run $2,100 to $4,000, with coastal properties higher — among the highest in the country, after Florida property insurance premiums jumped 34% from late 2022 through early 2025. If your pro-forma uses the national "$1,200 insurance" line, your NOI is overstated by a thousand dollars or more, and both metrics inherit the error. For a market-by-market read on this cost, see our breakdown of insurance costs in Orlando versus Tampa.

The tax bill that resets the January after you buy

This one catches almost every out-of-state buyer. A non-homestead investment property gets reassessed to full market value on January 1 of the year after you purchase it. The seller's tax bill may sit on an old, capped assessment — possibly a homestead exemption with a Save Our Homes cap you don't inherit. Once it's a non-homestead rental, that protection is gone and the assessment jumps to market value, subject to a 10% annual cap going forward. The Pinellas County Property Appraiser explains the reassessment plainly. If you model the seller's taxes instead of your future taxes, your Year-2 NOI is fiction — and so is the cap rate built on it.

Put those two together and the danger is clear: the seller's cap rate is a costume. A listing or pro-forma cap rate is usually built on the seller's costs — their old tax assessment and their grandfathered insurance — not yours. Re-underwrite NOI with your numbers before you trust either metric. That single discipline separates investors who do well in Florida from the ones who buy a "6% cap" and wonder why the account runs dry.

How do the two metrics work together on a real Florida deal?

Use cap rate to screen, then cash-on-cash to decide — and always run the cash-on-cash on Florida-real NOI. Here's the full sequence on one property, so you can see how a number moves when the inputs get honest.

Take a Lake Nona single-family rental priced at $658,000 that rents for $2,373 a month — $28,476 a year. An out-of-state buyer's first-pass pro-forma might look like this:

- Gross rent: $28,476

- Operating costs (national assumptions): $9,000

- NOI: $19,476

- Cap rate: 3.0% — already thin, because Lake Nona is an appreciation market with a high entry price

Now apply the Florida Carry Test. Swap the $1,200 national insurance line for a real $2,600 DP-3 quote. Replace the seller's capped tax bill with a reassessed non-homestead assessment. Add a 10% vacancy allowance and a 10% maintenance reserve instead of pretending those are zero. Operating costs climb to roughly $13,500, NOI drops to about $14,976, and the cap rate falls to 2.3%.

Then layer on financing. With 25% down ($164,500) plus closing costs, you're in for about $185,000 of cash. At 6.75% on a $493,500 loan, debt service runs near $38,400 a year — far above NOI. Cash-on-cash is deeply negative. This is a property you buy only if you're betting hard on appreciation and can carry the monthly loss out of pocket, with eyes open.

Run the same exercise on the Riverview duplex from earlier and you get a thin-but-positive cap rate, financing that's close to break-even, and a far easier decision. Same two formulas, completely different deals — because the inputs, not the math, are where Florida investing is won or lost. If you want the full system for stress-testing a purchase, the Financial section of our Florida Owner's Guide collects the cost-modeling, financing, and tax pieces in one place.

So which one should you actually use?

Both. Always both, in order. Screen with cap rate to find good assets at fair prices, then validate with cash-on-cash to confirm your specific deal earns money. Skip the first and you'll model financing on overpriced properties. Skip the second and you'll buy a "great" asset that drains your bank account every month.

And underneath both, do the Florida Carry Test first. A real insurance quote and a reassessed tax bill aren't fine print — in this state they're the difference between a 6% cap rate and a 4% one, and between positive cash flow and a monthly write-off. The investors who treat insurance and reassessment as afterthoughts are the ones who post on the forums asking why the numbers stopped working.

You don't need fancier math. You need honest inputs and the right metric for the right question. Cap rate grades the house. Cash-on-cash grades your deal. Feed them real Florida numbers, run them in that order, and you'll know — before you sign — whether a property is a good asset, a good deal, or just a good story.