Security Deposit Alternatives in Florida: Surety Bonds Under FL 83.491

Since July 2023, Florida landlords can offer tenants a fee in lieu of a security deposit under FL 83.491. Most landlords still don't know this option exists — and the ones who do aren't sure if it's worth the trade-off.

Security Deposit Alternatives in Florida: Surety Bonds Under FL 83.491

This option has been available since July 2023, and most Florida landlords still don't know it exists.

Florida Statute 83.491 allows landlords to offer tenants a "fee in lieu of security deposit" — essentially a monthly surety bond payment that replaces the traditional upfront deposit. It's not a deposit. It's not a payment toward damages. It's a fee that funds a bond, and if your tenant causes damage, you file a claim against the bond instead of deducting from a deposit.

For landlords tired of the deposit-return drama under FL 83.49 — the 30-day notice requirement, the itemized deductions, the disputes — this is a genuinely different approach. But it comes with trade-offs worth understanding.

How Does FL 83.491 Work?

The law gives landlords exclusive discretion to offer this alternative. You're not required to offer it, but if you do offer it at a property, you generally must offer it to all new tenants on the same premises.

Here's the mechanics:

The tenant pays a recurring fee — typically monthly — instead of an upfront security deposit. The fee amount is set by the surety bond program you partner with (Rhino, Jetty, LeaseLock, Obligo are the main providers in Florida). Typical monthly fees run $15–$35 for a standard apartment or single-family rental.

The fee is NOT a deposit. This is the key distinction. The tenant doesn't get it back. It's a non-refundable fee that funds the surety bond. And it doesn't limit the tenant's liability — they're still on the hook for unpaid rent, damages beyond normal wear and tear, and any other obligations under the lease.

If the tenant causes damage, you file a claim against the surety bond. The bond provider pays you (up to the coverage limit, typically equal to what the security deposit would have been), and then the bond provider pursues the tenant for reimbursement.

Post-tenancy obligations. After the tenant moves out, you have 30 days to notify them of any costs or fees owed. If you're using the surety bond option, you can't submit a claim to the insurer until at least 15 days after notifying the tenant, and you must provide itemized documentation of losses.

What's the Math Look Like?

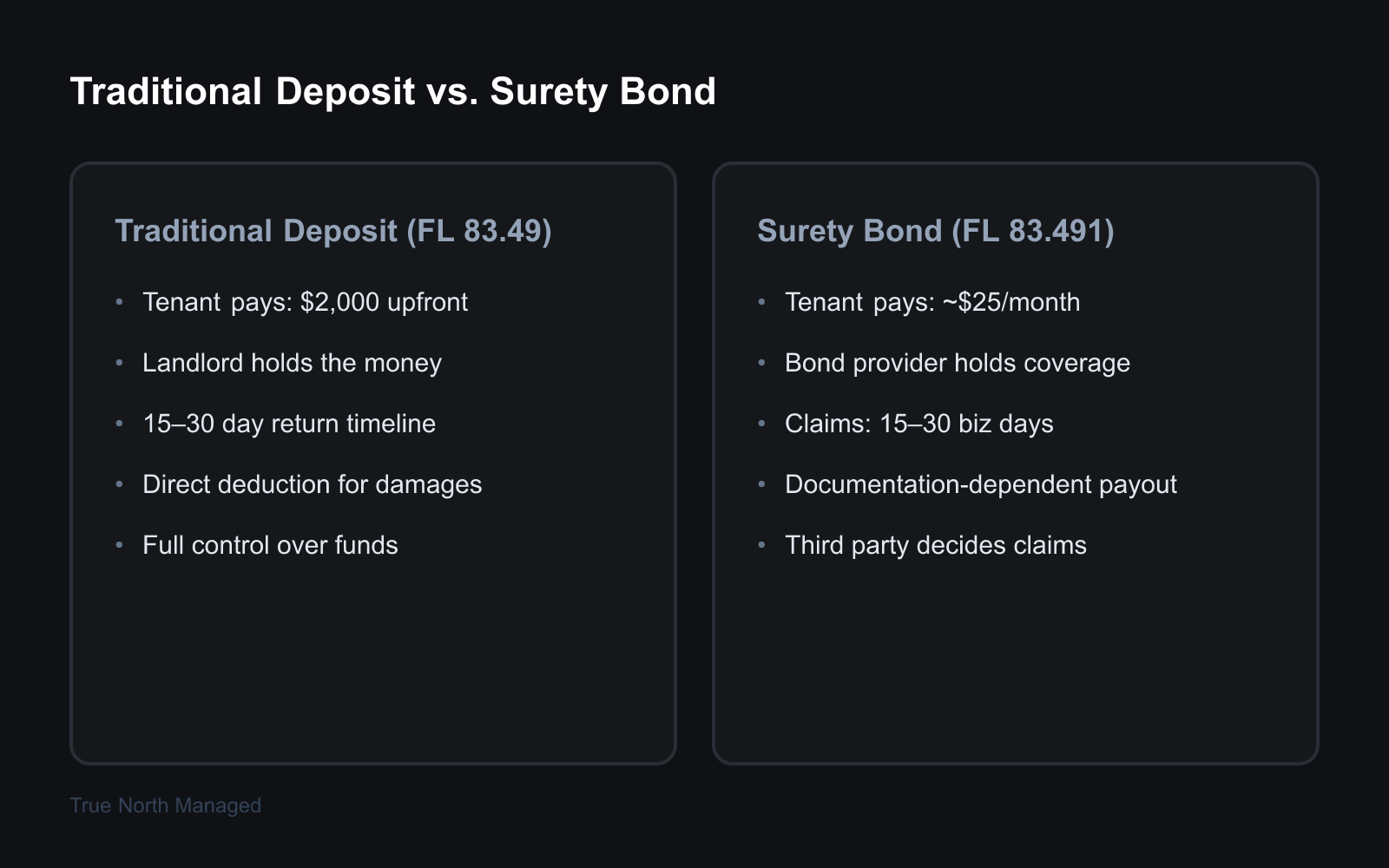

Let's compare a traditional security deposit vs. a surety bond on a $2,000/month rental.

Traditional deposit (FL 83.49):

- Tenant pays: $2,000 upfront (one month's rent)

- Landlord holds: $2,000 in a separate account (interest-bearing or surety bond required by FL 83.49)

- On move-out: Landlord has 15 or 30 days to return or provide notice of claim

- Maximum claim: $2,000 (the deposit amount)

Fee in lieu (FL 83.491):

- Tenant pays: ~$25/month ($300/year) — non-refundable

- Landlord holds: Nothing. The bond provider holds the coverage.

- On move-out: Landlord files a claim with documentation

- Maximum claim: Typically $2,000 (matching what the deposit would have been)

From the tenant's perspective, the surety bond reduces their move-in cost from $2,000 to $25. That's a massive difference for tenants who are cash-constrained — which, in a market where first-month rent plus deposit plus last month can total $4,000–$6,000, is a lot of tenants.

From the landlord's perspective, you're trading a pot of money you control for a claims process managed by a third party. That's the trade-off.

When Does the Surety Bond Work Better for Landlords?

Faster leasing. Lower move-in costs attract a wider applicant pool. If your property sits vacant for an extra two weeks because tenants can't scrape together the deposit, you're losing $1,000 in rent. The surety bond eliminates that barrier.

No deposit administration. FL 83.49 has strict rules about how you hold, report, and return security deposits. Miss the 30-day notification window, and you forfeit your claim entirely. With a surety bond, you're not holding any money — the administrative burden shifts to the bond provider.

Competitive differentiation. In a market with rising vacancy (and both Orlando and Tampa have seen vacancy rates climb this year), offering a deposit alternative makes your listing stand out. It's a tangible benefit that tenants compare when choosing between properties.

When Should You Stick With a Traditional Deposit?

You want direct control. With a traditional deposit, you hold the money. If the tenant owes $1,500 in damages, you deduct it and send the balance. With a surety bond, you file a claim, provide documentation, wait for review, and hope the bond provider agrees with your assessment. The claims process adds a step and a decision-maker you don't control.

The tenant is high-risk. If you're already on the fence about an applicant, a traditional deposit gives you immediate cash protection. A surety bond gives you a claim process — and claims can be denied or reduced if your documentation isn't thorough.

The bond coverage is too low. Some programs cap coverage at one month's rent. If your property rents for $2,000 but potential damage exposure is $5,000 (pets, pool, high-end finishes), the bond may not cover your actual risk.

How Does the Claims Process Work?

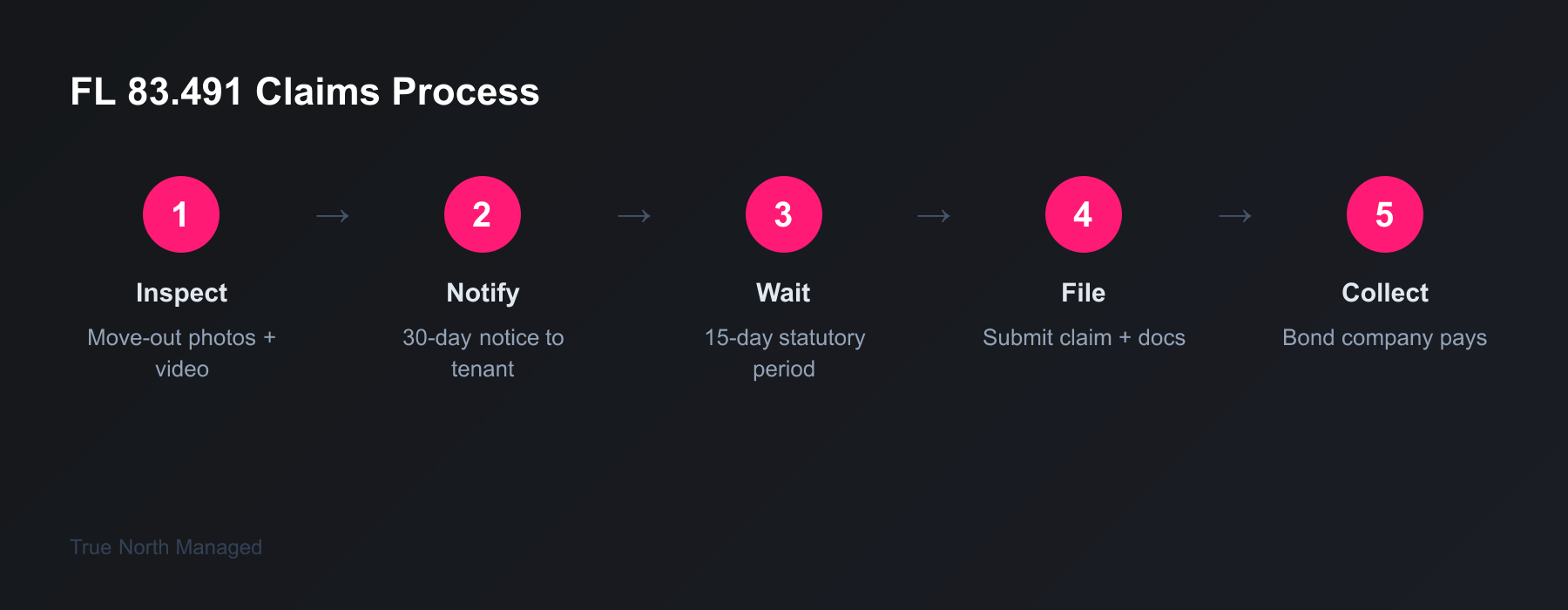

This is where it matters most. When a tenant moves out and you need to make a claim:

- Document everything. Conduct a thorough move-out inspection with photos and video. Compare to the move-in inspection.

- Send the 30-day notice. Just like with a traditional deposit, you notify the tenant of damages owed.

- Wait 15 days. FL 83.491 requires a 15-day waiting period after notification before you can submit a claim to the bond provider.

- Submit the claim. Provide the bond company with your move-out inspection, photos, invoices or estimates for repairs, and the tenant notification.

- Bond company reviews and pays. Review timelines vary by provider — typically 15–30 business days. If approved, the bond company pays you and then pursues the tenant for reimbursement.

The biggest risk: denied claims. Bond companies aren't in the business of paying every claim. Your documentation has to be tight — move-in and move-out photos, itemized repair costs, proof of normal wear vs. tenant damage. If your documentation is weak, the bond company may deny or reduce the payout.

This is actually one area where a property manager's inspection process pays for itself — PMs who manage the move-in/move-out documentation professionally are more likely to win claims.

Frequently Asked Questions

Can I require the surety bond option, or does the tenant get to choose? You choose whether to offer it. If you offer it, tenants can choose between the traditional deposit and the fee option. You can't force tenants to use the bond — they always have the right to put down a traditional deposit instead.

Does the fee program cover unpaid rent? It depends on the program. Some surety bonds cover unpaid rent, damages, and lease-break penalties. Others cover only property damage. Read the terms of the specific program you're considering.

What happens if the tenant leaves owing more than the bond covers? You pursue the tenant directly for the difference — through small claims court if necessary. The bond doesn't cap the tenant's liability; it only caps the bond company's payout.

Do I still need to follow FL 83.49 deposit rules if I offer the alternative? Yes, for any tenant who chooses the traditional deposit. FL 83.491 is an alternative, not a replacement. If even one tenant at the property opts for a traditional deposit, you still need to comply with all FL 83.49 requirements for that tenant's deposit.

Which bond providers operate in Florida? The major providers include Rhino, Jetty, LeaseLock, and Obligo. Each has a different fee structure, coverage limit, and claims process. Rhino and Jetty are the most widely available in Florida's Orlando and Tampa markets. Compare at least two providers before committing — pay particular attention to claims turnaround time and documentation requirements, because those determine how useful the bond actually is when you need it.

Can I switch back to traditional deposits after offering the alternative? Yes, for new leases. Existing tenants who signed up under the surety bond option stay on their current terms until the lease ends. You can stop offering the alternative to new tenants at any time.

Security deposit alternatives are a tool — not a universal upgrade. They make sense in specific situations (competitive markets, high move-in cost barriers, landlords who want less deposit administration) and less sense in others (high-damage risk, landlords who want maximum control).

If you're managing deposits — traditional or alternative — and want to make sure you're compliant with both FL 83.49 and FL 83.491, get a free rental analysis to see how professional management handles the financial side of your rental.