Tenant Skipped Owing Rent: Recovering the Debt in Florida

Your tenant vanished owing rent. Here's how Florida landlords chase the money — the deposit claim, the money judgment, and the honest call on when to write it off.

The key's on the counter. Half the furniture's gone, the rest is junk they didn't want. Your texts go to a phone that's been disconnected. Rent's three months behind, and your tenant is — somewhere. Not here.

Re-renting the place is one problem. Getting your money back is a completely different one. And in Florida, they run on separate tracks. Here's how to chase the debt.

The short answer

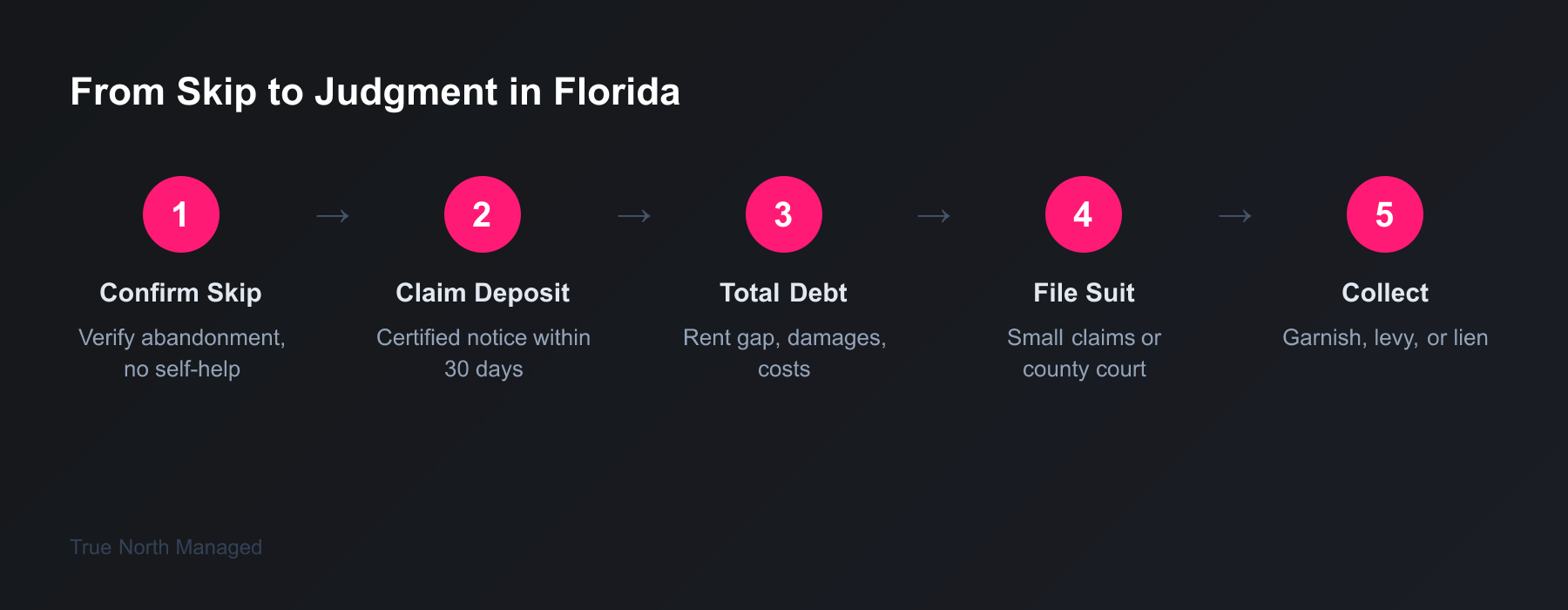

A skipped tenant who owes rent hands you two problems that look like one: the unit and the money. You handle the unit by confirming abandonment and re-renting. You handle the money through a separate civil action — sue for a money judgment in small claims (up to $8,000) or county court, win it, then try to collect. The catch most landlords don't hear until it's too late: in Florida, plenty of skips are partly or fully judgment-proof. So the real question isn't just how to recover the debt. It's whether it's worth chasing.

Why this hits different in Orlando and Tampa

A skip blurs three problems into one frantic afternoon: getting the unit back, dealing with the stuff they left, and recovering the money.

Those are three different legal tracks. Getting possession back is abandonment or eviction. The belongings they left behind have their own rulebook under Chapter 715 — we walk through that in our guide to handling a tenant's abandoned property. This post is about the third track, the one that keeps you up at night: the money.

And the money's real. Average rent in Orlando runs around $1,800 a month, and Tampa's a bit higher — see our breakdown of average rent across Orlando neighborhoods for the numbers by unit type. Three skipped months plus the cost of turning the unit lands you somewhere north of $6,000 — right at the edge of small claims court. That's not a write-it-off-and-shrug number for most owners. So let's break down how recovery actually works.

Did your tenant actually skip, or are they just gone for now?

Before you change a single lock, you need to know the unit is truly abandoned — not just empty for a couple of weeks. Florida presumes abandonment when the tenant's been gone for half a rental period (about 15 days on a monthly lease), rent is unpaid, and they gave you no written notice they'd be away. Act before that, and you're the one breaking the law.

Here's the trap. Florida Statute 83.59 says you can only get possession back three ways: the tenant surrenders it, the tenant abandons it, or a court hands it to you. There's no fourth option where you decide they're gone and clear the place yourself.

If you change the locks, haul out their belongings, or shut off the power on a tenant who hasn't actually abandoned the unit, you've committed a self-help eviction. Florida Statute 83.67 makes you liable for the tenant's actual and consequential damages — or three months' rent, whichever is greater — plus their attorney's fees. Think about that for a second. You're owed money, and one wrong move turns you into the one writing a check.

So slow down. The tenant who skipped owing rent and vanished for good? Re-take it. The tenant who's two weeks dark but might be in a hospital bed or deployed overseas? That's not abandonment yet — that might be an eviction for non-payment instead. Confirm which one you've got before you touch anything.

If this skip followed months of rent that always showed up late, you probably saw it coming. That history matters now — it's part of the paper trail you'll lean on if you decide to chase the debt.

How much can the security deposit actually cover?

Apply the security deposit to the unpaid rent and damages first — it's the easiest money to claim and it starts your paper trail. Florida gives you 30 days from the end of the tenancy to send written notice of your claim by certified mail. Miss that window and you forfeit the deposit entirely. The deposit almost never covers the whole debt, but it's the cleanest dollars you'll touch in this process.

The rules live in Florida Statute 83.49. Send the certified-mail notice within 30 days, telling the tenant exactly what you're keeping and why. They get 15 days to object in writing. If you make no claim at all, you owe the full deposit back within 15 days.

But do the math on what's left. Say you held one month's rent — $1,800 in Orlando. The tenant skipped owing three months plus you've got $1,200 in cleaning and re-key costs. The deposit knocks the balance down to maybe $4,800. Still a real number. The deposit is a down payment on your recovery, not the recovery itself.

One more thing: handle the deposit claim and the abandoned-property notice as separate processes. Different statutes, different deadlines. Don't let them blur.

What can you actually sue a skipped tenant for in Florida?

Here's where it splits from eviction. Getting possession back is one judgment; getting your money is a separate civil money action. You're suing for the unpaid rent, the damages, late fees if your lease allows them, and court costs. But Florida caps what you can recover — and how much depends on a choice you make the moment your tenant leaves.

Florida Statute 83.595 gives you four paths when a tenant breaks the lease and leaves early:

- Terminate and retake for your own account. You take the unit back, the tenant's off the hook for future rent. Clean break, but you eat the remaining lease.

- Retake for the account of the tenant. You re-rent the place and hold the tenant liable for the gap between their rent and what the new tenant pays.

- Stand by and do nothing. Hold the tenant liable for the rent as it comes due, month by month.

- Charge liquidated damages — but only if your lease has a signed early-termination addendum, and only up to two months' rent.

Most landlords who actually want their money pick option two. You re-rent, and the skipped tenant owes you the shortfall. But that option comes with a string attached, and it's the one people get wrong: the moment you re-rent for the tenant's account, you have to make a good-faith effort to fill the unit. The statute spells out what good faith means — you use at least the same effort you'd use renting it the first time, or the same effort you put into your other vacancies. You don't have to give it preference over your other empty units. You just can't let it sit dark and then bill the tenant for the whole empty stretch.

That's the part that trips people up. You can't leave the unit vacant for six months out of spite and send the ex-tenant a bill for six months' rent. Your recoverable damages are the lease rent minus what you collect from re-renting. Re-rent it in a month, and you can chase that one month's gap plus your costs.

Option three — stand by and do nothing — skips the re-rent duty, but it's almost always the wrong move against a skip. You'd be racking up rent on an empty unit, billing it to someone you may never collect a dime from, while your mortgage payment comes due every month. Re-rent it. Take the certain income over the theoretical judgment.

Small claims or county court — where do you file?

File in small claims if the debt is $8,000 or less, and in regular county court if it runs from $8,001 to $50,000. You file in the county where the property sits. Bring your lease, your rent ledger, and the deposit-claim paperwork. The whole thing only works if you can actually find and serve the tenant — no service, no case.

Florida's small claims division handles claims up to $8,000 under Florida Statute 34.01, and the Florida Courts small claims resource walks you through filing the statement of claim. Above $8,000, you're in county court proper. Filing fees run from $55 to $300 depending on the amount, plus around $45 for the sheriff to serve the papers.

If the tenant doesn't show up to court — and skips often don't — you can ask for a default judgment. For straight unpaid rent, where the number is fixed and provable from your lease and ledger, a judge can enter judgment on the paperwork alone. That's the good news.

The bad news is the part nobody puts in the brochure: you have to serve them first. You can't sue a ghost. If your tenant vanished and you can't track down an address, the case stops before it starts.

Is it even worth pursuing?

This is the question to answer before you spend a dollar on filing fees. A money judgment in Florida is a permission slip to try to collect — not a check. And against a lot of skipped tenants, that permission slip is worth very little, because Florida law shields most of what you'd want to grab.

Start with wages. Florida Statute 222.11 fully exempts the wages of a "head of household" — anyone providing more than half the support for a child or dependent. No dollar cap. So the working parent who skipped on you? If they qualify, you can't garnish a cent of their paycheck without a signed written waiver they almost certainly never gave you. That covers a huge share of the tenants who skip.

Then there's their home. Florida's homestead protection, written into Article X, Section 4 of the state constitution, shields a primary residence from forced sale with no cap on the equity. A civil judgment doesn't even lien it. Retirement accounts, Social Security, disability benefits — all off-limits too.

Stack it up and you get the hard truth: a tenant with no seizable bank account, exempt wages, and a homestead is, in practice, judgment-proof. You can win in court and collect nothing.

There's also the tax angle that surprises people. If you're a cash-basis landlord — and almost every small owner is — you can't write off that unpaid rent as a bad debt. You never reported it as income, so there's nothing to deduct. The only "benefit" is that you don't owe tax on money you never got. Cold comfort.

So weigh it honestly. If the tenant has a steady non-exempt job, money in the bank, or other assets, a judgment can pay off — and it follows them for 20 years. If they're broke and exempt across the board, chasing them is good money after bad. Writing it off isn't giving up. Sometimes it's just the math.

How do you collect once you have a judgment?

A judgment doesn't collect itself — you enforce it. The main tools are a writ of execution (the sheriff seizes and sells non-exempt property), a writ of garnishment (wages or bank accounts), and a judgment lien against any non-homestead real estate they own. Florida judgments stay valid for 20 years and earn interest the whole time.

A writ of execution lets the sheriff levy and sell non-exempt personal property. A writ of garnishment can capture up to 25% of disposable wages — assuming the head-of-household exemption doesn't apply — or freeze a bank account. Record the judgment with the clerk and it becomes a lien on any non-homestead property the tenant owns or later buys. And the balance grows: post-judgment interest is set quarterly by the state CFO under Florida Statute 55.03, running around 8% lately.

Can't find the tenant to enforce any of this? Start with skip-tracing. Pull the rental application — old employer, references, emergency contacts. Try the USPS address-correction service. Search public records. If you'd rather hand it off, a collection agency or a licensed skip-tracer can take it from here.

A quick note on collections and credit. When you call a former tenant about the debt, federal debt-collection rules don't apply to you — you're collecting your own money. The moment you hand it to a third-party agency, the FDCPA kicks in for them. And most small landlords can't report to the credit bureaus directly anyway. It's usually the collection agency that puts the debt on the ex-tenant's credit file, where it'll surface on the next landlord's tenant-screening report.

Three mistakes that cost Florida landlords the money

1. Re-taking the unit before you've confirmed abandonment. The single fastest way to turn a debt you're owed into a debt you owe. Change the locks on a tenant who hasn't legally abandoned, and Florida Statute 83.67 puts you on the hook for three months' rent plus their legal fees. Wait out the presumption or get a court order.

2. Blowing the 30-day deposit-claim deadline. The deposit is your easiest recovery, and the clock is unforgiving. Miss the certified-mail notice window under 83.49 and you forfeit the whole thing — handing money back to the tenant who skipped on you. Calendar it the day they leave.

3. Chasing a judgment-proof skip on principle. I get it — it feels wrong to let them walk. But a judgment against someone with exempt wages and no assets is a piece of paper. Spend the filing fee only when there's a real shot at collecting. Otherwise, claim the deposit, document everything for your records, and put your energy into re-renting.

When the math is too much to do alone

A skip is one of the worst weeks in a landlord's life. You're out the rent, you've got a unit to turn, and now you're being asked to play paralegal — deposit notices, money judgments, garnishment writs, exemption law. For a guide to the full landlord playbook in Florida, our owner's guide lays out where each of these pieces fits.

Or you let someone else carry it. We handle the deposit claim on deadline, document the file the way a court wants to see it, get the unit re-rented fast to cap your damages, and give you a straight answer on whether the judgment is worth chasing. So you're not the one Googling "how to garnish wages in Florida" at midnight.

If your tenant just skipped — or you'd rather never face this alone — get a free rental analysis and we'll talk through it.