Flood Insurance for Florida Rental Properties: NFIP vs. Private Market

NFIP vs. private flood insurance for Florida rentals: cost comparison, when it's required, and how Risk Rating 2.0 changes the math.

When to Drop Coverage

In Florida, You can drop NFIP coverage if you're not in a flood zone and your lender doesn't require it. But FEMA maps change -- FEMA Risk Rating 2.0 has shifted zones. Orlando and Tampa have plenty of properties in or near flood zones. Elevation matters. If your property is above the base flood elevation,

You can drop NFIP coverage if you're not in a flood zone and your lender doesn't require it. But FEMA maps change -- FEMA Risk Rating 2.0 has shifted zones. Orlando and Tampa have plenty of properties in or near flood zones.

Elevation matters. If your property is above the base flood elevation, rates drop. An elevation certificate can cut premiums in high-risk zones. Ask your agent if it's worth it.

Reconsider only if the property is clearly outside any flood zone and you've paid off the mortgage. Even then, Florida sees flooding outside mapped floodplains. Dropping coverage when the loan is paid off leaves your equity and tenants exposed. The savings rarely justify the risk. Check FEMA maps before deciding.

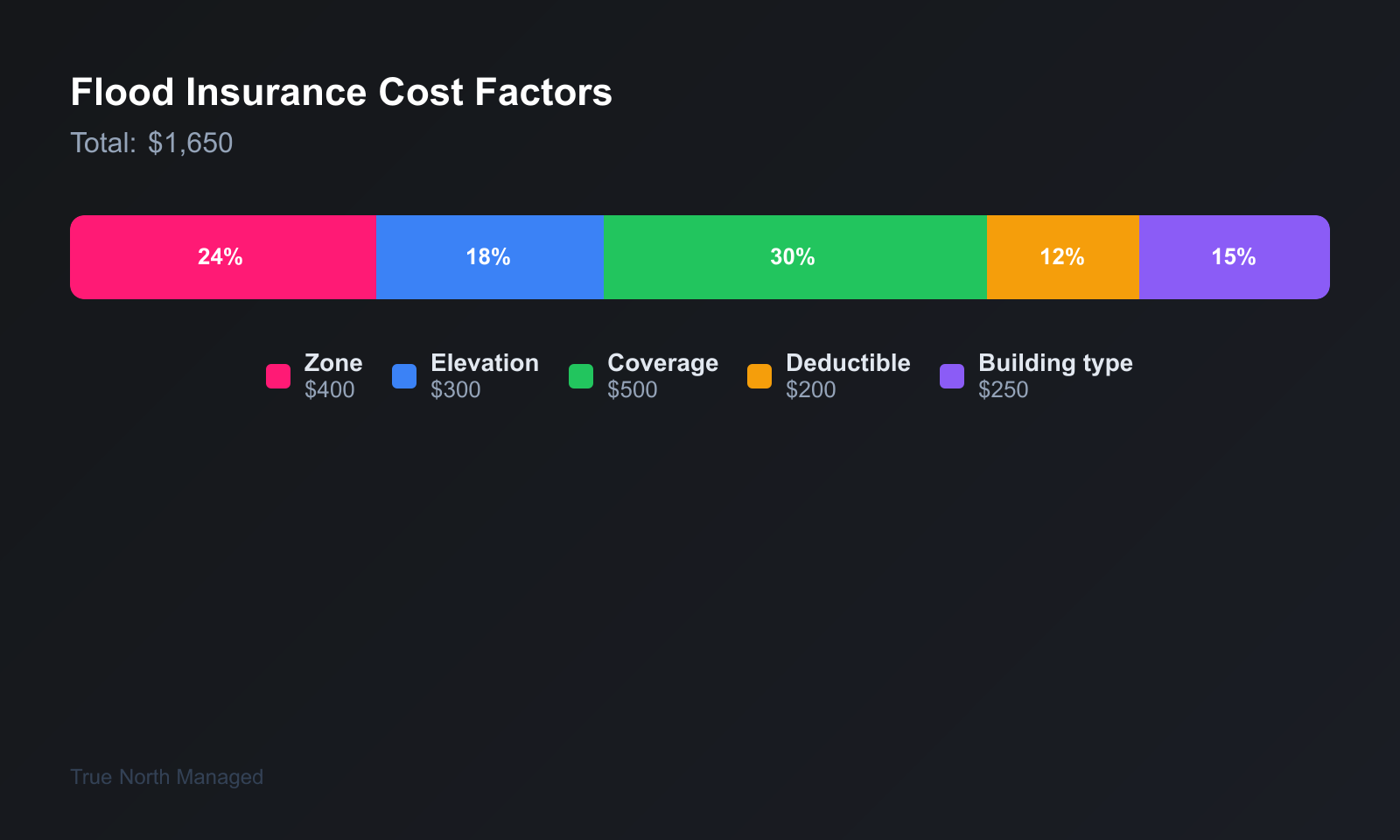

Florida rental properties face flood risk from hurricanes, storm surge, and heavy rain. Landlords need to know: NFIP vs. private flood insurance (NFIP doesn't cover loss of rents; private policies often do for 12–24 months), when coverage is required, and how FEMA's Risk -- Rating 2.0 changes the cost picture.

When Is Flood Insurance Required?

Flood insurance is required if your property is in a FEMA flood zone and you've a mortgage. Lenders mandate it. Cash buyers can skip it, but that's risky. Florida has extensive flood exposure. If your rental has a federally backed mortgage (FHA, VA, Fannie, Freddie), the lender will require flood insurance if the property is

Flood insurance is required if your property is in a FEMA flood zone and you've a mortgage. Lenders mandate it. Cash buyers can skip it, but that's risky. Florida has extensive flood exposure.

If your rental has a federally backed mortgage (FHA, VA, Fannie, Freddie), the lender will require flood insurance if the property is in a FEMA Special Flood Hazard Area (SFHA). That's Zone A or V. Even outside SFHAs, many lenders require it in Florida. Cash buyers can choose, but skipping coverage in a flood-prone state is risky.

NFIP: The Government Option

NFIP is the government option -- typically $500-$2,000/year for residential. Risk Rating 2.0 has changed pricing. Some Orlando and Tampa properties saw big increases. The National Flood Insurance Program (NFIP) is the traditional source. Coverage is standardized: building and contents limits, deductibles, waiting periods. Premiums are set by FEMA and have historically been based on zone and elevation. FloodSmart.gov is the official NFIP resource for rates and agents. NFIP building coverage maxes at $250,000 for residential. For a $300,000 rental, you'd need to supplement or go private for full replacement cost.

Risk Rating 2.0: What Changed

Risk Rating 2.0: FEMA's new pricing model considers flood risk, distance to water, and building type. Some Florida properties saw 2-3x premium increases. Check your zone. FEMA rolled out Risk Rating 2.0 to price policies based on individual property risk rather than zone alone. Factors include distance to water, flood frequency, building characteristics, and replacement

Risk Rating 2.0: FEMA's new pricing model considers flood risk, distance to water, and building type. Some Florida properties saw 2-3x premium increases. Check your zone.

FEMA rolled out Risk Rating 2.0 to price policies based on individual property risk rather than zone alone. Factors include distance to water, flood frequency, building characteristics, and replacement cost. Some properties saw premium drops; others saw sharp increases. Check your current and projected rates with an agent.

Private Flood Insurance

Private flood insurance is cheaper or offer higher coverage. Shop both NFIP and private. Orlando and Tampa have agents who specialize in flood. Private carriers offer higher limits, flexible deductibles, and sometimes lower premiums. They're not bound by NFIP rules. In Florida, private flood has grown as NFIP rates have risen. Compare quotes from carriers that specialize in coastal properties.

Cost Comparison

Cost comparison: NFIP vs. private varies by zone and property. $500-$2,000/year is typical for residential. Get quotes before you buy. NFIP premiums in Florida vary widely: $500–$3,000+ annually depending on zone, elevation, and building value. Private policies is cheaper for low-risk properties and more full for high-value ones. Get both quotes.

Florida-Specific Considerations

Florida considerations: hurricane surge, riverine flooding, and NFIP rate changes. Coastal zones are expensive. Inland Orlando and Tampa have some flood exposure too. Orlando and Tampa have different flood exposure. Coastal Tampa properties face storm surge; inland Orlando faces riverine and rainfall flooding. Check the FEMA Flood Map Service Center for your exact address. Our

Florida considerations: hurricane surge, riverine flooding, and NFIP rate changes. Coastal zones are expensive. Inland Orlando and Tampa have some flood exposure too.

Orlando and Tampa have different flood exposure. Coastal Tampa properties face storm surge; inland Orlando faces riverine and rainfall flooding. Check the FEMA Flood Map Service Center for your exact address. Our Florida flood disclosure guide covers what you must tell tenants.

Flood insurance is one piece of Florida rental protection. Pair it with landlord insurance and windstorm coverage. If you're evaluating a rental in Orlando or Tampa, get a free rental analysis and we can factor insurance costs into the numbers.

NFIP vs. Private Flood

NFIP vs. private: compare both. Private is cheaper for some properties. NFIP has caps. Shop. NFIP (National Flood Insurance Program) is the traditional option. Coverage maxes at $250,000 building and $100,000 contents. Private flood insurance often offers higher limits, faster claims, and sometimes lower rates. Compare both. Check FEMA flood maps for your property's zone. X zones often don't require flood insurance for mortgages, but Florida flooding happens outside mapped floodplains.

Cost Benchmarks

Cost benchmarks: $500-$2,000/year for residential. Risk Rating 2.0 has pushed some higher. Get quotes. NFIP rates vary by zone and elevation. In moderate-risk zones, expect $500–1,500/year for a typical SFH. High-risk zones run $2,000–4,000 or more. Private policies is 20–40% cheaper in some areas. Get quotes from both. For more on Florida flood disclosure requirements , see our guide.

Common Flood Insurance Mistakes

In Florida, Common mistakes: skipping flood when not required, under-insuring, and not shopping. One flood can wipe out equity. Orlando and Tampa have seen it. Assuming your landlord policy covers flood. It doesn't. Dropping flood insurance because the mortgage was paid off. Tenants and your equity are still at risk. Not documenting contents. If you

Common mistakes: skipping flood when not required, under-insuring, and not shopping. One flood can wipe out equity. Orlando and Tampa have seen it.

Assuming your landlord policy covers flood. It doesn't. Dropping flood insurance because the mortgage was paid off. Tenants and your equity are still at risk. Not documenting contents. If you provide appliances or furniture, list them. Finally, waiting until hurricane season to buy. There's often a 30-day waiting period for new NFIP policies. For hurricane prep that includes insurance, see our checklist.

In a flood zone? Get a free rental analysis to understand your property's risk profile.

Bottom line: landlord policies don't cover flood. Get NFIP or private flood. Check FEMA maps for your zone. Buy before hurricane season—there's often a 30-day wait. Document contents. Dropping coverage when the mortgage is paid off leaves you exposed.

Private flood carriers have entered the Florida market in recent years. Rates is 20–40% lower than NFIP in some zones. Get quotes from both. Coverage limits and claims process differ. Read the policy. "Flood" can mean different things—rising water vs. storm surge—depending on the carrier.

When Coverage is Optional

Coverage is optional if you're not in a flood zone and own outright. But zones change. Consider it anyway.

Common Mistakes to Avoid

One of the biggest mistakes we see: skipping the written notice. Florida law is strict about documentation. If you don't have a paper trail—or email trail that meets SB 716's requirements—you can lose an eviction or deposit dispute. Document everything. Another mistake: underbudgeting for turnover. A typical Florida turnover runs $1,500–$3,000 when you include paint,

One of the biggest mistakes we see: skipping the written notice. Florida law is strict about documentation. If you don't have a paper trail—or email trail that meets SB 716's requirements—you can lose an eviction or deposit dispute. Document everything.

Another mistake: underbudgeting for turnover. A typical Florida turnover runs $1,500–$3,000 when you include paint, carpet, cleaning, and minor repairs. If you're only setting aside 5% of rent for maintenance, you're short. Plan for 8–12% in year one until you know your property.

Third: treating every tenant the same. A military family near MacDill has different needs than a UCF grad student. Screen for fit, not just credit score. The right tenant in the right property stays longer and costs you less.

Florida-Specific Considerations

Florida Statute 83 applies to residential tenancies. Know the notice requirements: 3 days for non-payment (soon 5 under SB 716), 7 days for cure or vacate for lease violations, 15 days for month-to-month termination. Wrong notice = delayed eviction.

Insurance is another Florida reality. Wind and flood can double your premium in certain zones. Run quotes before you buy. A $200/month insurance difference changes your cash flow by $2,400/year.

Finally, property taxes. Homestead doesn't apply to rentals. You'll pay non-homestead rates. In Florida County, that's typically 1.2–1.5% of assessed value. Appeal if your assessment seems high—many landlords overpay.

When to Get Help

If you're out of state, hire a local property manager. The 8–10% fee pays for itself in faster leasing, better screening, and someone who can show up when the AC dies at 10 PM. Self-managing from another state is a recipe for deferred maintenance and tenant frustration.

For legal issues—evictions, deposit disputes, lease breaks—consult a Florida-licensed attorney. Landlord-tenant law has traps. A $500 consult can save you $5,000 in a botched eviction. We've seen it.

Finally, for complex financial decisions—1031 exchanges, LLC structuring, depreciation—talk to a CPA who works with rental owners. The tax code rewards those who plan. Don't wing it.

When to Get Help

If you're out of state, hire a local property manager. The 8–10% fee pays for itself in faster leasing, better screening, and someone who can show up when the AC dies at 10 PM. Self-managing from another state is a recipe for deferred maintenance and tenant frustration.

For legal issues—evictions, deposit disputes, lease breaks—consult a Florida-licensed attorney. Landlord-tenant law has traps. A $500 consult can save you $5,000 in a botched eviction. We've seen it.

Finally, for complex financial decisions—1031 exchanges, LLC structuring, depreciation—talk to a CPA who works with rental owners. The tax code rewards those who plan. Don't wing it.

If your rental property sits in Zone X -- minimal flood risk -- and you own it free and clear, flood insurance becomes a financial decision rather than a lender requirement. But even in low-risk zones, about 25% of flood claims come from areas outside high-risk designations. Weigh the annual premium against your ability to absorb a $50,000-plus loss, and make a deliberate choice rather than simply skipping coverage by default.

Elevation matters. If your property is above the base flood elevation, rates drop. An elevation certificate documents this. Cost runs $500–1,000 but can cut premiums significantly in high-risk zones. Ask your agent if it's worth it for your property. The certificate stays with the property for future owners.

If you own a rental in Orlando or Tampa and want a clear picture of what it could earn, get a free rental analysis. No obligation—just real numbers.