Tampa Bay Flood Zones: What Landlords Need to Know Before Buying

FEMA zones A, AE, VE, X. Flood insurance requirements. Risk Rating 2.0 impact. High-risk neighborhoods and elevation certificates.

Tampa Bay Flood Zone Geography

Tampa Bay sits on a low-lying coastal plain.Storm surge, river flooding, and heavy rain create flood risk. FEMA designates flood zones that determine insurance requirements and costs. FL landlords in Orlando and Tampa should check local requirements.

Tampa Bay sits on a low-lying coastal plain. Storm surge, river flooding, and heavy rain create flood risk. FEMA designates flood zones that determine insurance requirements and costs. Before you buy a rental in South Tampa, St. Petersburg, or the coastal suburbs, check the zone. A property in the wrong zone can turn a solid investment into a money pit.

FEMA Zone Types: A, AE, VE, and X

Zone A and AE are high-risk.AE has a base flood elevation. Zone VE is coastal high-risk with wave action. FL landlords in Orlando and Tampa should check local requirements.

Zone A and AE are high-risk. AE has a base flood elevation. Zone VE is coastal high-risk with wave action. These zones typically require flood insurance if you've a mortgage. Zone X (shaded) is moderate risk. Zone X (unshaded) is minimal risk.FEMA's flood map servicelets you look up any address.Hillsborough County's flood zone viewerprovides local data. Check before you make an offer. Zones can change when FEMA updates maps. A property that was Zone X last year might be AE now.

Flood Insurance Requirements

If your property is in a high-risk zone and you've a federally backed mortgage, flood insurance is required.NFIP (National Flood Insurance Program) policies are available through floodsmart. gov . FL landlords in Orlando and Tampa should check local requirements.

If your property is in a high-risk zone and you've a federally backed mortgage, flood insurance is required. NFIP (National Flood Insurance Program) policies are available throughfloodsmart.gov. Private flood insurance is an option in some areas. Premiums depend on zone, elevation, and building characteristics. OurFlorida flood disclosure guidecovers SB 948 requirements for landlords. You must disclose flood zone status to tenants. Even if you're not in a high-risk zone, disclosure is good practice.

Risk Rating 2.0 Impact

FEMA's Risk Rating 2.0 changed how premiums are calculated. Some Tampa properties saw big premium increases. FL landlords in Orlando and Tampa should check local requirements.

FEMA's Risk Rating 2.0 changed how premiums are calculated. Some Tampa properties saw big premium increases. Others saw decreases. The new model considers more factors than the old one. Get a quote before you buy. Factor flood insurance into your operating expenses. Don't rely on what the seller paid. Your premium may be different.

High-Risk Neighborhoods and Elevation Certificates

Coastal areas, river corridors, and low-lying pockets carry higher risk.In Florida, An elevation certificate can reduce premiums if your structure is above the base flood elevation. Have one prepared when buying in a high-risk zone.

Coastal areas, river corridors, and low-lying pockets carry higher risk. An elevation certificate can reduce premiums if your structure is above the base flood elevation. Have one prepared when buying in a high-risk zone. It may pay for itself in lower insurance costs. A surveyor can produce an elevation certificate. The cost is typically $500 to $1,500. In Zone AE or VE, it's often worth it.

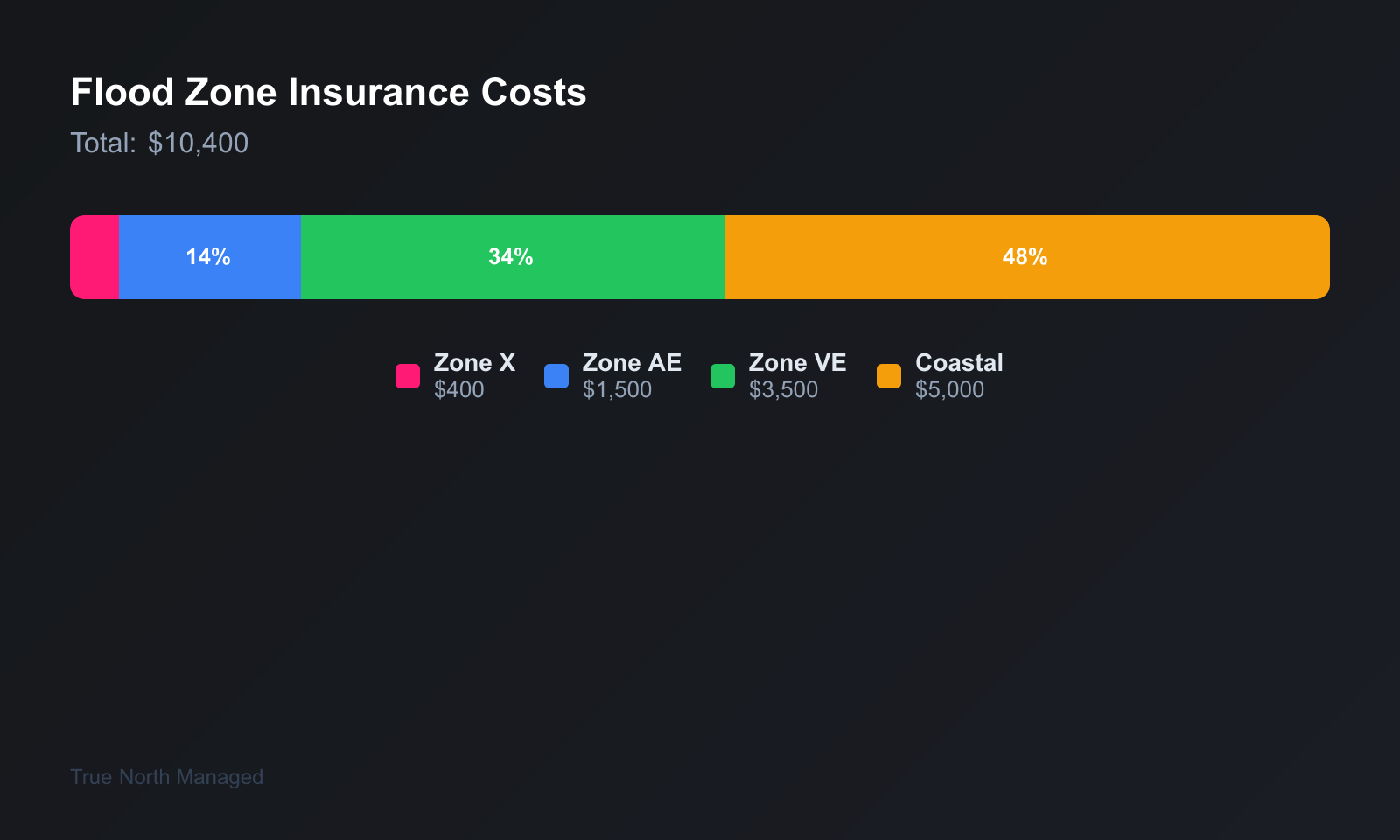

Insurance Cost Ranges

Flood insurance in Zone X can run a few hundred dollars per year.In Florida, In Zone AE or VE, expect $1,000 to $3,000 or more annually depending on coverage and elevation. Get quotes for specific properties.

Flood insurance in Zone X can run a few hundred dollars per year. In Zone AE or VE, expect $1,000 to $3,000 or more annually depending on coverage and elevation. Get quotes for specific properties. Don't assume. A property that looks like a deal can become expensive when you add flood insurance. Include flood in your pro forma. Missing it throws off your cash flow.

Flood zones are a fact of life in Tampa Bay. Know your zone, get quotes, and factor insurance into your numbers. Need help evaluating a Tampa rental?Get a free rental analysisand we'll walk you through the market.

FEMA Zones

FEMA's National Flood Hazard Layer designates zones: A, AE, V, VE, and X.Zones A and AE have 1% annual flood risk; V and VE add wave action. Zone X is minimal risk. FL landlords in Orlando and Tampa should check local requirements.

FEMA's National Flood Hazard Layerdesignates zones: A, AE, V, VE, and X. Zones A and AE have 1% annual flood risk; V and VE add wave action. Zone X is minimal risk. Lenders require flood insurance in A and V zones. Even in X zones, some landlords buy coverage. Hillsborough and Pinellas have extensive coastal and riverine flood areas.

Insurance Requirements

Flood insurance is separate from homeowner policies.NFIP policies are available through FEMA. Private flood insurance may offer better rates. FL landlords in Orlando and Tampa should check local requirements.

Flood insurance is separate from homeowner policies. NFIP policies are available through FEMA. Private flood insurance may offer better rates. Wind coverage is in the main policy; deductibles can be 2% to 5% of dwelling value in coastal zones. See ourTampa landlord insuranceguide. Ourflood disclosure guidecovers SB 948 requirements.

County Differences

X zones: lowest risk, often no flood insurance required for conventional loans.In Florida, AE and VE: higher risk, mandatory coverage. Premiums can run $1,500-$5,000/year depending on elevation and building type. FL landlords in Orlando and Tampa should check local requirements.

Insurance Rate Tiers

X zones: lowest risk, often no flood insurance required for conventional loans.In Florida, AE and VE: higher risk, mandatory coverage. Premiums can run $1,500-$5,000/year depending on elevation and building type. FL landlords in Orlando and Tampa should check local requirements.

X zones: lowest risk, often no flood insurance required for conventional loans. AE and VE: higher risk, mandatory coverage. Premiums can run $1,500-$5,000/year depending on elevation and building type. Elevation certificates can lower rates in some cases.

Elevation Certificates and Disclosure

An elevation certificate shows your structure's elevation vs base flood.Insurers use it to set rates. Cost: $500-$1,500. FL landlords in Orlando and Tampa should check local requirements.

An elevation certificate shows your structure's elevation vs base flood. Insurers use it to set rates. Cost: $500-$1,500. Florida requires sellers to disclose known flood risk. Tenants should know if the property is in a flood zone -- put it in the lease.

Elevation Certificates and What They Mean for Your Premiums

An elevation certificate is the single most valuable document for a Tampa Bay rental property in or near a flood zone.It shows your property is lowest floor relative to the Base Flood Elevation, and that difference -- measured in feet and sometimes inches -- directly determines your annual flood insurance premium. A property sitting.

An elevation certificate is the single most valuable document for a Tampa Bay rental property in or near a flood zone. It shows your property is lowest floor relative to the Base Flood Elevation, and that difference -- measured in feet and sometimes inches -- directly determines your annual flood insurance premium. A property sitting two feet above BFE might pay $800/year while the identical building one foot below BFE pays $3,200. If the seller doesn't have one, budget $300-500 for a surveyor to create it before closing.

Flood Insurance and Lending

If you're in a flood zone, your lender will require flood insurance. NFIP rates are going up—Congress has been phasing them toward actuarial risk. In Tampa Bay, a typical SFH in Zone AE might pay $1,500–$3,000 per year. Private flood can be cheaper.

Check FEMA flood maps before you buy. Zone X is minimal risk—flood insurance isn't required but is still smart. Zone AE is high risk—mandatory. Don't skip the flood determination—it affects your insurance and resale.

Elevation Certificates

In flood zones, you may need an elevation certificate for insurance. It shows your structure's elevation relative to the base flood elevation. The higher you're, the lower your premium.

Lenders require flood insurance in zones A and V. Zone X is minimal risk—insurance isn't required but is still recommended. A few inches of water can cause $20,000 in damage. Don't skip it.

Bottom Line

Check flood maps before you buy. Zone AE means mandatory insurance. NFIP or private—both work. Don't skip the flood determination.

Private flood insurance can be cheaper than NFIP in some zones. Get quotes from both. Elevation certificates matter.

When in doubt, document it. Florida landlords who follow the process and keep a paper trail protect themselves when disputes arise. A few minutes of documentation can save months of headaches.

Florida's landlord-tenant statutes—particularly Chapter 83—govern most of what you'll encounter. Familiarize yourself with the notice requirements, timelines, and documentation rules. A well-documented process protects you when disputes arise. In Orlando and Tampa, local ordinances can add layers; check your county and city rules before you act.

Hillsborough, Pinellas, and Pasco each have different flood exposure. Tampa Bay and the Gulf create coastal risk. Riverine flooding affects inland areas. Check the specific property on FEMA's map. OurOrlando landlord insuranceguide covers a market with less coastal exposure. TheTampa hublinks to neighborhood guides.