Condo Investing in Florida: HOA Risks Every Landlord Should Know

Florida condo investing carries risks most SFR landlords never think about — milestone inspections, mandatory reserves, special assessments hitting $50K–$400K per unit, and HOA rental restrictions that can shut down your cash flow overnight.

Condo Investing in Florida: HOA Risks Every Landlord Should Know

You found a condo in Florida with numbers that look great on paper — purchase price under $250,000, projected rent at $1,800/month, 6% cap rate. Before you write the offer, there are risks specific to Florida condos that don't exist with single-family rentals, and they can wipe out your returns in a single board meeting.

With the December 2025 compliance deadline approaching for structural reserve studies, Florida's condo landscape looks fundamentally different than it did three years ago. The Surfside building collapse in June 2021 triggered legislation that's now forcing millions of dollars in special assessments across the state. If you're buying a Florida condo as an investment, you need to understand what changed and why it matters for your bottom line.

What Did the Surfside Safety Act Change?

In May 2022, Florida passed Senate Bill 4-D, known as the Building Safety Act. It's the most significant condo legislation in Florida history, and it affects every condominium and cooperative building with three or more stories.

Here's what the law requires:

Milestone inspections. Buildings within 3 miles of the coastline must complete their first structural inspection by age 25. Inland buildings get until age 30. After the first inspection, repeat inspections happen every 10 years. The inspections must be performed by a licensed architect or engineer, and they happen in two phases — a visual exam first, then a more detailed investigation if the Phase 1 reveals problems.

Structural Integrity Reserve Studies. Every qualifying association must complete a reserve study by December 31, 2025, evaluating the condition and remaining useful life of structural components: the roof, load-bearing walls, foundation, plumbing, electrical systems, waterproofing, and exterior painting. The study estimates the cost to repair or replace each component.

Mandatory reserve funding. Here's the part that hits your wallet: associations can no longer waive or reduce reserves for structural components. Before SB 4-D, condo boards routinely voted to underfund reserves — keeping monthly fees artificially low while deferring maintenance. That option is gone as of December 31, 2024.

How Bad Are the Special Assessments?

Bad. In some cases, catastrophic for investors who didn't see them coming.

When a reserve study reveals decades of deferred maintenance and an underfunded reserve account, the association has two options: raise monthly assessments dramatically, or levy a one-time special assessment to close the gap. Many boards are doing both.

The numbers vary wildly by building age, condition, and location:

- A 1970s-era high-rise in South Florida might face $100,000–$400,000 per unit in structural repairs

- A newer mid-rise in Orlando or Tampa might see $15,000–$50,000 per unit

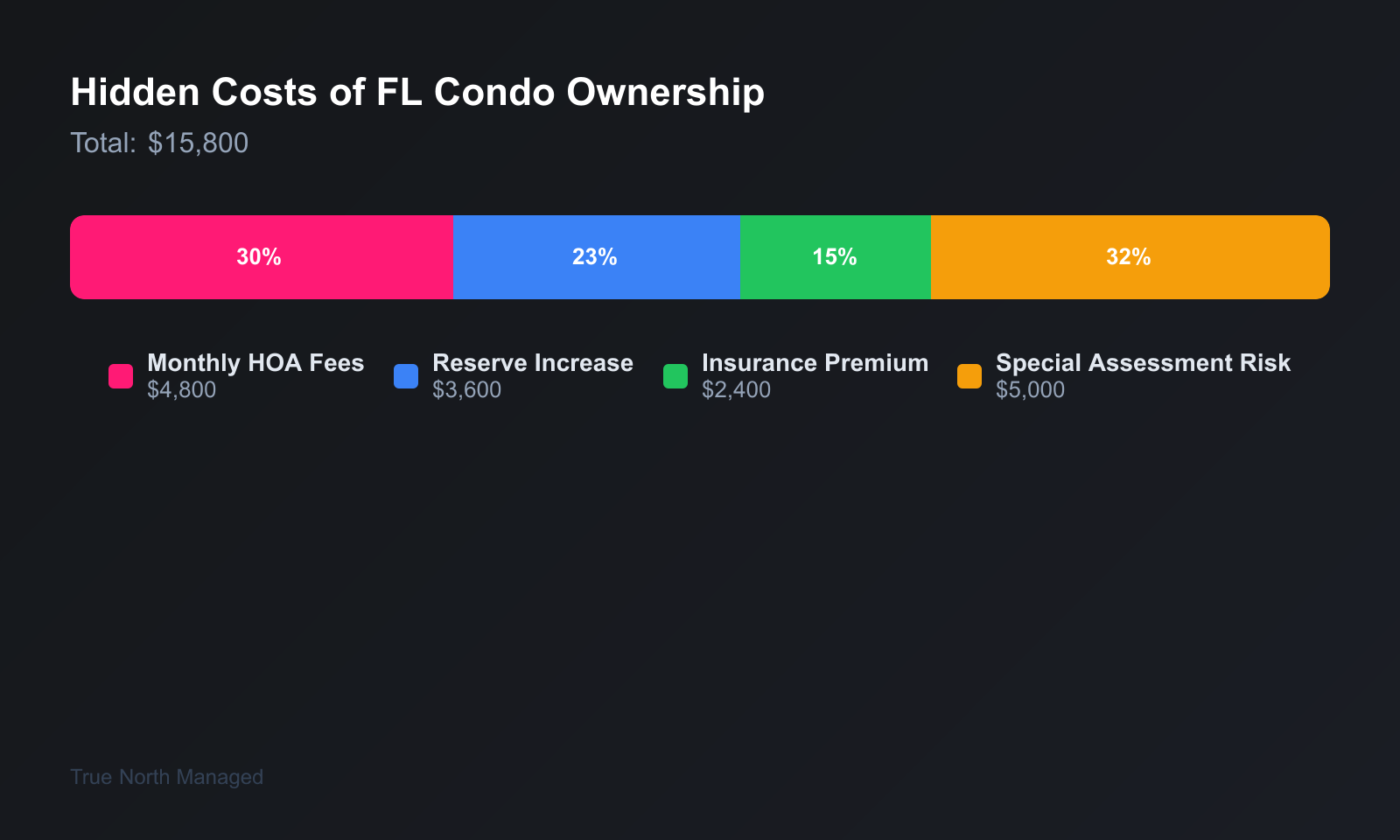

- Even well-maintained buildings are seeing assessment increases of $200–$500/month for reserve funding

For a condo investor, a $50,000 special assessment on a unit generating $1,800/month in rent destroys more than two years of gross rental income. At $100,000, you're looking at nearly five years. That's not a bad investment — that's a money pit.

What About HOA Rental Restrictions?

Beyond the structural issues, Florida HOAs have broad power to restrict rentals — and those restrictions can change after you buy.

Common rental restrictions in Florida condos: See our HOA rental restrictions in Florida for details.

- Lease term minimums. Many associations require minimum 6-month or 12-month leases, eliminating short-term rental income.

- Rental caps. Some associations limit the percentage of units that can be rented at any time — 20%, 30%, or 50% caps are common. If the cap is full when you buy, you may not be able to rent your unit at all until a spot opens.

- Approval requirements. Many boards require tenant approval, including background checks and interviews. This adds 2–4 weeks to your leasing timeline and gives the board veto power.

- Waiting periods. Some associations require new owners to occupy the unit for 1–2 years before renting.

Under Florida Statute 718, rental restrictions adopted after an owner purchases their unit generally cannot be applied retroactively — you're "grandfathered in" under the rules that existed when you bought. But this protection has limits and exceptions, and it doesn't help if the restrictions existed before you closed.

The due diligence step most investors skip: Request the association's governing documents, recent financial statements, and board meeting minutes before making an offer. The minutes will reveal upcoming assessments, maintenance plans, and any proposed rule changes.

What Does the Insurance Situation Look Like?

Florida's condo insurance market is in crisis mode. Many buildings can't get private coverage at any price and are forced onto Citizens Property Insurance — the state's insurer of last resort. Premiums have doubled or tripled for many associations over the past three years.

For individual unit owners, you need an HO-6 policy covering your interior, personal property, and liability. But the association's master policy premiums get passed through to you as part of the monthly HOA fee. If the association's premium jumps from $200,000 to $600,000 annually, your monthly fee increases by $300–$600 depending on unit count.

When you're modeling cash flow for a condo investment, don't use last year's HOA fee as your baseline. Ask the association what their current and projected insurance costs look like. If they can't answer that question, that's a red flag.

What Should You Check Before Buying a Florida Condo?

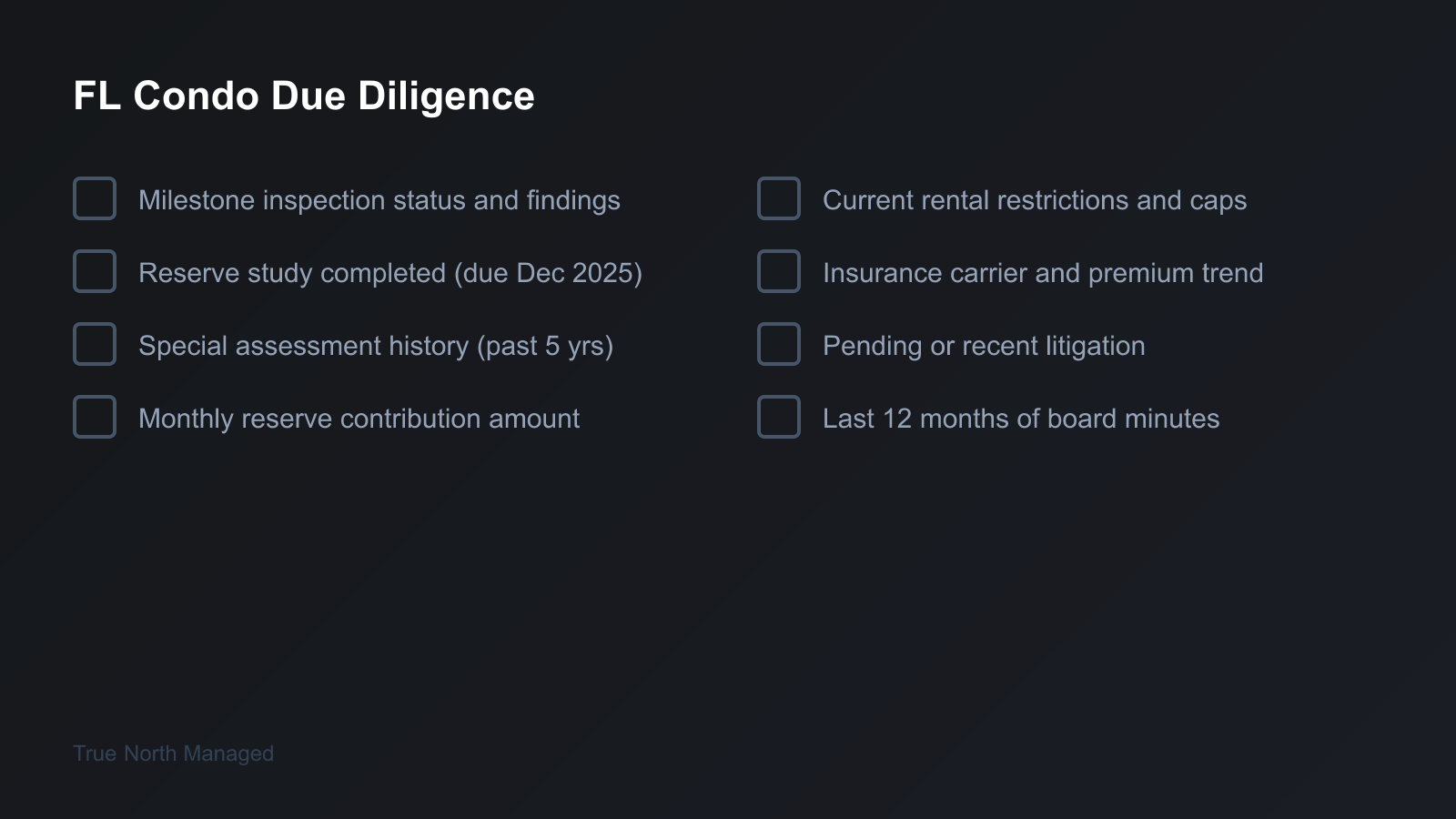

Here's the due diligence checklist that separates informed investors from people who end up on Reddit asking "can my HOA really charge me $80,000?"

- Milestone inspection status. Has the building completed its Phase 1 inspection? If so, what were the findings? If Phase 2 was required, what repairs were identified?

- Reserve study. Has the Structural Integrity Reserve Study been completed? What's the current reserve balance vs. the recommended balance? What's the funding gap?

- Special assessment history. Have any special assessments been levied in the past 5 years? Are any pending or under discussion?

- Reserve funding schedule. What's the current monthly reserve contribution? How much is it projected to increase?

- Rental restrictions. What are the current rules on leasing? Any pending amendments?

- Insurance. Who's the current carrier? What's the premium trend? Is the building on Citizens?

- Litigation. Any pending or recent lawsuits involving the association?

- Board meeting minutes. Read the last 12 months. They reveal what's actually happening, not what the listing agent tells you.

When Does Condo Investing Still Make Sense?

Not every Florida condo is a ticking assessment bomb. Newer buildings (built after 2002, when Florida building codes were significantly updated) tend to have better structural foundations. Buildings with well-funded reserves and a history of proactive maintenance are lower risk.

Condo investing can still work when:

- The building is relatively new (under 20 years) with a clean inspection record

- The reserve study shows adequate or surplus funding

- HOA fees are stable and the association has a funded reserve plan

- Rental restrictions are landlord-friendly (no caps, no waiting periods)

- The insurance market in that area isn't in crisis

But the days of buying a cheap Florida condo, ignoring the HOA, and collecting rent checks are over. The post-Surfside regulatory environment demands that investors treat condo due diligence as seriously as they'd treat a commercial property acquisition.

Frequently Asked Questions

Can my HOA change the rental rules after I buy? Generally, no — under FL 718, rental restrictions adopted after your purchase date don't apply retroactively to existing owners. But there are exceptions, particularly for amendments that receive a supermajority vote. Read the governing documents and consult an attorney before assuming you're protected.

How do I find out about pending special assessments before buying? Request the association's most recent reserve study, financial statements, and board meeting minutes. Florida law requires associations to make these available to prospective buyers. If the seller or agent can't produce them, walk away.

What's the difference between a milestone inspection and a reserve study? The milestone inspection evaluates the structural condition of the building — is it safe? The reserve study evaluates the financial planning — can the association afford to maintain and repair structural components? Both are now mandatory under SB 4-D.

Are special assessments tax deductible? It depends. Special assessments for maintenance and repairs may be deductible as operating expenses. Assessments for improvements that add value (like a new pool deck) must be added to your cost basis and depreciated. Consult your CPA.

Should I avoid all Florida condos as investments? No. Newer buildings with well-funded reserves, clean inspection records, and landlord-friendly HOA rules can still be solid investments. The risk is concentrated in older buildings with decades of deferred maintenance and underfunded reserves.

If you already own a condo investment in Florida and you're wondering how these changes affect your property, or if you're evaluating a condo purchase, get a free rental analysis to see the real numbers — including the HOA and insurance costs that make or break the deal.