Orlando Landlord Insurance: Orange County Coverage Specifics

Orange County landlords need DP-1 or DP-3 policies, windstorm coverage, and sinkhole awareness. Here's what actually matters for Orlando rentals.

Orlando rental properties face risks that standard homeowners insurance doesn't cover. Landlord policies in Orange County need to account for windstorm, flood zones, and Central Florida's unique sinkhole exposure. Here's what actually matters when you're insuring an Orlando rental.

DP-1 vs DP-3: What Orange County Landlords Need

Most Orlando landlords use either a DP-1 (named perils, ACV) or DP-3 (open perils, RCV) policy— DP-1 vs DP-3 explains the difference. DP-3 costs more but covers a broader range of losses—water damage, theft, vandalism—without listing each peril. For a $300K property in Dr. Most Orlando landlords use either a DP-1 (named perils) or DP-3

Most Orlando landlords use either a DP-1 (named perils, ACV) or DP-3 (open perils, RCV) policy—DP-1 vs DP-3 explains the difference. DP-3 costs more but covers a broader range of losses—water damage, theft, vandalism—without listing each peril. For a $300K property in Dr.

Most Orlando landlords use either a DP-1 (named perils) or DP-3 (open perils) policy. DP-3 costs more but covers a broader range of losses—water damage, theft, vandalism—without listing each peril. For a $300K property in Dr. Phillips or Lake Nona, the premium difference is often $200–400/year. Given turnover and tenant-caused damage, DP-3 usually pays for itself. Orlando market conditions favor newer construction in many submarkets, but older homes in College Park or Winter Park benefit most from open-perils coverage.

Citizens Property Insurance in Orange County

In Orlando, When private carriers won't write wind coverage in Florida, Citizens Property Insurance Corporation is. Orange County has a big Citizens footprint, especially for older homes and properties in wind-prone zones. Citizens policies are generally more expensive and come with assessment risk—if Citizens has a bad hurricane year, all policyholders is surcharged. When private

When private carriers won't write wind coverage in Florida, Citizens Property Insurance Corporation is. Orange County has a big Citizens footprint, especially for older homes and properties in wind-prone zones. Citizens policies are generally more expensive and come with assessment risk—if Citizens has a bad hurricane year, all policyholders is surcharged.

When private carriers won't write wind coverage in Florida, Citizens Property Insurance Corporation is the insurer of last resort. Orange County has a big Citizens footprint, especially for older homes and properties in wind-prone zones. Citizens policies are generally more expensive and come with assessment risk—if Citizens has a bad hurricane year, all policyholders is surcharged. The Florida Office of Insurance Regulation (OIR) oversees rate filings. Check whether your property qualifies for Citizens and what the private-market alternatives are before you assume it's your only option.

Windstorm vs Flood: Two Separate Policies

Standard landlord policies in Florida exclude flood. Windstorm is often included but may have a separate deductible—2% of dwelling value is common. For Orange County properties near the St. FL landlords in Orlando and Tampa should check local requirements. Standard landlord policies in Florida exclude flood. Windstorm is often included but may have a separate

Standard landlord policies in Florida exclude flood. Windstorm is often included but may have a separate deductible—2% of dwelling value is common. For Orange County properties near the St. FL landlords in Orlando and Tampa should check local requirements.

Standard landlord policies in Florida exclude flood. Windstorm is often included but may have a separate deductible—2% of dwelling value is common. For Orange County properties near the St. Johns River, Lake Apopka, or in flood zones, you need a FEMA flood policy through the NFIP or a private flood carrier. Flood zones matter: X zones have lower premiums; A and V zones cost more. Run the address through FEMA's flood map service center before you buy.

Sinkhole Coverage: Central Florida Specifics

In Orlando, Central Florida's limestone geology creates sinkhole risk. Catastrophic ground cover collapse is required in Florida landlord policies, but "sinkhole loss" coverage—which covers gradual ground movement and foundation cracks—is optional. In Orange County, many carriers offer it as an endorsement. Central Florida's limestone geology creates sinkhole risk. Catastrophic ground cover collapse is required in

Central Florida's limestone geology creates sinkhole risk. Catastrophic ground cover collapse is required in Florida landlord policies, but "sinkhole loss" coverage—which covers gradual ground movement and foundation cracks—is optional. In Orange County, many carriers offer it as an endorsement.

Central Florida's limestone geology creates sinkhole risk. Catastrophic ground cover collapse is required in Florida landlord policies, but "sinkhole loss" coverage—which covers gradual ground movement and foundation cracks—is optional. In Orange County, many carriers offer it as an endorsement. For homes in known sinkhole-prone areas (parts of Winter Garden, Ocoee, Apopka), the endorsement adds $100–300/year. Skip it in stable subgrades; add it where geology suggests risk. Our statewide landlord insurance guide covers the basics; this post focuses on Orlando-specific considerations.

Average Costs and Mitigation Discounts

Orange County landlord insurance premiums vary widely: $1,200–2,500/year for a $250K SFH is typical,. Wind mitigation credits can cut 10–25% off your premium: impact-resistant windows, reinforced garage doors, and a wind mitigation inspection report. Many Orlando homes built after 2002 already qualify for discounts. Orange County landlord insurance premiums vary widely: $1,200–2,500/year for a $250K

Orange County landlord insurance premiums vary widely: $1,200–2,500/year for a $250K SFH is typical,. Wind mitigation credits can cut 10–25% off your premium: impact-resistant windows, reinforced garage doors, and a wind mitigation inspection report. Many Orlando homes built after 2002 already qualify for discounts.

Orange County landlord insurance premiums vary widely: $1,200–2,500/year for a $250K SFH is typical, depending on age, construction, and location. Wind mitigation credits can cut 10–25% off your premium: impact-resistant windows, reinforced garage doors, and a wind mitigation inspection report. Many Orlando homes built after 2002 already qualify for discounts. Get an inspection and submit it to your carrier.

Next Step

Insurance is one piece of the Orlando rental puzzle. Get a free rental analysis to see what your property could generate—and how coverage fits into your numbers. We manage Orlando rentals across Orange County and can point you to local carriers who understand the market. Insurance is one piece of the Orlando rental puzzle. Get

Insurance is one piece of the Orlando rental puzzle. Get a free rental analysis to see what your property could generate—and how coverage fits into your numbers. We manage Orlando rentals across Orange County and can point you to local carriers who understand the market.

Insurance is one piece of the Orlando rental puzzle. Get a free rental analysis to see what your property could generate—and how coverage fits into your numbers. We manage Orlando rentals across Orange County and can point you to local carriers who understand the market.

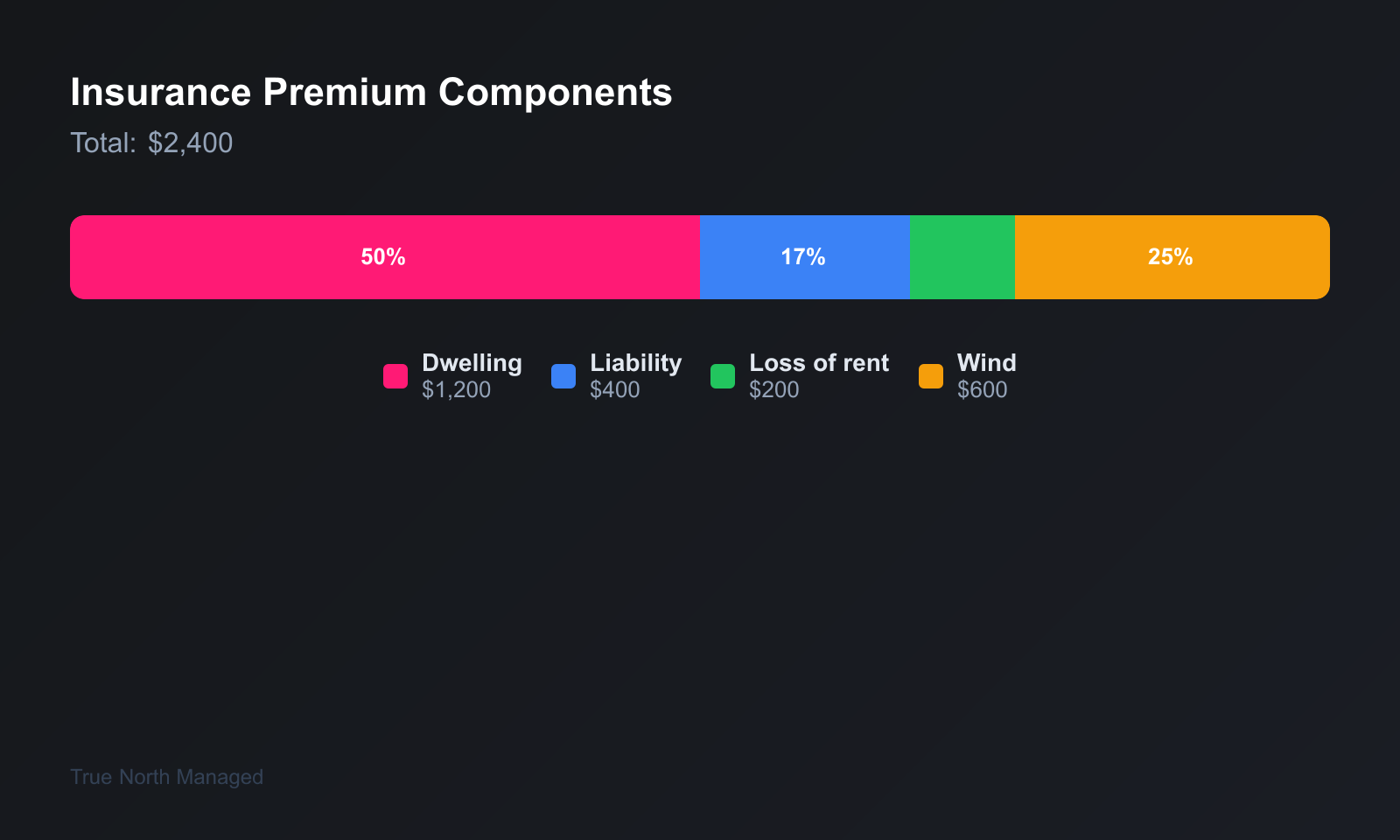

Orange County Coverage Basics

In Orlando, Orange County landlords need dwelling coverage, liability, and loss of rent. Wind and hail are included in most policies, but deductibles is 2% of dwelling value. Older homes may need wind mitigation updates to qualify for preferred rates. Orange County landlords need dwelling coverage, liability, and loss of rent. Wind and hail are

Orange County landlords need dwelling coverage, liability, and loss of rent. Wind and hail are included in most policies, but deductibles is 2% of dwelling value. Older homes may need wind mitigation updates to qualify for preferred rates.

Orange County landlords need dwelling coverage, liability, and loss of rent. Wind and hail are included in most policies, but deductibles is 2% of dwelling value. Older homes may need wind mitigation updates to qualify for preferred rates. Check the Florida CFO's consumer resources for insurance guidance.

Flood Zones

Orlando has pockets of flood zones, especially near lakes and retention areas. FEMA's flood map service shows designations. If your property is in a flood zone, flood insurance is typically required by your lender. FL landlords in Orlando and Tampa should check local requirements. Orlando has pockets of flood zones, especially near lakes and retention

Orlando has pockets of flood zones, especially near lakes and retention areas. FEMA's flood map service shows designations. If your property is in a flood zone, flood insurance is typically required by your lender. FL landlords in Orlando and Tampa should check local requirements.

Orlando has pockets of flood zones, especially near lakes and retention areas. FEMA's flood map service shows designations. If your property is in a flood zone, flood insurance is typically required by your lender. Even if not required, it is wise in low-lying areas. See our Tampa Bay flood zones guide for comparison.

Cost Ranges

Dwelling policies cover the structure; landlord policies add liability and loss of rent. Compare deductibles, wind/hail deductibles (often 2-5% of dwelling value in Florida), and loss-of-rent limits. Some policies cap loss of rent at 12 months. Policy Comparison In Orlando, Dwelling policies cover the structure; landlord policies add liability and loss of rent. Compare deductibles,

Dwelling policies cover the structure; landlord policies add liability and loss of rent. Compare deductibles, wind/hail deductibles (often 2-5% of dwelling value in Florida), and loss-of-rent limits. Some policies cap loss of rent at 12 months.

Policy Comparison

In Orlando, Dwelling policies cover the structure; landlord policies add liability and loss of rent. Compare deductibles, wind/hail deductibles (often 2-5% of dwelling value in Florida), and loss-of-rent limits. Some policies cap loss of rent at 12 months. Dwelling policies cover the structure; landlord policies add liability and loss of rent. Compare deductibles, wind/hail deductibles

Dwelling policies cover the structure; landlord policies add liability and loss of rent. Compare deductibles, wind/hail deductibles (often 2-5% of dwelling value in Florida), and loss-of-rent limits. Some policies cap loss of rent at 12 months.

Dwelling policies cover the structure; landlord policies add liability and loss of rent. Compare deductibles, wind/hail deductibles (often 2-5% of dwelling value in Florida), and loss-of-rent limits. Some policies cap loss of rent at 12 months. Umbrella policies sit on top for extra liability.

Common Exclusions and Claims

Flood and earthquake are excluded; buy separate policies if needed. In Florida, Wear and tear isn't covered. Document damage with photos before and after. FL landlords in Orlando and Tampa should check local requirements. Flood and earthquake are excluded; buy separate policies if needed. Wear and tear isn't covered. Document damage with photos before and

Flood and earthquake are excluded; buy separate policies if needed. In Florida, Wear and tear isn't covered. Document damage with photos before and after. FL landlords in Orlando and Tampa should check local requirements.

Flood and earthquake are excluded; buy separate policies if needed. Wear and tear isn't covered. Document damage with photos before and after. File claims promptly; delayed claims get more scrutiny. Keep receipts for temporary repairs.

What Landlord Policies Typically Exclude

Standard Orlando landlord insurance covers the structure, liability, and lost rent -- but it doesn't cover everything. Flood damage requires a separate NFIP or private flood policy. Mold remediation is often excluded or capped at $10,000 unless you buy a rider. Standard Orlando landlord insurance covers the structure, liability, and lost rent -- but it

Standard Orlando landlord insurance covers the structure, liability, and lost rent -- but it doesn't cover everything. Flood damage requires a separate NFIP or private flood policy. Mold remediation is often excluded or capped at $10,000 unless you buy a rider.

Standard Orlando landlord insurance covers the structure, liability, and lost rent -- but it doesn't cover everything. Flood damage requires a separate NFIP or private flood policy. Mold remediation is often excluded or capped at $10,000 unless you buy a rider. And tenant belongings are never your responsibility (though requiring renters insurance in your lease protects everyone). Read the exclusions page of your policy, not just the declarations page -- that's where the surprises hide.

Orange County Wind and Flood

Orange County isn't coastal, but windstorm still applies. Hurricane damage can reach inland—we saw it in 2004 and 2017. Windstorm coverage is usually a separate line item. Make sure it's included. Flood zones exist in Orlando—Lake Nona, Dr. Phillips, and some areas near the lakes. Check FEMA maps. If you're in a flood zone, your

Orange County isn't coastal, but windstorm still applies. Hurricane damage can reach inland—we saw it in 2004 and 2017. Windstorm coverage is usually a separate line item. Make sure it's included.

Flood zones exist in Orlando—Lake Nona, Dr. Phillips, and some areas near the lakes. Check FEMA maps. If you're in a flood zone, your lender will require flood insurance. NFIP or private—both work.

Liability Limits

In Orlando, Carry at least $300,000 in liability. A tenant or visitor who slips and falls can sue for more. Umbrella policies add $1-2 million for a few hundred dollars per year. Worth it at 3+ properties. Ensure your policy covers rental use. A homeowner policy doesn't. Landlord policies are different—they exclude owner-occupancy. Don't let

Carry at least $300,000 in liability. A tenant or visitor who slips and falls can sue for more. Umbrella policies add $1-2 million for a few hundred dollars per year. Worth it at 3+ properties.

Ensure your policy covers rental use. A homeowner policy doesn't. Landlord policies are different—they exclude owner-occupancy. Don't let your agent assume.

Bottom Line

Orlando isn't coastal but windstorm still applies. Carry $300k+ liability. Check flood zones. Get landlord-specific coverage.

Orlando isn't in a wind pool, but windstorm still applies. Hurricane damage can reach inland. Don't skip the coverage.

When in doubt, document it. Florida landlords who follow the process and keep a paper trail protect themselves when disputes arise. A few minutes of documentation can save months of headaches.

Expect $1,800 to $3,500 annually for a typical single-family rental in Orange County. Newer construction and wind mitigation credits can lower that. Compare quotes from multiple carriers. Our statewide landlord insurance guide covers coverage types. For Tampa comparison, see insurance costs Orlando vs Tampa.

If you own a rental in Orlando or Tampa and want a clear picture of what it could earn, get a free rental analysis. No obligation—just real numbers.