How to Convert Your Orlando Home Into a Rental Property

Thinking about renting out your Orlando home instead of selling? Here's the step-by-step process, the tax implications, and the math.

You're moving. Maybe it's a job transfer, a downsize, or a family change. Either way, you've got a house in Orlando and you're not ready to sell. Converting your primary residence to a rental can make sense—you keep the asset, someone else pays the mortgage, and Orlando's rental demand stays strong. But the switch isn't just a matter of listing on Zillow. there're tax implications, insurance changes, and legal steps you need to get right before a tenant moves in. See our Orlando tenant screening guide for more. See our Orlando landlord insurance specifics for more.

Here's the short answer: Plan for 4–8 weeks. You'll need to remove your homestead exemption, switch to landlord insurance, prep the property for tenants, and set up your lease and security deposit handling under Florida law. Miss a step and you could face denied insurance claims, tax surprises, or HOA fines.

Let's walk through what actually matters.

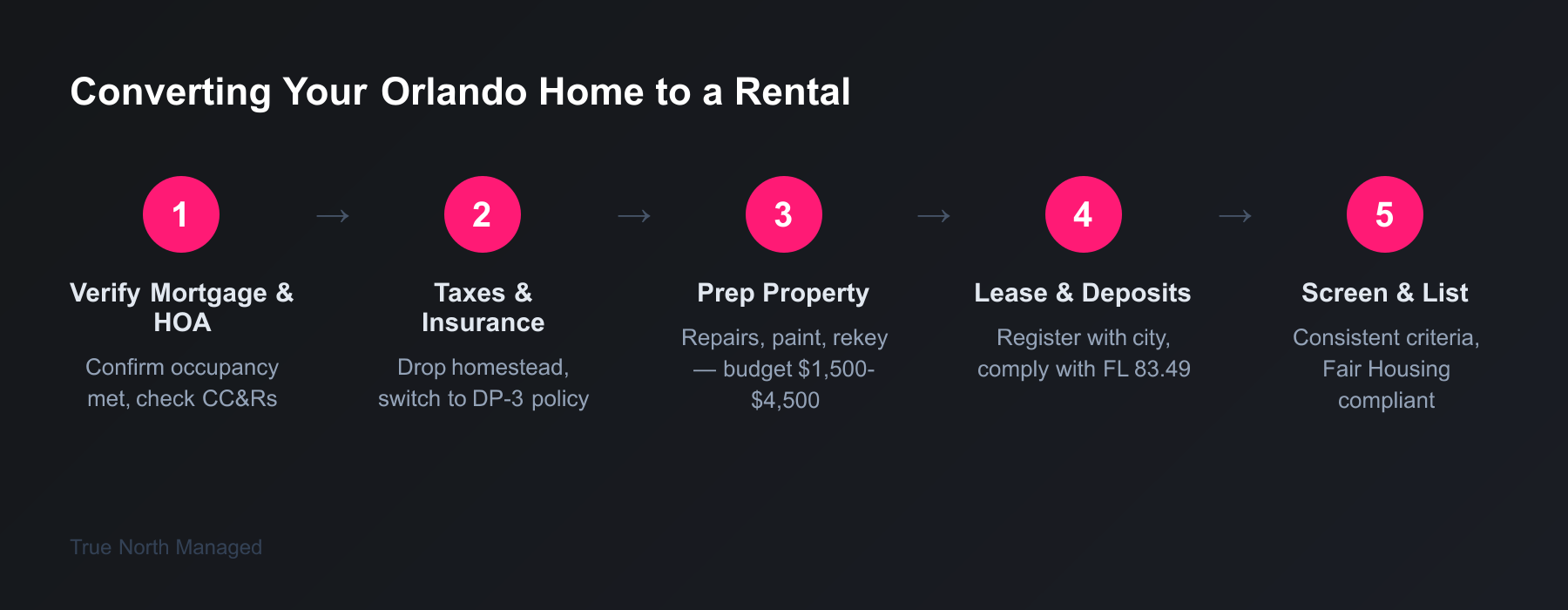

Your Conversion Checklist

Step 1: Check Your Mortgage and HOA First

Before you do anything else, verify you're allowed to rent.

Mortgage occupancy. Most conventional loans require you to live in the home for at least 12 months before converting to a rental. FHA, VA, and USDA loans often require 12–36 months. Violating an owner-occupancy clause can trigger loan acceleration or worse—it's treated as mortgage fraud. If you're past the occupancy period, notify your lender in writing that you're converting the property to a rental. Most lenders approve this without changing your loan terms as long as payments stay current.

HOA restrictions. Orlando-area HOAs vary widely. Some prohibit rentals entirely. Others allow them with minimum lease terms (often 30 days or more). Florida law lets HOAs restrict rentals, but they can't retroactively apply new restrictions to owners who bought before the rule was adopted. One exception: HOAs can enforce restrictions that limit leases to less than six months or cap rentals to three times per year without going through a formal amendment process. Pull your Covenants, Conditions, and Restrictions (CC&Rs) and confirm the rules in writing before you list. Violations mean fines—and you're on the hook for tenant violations too.

Step 2: Handle Taxes and Homestead

Converting to a rental changes your tax picture in two big ways.

Homestead exemption. Once you rent out your primary residence, you lose your homestead exemption. Florida allows you to keep it for the tax year if you rent after January 1, but you can't use that exception two years in a row. If you rent for more than 30 days per calendar year for two consecutive years, or more than six months total, the exemption is gone. Notify your county property appraiser when the property no longer qualifies—failure to do so can mean penalties and interest.

Capital gains. If you've lived in the home at least two of the last five years, you're eligible for the Section 121 exclusion—up to $250,000 ($500,000 if married) in tax-free gains when you sell. Converting to a rental and then selling later can reduce or eliminate that benefit. Gains are allocated between qualified use (when you lived there) and non-qualified use (when it was rented). Depreciation taken during the rental period is also recaptured at ordinary income rates when you sell. The IRS Publication 523 covers the rules in detail.

Depreciation. Once the property is converted, you can depreciate the building (not the land) over 27.5 years. Your basis is the lesser of your adjusted cost basis or fair market value on the conversion date—the IRS uses this "lower of" rule so you can't convert pre-conversion value declines into business losses. Depreciation starts when the property is "placed in service"—ready and available for rent and advertised to tenants—not necessarily when someone moves in. The IRS applies a mid-month convention, treating the property as placed in service in the middle of that month. Talk to a CPA before you convert; the numbers matter.

Step 3: Switch to Landlord Insurance

Your homeowner's policy won't cover a tenant-occupied property. Standard homeowner's insurance is designed for owner-occupied homes. If you rent it out and keep that policy, you risk denied claims and policy cancellation. You need a landlord (DP-3) policy that covers the structure, your liability for tenant and guest injuries, and lost rental income if the property becomes uninhabitable from a covered event. Your homeowner's policy covers your personal belongings and temporary housing—those don't apply when you're not living there.

Notify your insurance agent when the property becomes tenant-occupied. Require tenants to carry renter's insurance to protect their belongings and provide their own liability coverage—it's usually $10–20/month and reduces disputes over damages.

Step 4: Get the Property Rent-Ready

Make-ready costs vary by condition. A light cosmetic turn (touch-ups, deep clean, rekey) typically runs $1,500–$2,500 and takes 3–5 days. A standard prep (full repaint, partial flooring repairs, appliance servicing) runs $2,500–$4,500 and 5–7 days. Heavy deferred maintenance can push $4,500–$6,500 or more. Plan for repairs, fresh paint, professional cleaning, rekeying locks, and a final walkthrough before listing.

Budget 8–12% of gross rent annually for maintenance on an average-age property. Newer homes might need 5–7%; older properties might need 12–15%. The 1% rule—setting aside 1% of property value per year—is another common benchmark: a $300,000 home would mean $3,000/year. Real maintenance costs are unpredictable; industry data shows most landlords underestimate. Build a reserve before you list.

Orlando's rental market has cooled slightly—median rent is down about 1.8% year-over-year—but demand remains strong. Central Florida saw more renter demand than Miami and Fort Lauderdale combined over the past year. Price right using our Orlando rent guide and you'll fill the unit faster.

Step 5: Set Up Your Lease and Legal Obligations

Florida doesn't require a state-level rental license for long-term rentals, but Orlando requires residential rental properties to be registered annually with the city. Your legal responsibilities as a Florida landlord include maintaining the property in habitable condition, providing required disclosures, and following entry and deposit rules. Check your municipality for registration fees and any local inspection requirements.

Your lease must include:

- Clear identification of landlord and tenant

- Legal description of the dwelling

- Rent amount and payment schedule

- Landlord name, address, and agent for receiving notices

- Radon gas disclosure (required in every Florida lease)

- Lead-based paint disclosure (if built before 1978)

For leases over one year, Florida requires two witnesses to the landlord's signature. If you rent five or more units, you must include the full Florida Statute 83.49 security deposit disclosure in the lease or provide it within 30 days of receiving the deposit. The statute governs how you hold deposits: a separate non-interest-bearing or interest-bearing account in a Florida bank, or a surety bond. Notify the tenant in writing within 30 days of receipt with the bank name and account type. Return the full deposit within 15 days of move-out if no deductions, or send an itemized claim by certified mail within 30 days if claiming deductions. Miss that 30-day deadline and you forfeit the right to any deductions—even if the tenant left real damage.

Step 6: Screen Tenants the Right Way

Tenant screening protects you from bad tenants. The Fair Housing Act and Florida Fair Housing Act prohibit discrimination based on race, color, religion, sex, national origin, disability, and familial status. Create a written screening policy and apply it to every applicant: income verification (3x rent is the standard), credit check, rental history, and criminal background. You can't use blanket criminal bans—assess the nature, severity, and recency of any conviction. If you deny based on a consumer report, you must send an adverse action notice with the reporting agency's contact info and the applicant's right to dispute. Never ask about protected characteristics—disability, number of children, religion, country of origin, or marital status.

Step 7: Decide Whether to Self-Manage or Hire Help

Self-managing saves the management fee—typically 8–10% of monthly rent—but it's time-consuming. You handle tenant screening, advertising, maintenance calls, emergency repairs, and lease enforcement. Signs you should hire help: you're relocating out of state, you're unsure about Florida landlord-tenant law, or you don't have systems for rent collection and maintenance requests. Orlando property managers handle the legal compliance, 24/7 emergencies, and market pricing that new landlords often struggle with. About 66% of Orlando renters renewed leases in 2024; professionals often push that higher with better tenant placement. We've covered the full comparison and what it costs elsewhere.

What about an LLC? Holding the property in an LLC creates liability protection—if a tenant is injured or a dispute arises, the LLC's assets are at risk rather than your personal home and savings. Florida allows single-purpose LLCs for rental properties. Formation costs around $125 to file with the Division of Corporations. If you're considering an LLC, talk to an attorney; transferring an existing mortgage into an LLC can trigger a due-on-sale clause, so timing matters.

Common Mistakes When Converting

Skipping the insurance switch. Keeping homeowner's insurance while renting is a recipe for denied claims. Switch before the first tenant moves in.

Ignoring HOA rules. Check your CC&Rs before you list. Fines and forced lease terminations are real.

Forgetting the homestead notice. Notify your property appraiser when you convert. Penalties add up.

Under-budgeting for maintenance. Set aside at least 8–10% of gross rent. Deferred maintenance compounds fast.

Rushing tenant screening. A bad tenant costs far more than a few extra days of vacancy. Follow your screening process every time.

Listing before you're ready. The "placed in service" date for tax purposes is when the property is ready and advertised—not when you sign a lease. But more practically, listing a property that isn't rent-ready (broken appliances, peeling paint, dirty carpets) attracts the wrong tenants and lengthens vacancy. Finish the make-ready work first.

Committing deposit funds. Florida law forbids commingling security deposits with your personal or business accounts. Hold them in a separate Florida bank account from day one. Comingling can void your right to deduct from the deposit and expose you to penalties.

Converting your Orlando home to a rental is doable—and for many owners, it's the right call. Orlando's metro grew 12.7% during 2019–2024, one of the fastest rates for large markets nationally, and renter demand remains healthy even as the market cools. Get the legal, tax, and insurance pieces in place first, prep the property properly, and you'll be in a much better position when that first tenant signs the lease.

Not sure what your property could rent for or whether the numbers work? Get a Free Rental Analysis →