Windstorm Insurance in Florida: What Landlords Pay and Why

Windstorm coverage in Florida: Citizens vs. private carriers, cost factors, mitigation credits, and the My Safe Florida Home program.

Windstorm insurance in Florida is expensive and non-negotiable for most lenders. Landlords need to understand Citizens vs. private carriers, what drives cost, and how mitigation credits can lower premiums.

Why Windstorm Coverage Matters

Standard homeowner and landlord policies often exclude or limit wind damage in Florida. Windstorm coverage fills that gap. Lenders require it for properties in wind-borne debris regions. FL landlords in Orlando and Tampa should check local requirements. Standard homeowner and landlord policies often exclude or limit wind damage in Florida. Windstorm coverage fills that gap.

Standard homeowner and landlord policies often exclude or limit wind damage in Florida. Windstorm coverage fills that gap. Lenders require it for properties in wind-borne debris regions. FL landlords in Orlando and Tampa should check local requirements.

Standard homeowner and landlord policies often exclude or limit wind damage in Florida. Windstorm coverage fills that gap. Lenders require it for properties in wind-borne debris regions. Even without a loan, going without it in Florida is a gamble.

Citizens Property Insurance

Citizens is Florida's insurer of last resort. When private carriers won't write or charge prohibitively, Citizens steps in. Premiums are typically higher than private market when private is available. FL landlords in Orlando and Tampa should check local requirements. Citizens is Florida's insurer of last resort. When private carriers won't write or charge prohibitively, Citizens

Citizens is Florida's insurer of last resort. When private carriers won't write or charge prohibitively, Citizens steps in. Premiums are typically higher than private market when private is available. FL landlords in Orlando and Tampa should check local requirements.

Citizens is Florida's insurer of last resort. When private carriers won't write or charge prohibitively, Citizens steps in. Premiums are typically higher than private market when private is available. Depopulation efforts move policies to private carriers when they re-enter the market.

Private Market Options

Private carriers offer windstorm as part of a package or as a separate policy. In Florida, Shop annually: the market shifts. Some carriers specialize in coastal; others focus on inland. FL landlords in Orlando and Tampa should check local requirements. Private carriers offer windstorm as part of a package or as a separate policy. Shop annually: the market shifts. Some carriers specialize in coastal; others focus on inland. An independent agent who writes multiple companies can compare.

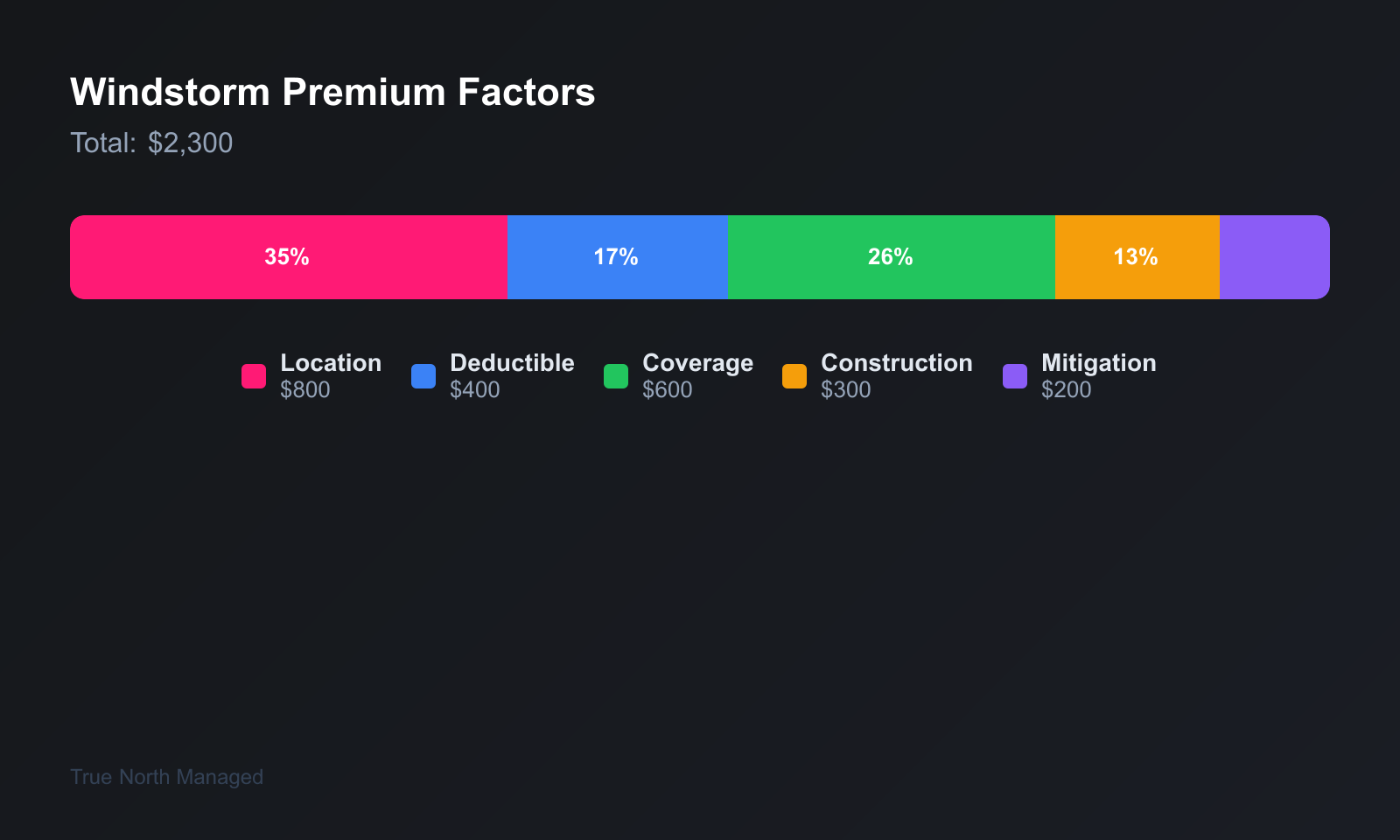

What Drives Cost

Location (coastal vs. In Florida, inland), construction (frame vs. masonry), roof type (hip vs. FL landlords in Orlando and Tampa should check local requirements. Location (coastal vs. inland), construction (frame vs. masonry), roof type (hip vs. gable), age of roof, and opening protection (shutters, impact windows). Older homes with gable roofs and no shutters cost more. Newer homes with hip roofs and impact windows cost less.

Mitigation Credits

Hip roof: Hip roofs perform better in wind than gable roofs. Many carriers offer a discount. Opening protection: Shutters or impact-resistant windows reduce wind-borne debris damage. Document what you've; insurers may require proof. Roof reinforcement: Roof-to-wall clips, secondary water barrier. A wind mitigation inspection documents these and can unlock credits. My Safe Florida Home Progr

Hip roof: Hip roofs perform better in wind than gable roofs. Many carriers offer a discount.

Opening protection: Shutters or impact-resistant windows reduce wind-borne debris damage. Document what you've; insurers may require proof.

Roof reinforcement: Roof-to-wall clips, secondary water barrier. A wind mitigation inspection documents these and can unlock credits.

My Safe Florida Home Program

The My Safe Florida Home program offers grants for hardening. Eligible improvements include roof upgrades, opening protection, and door reinforcement. Check the Florida Office of Insurance Regulation for program status and requirements. FL landlords in Orlando and Tampa should check local requirements. The My Safe Florida Home program offers grants for hardening. Eligible improvements include roof upgrades, opening protection, and door reinforcement. Check the Florida Office of Insurance Regulation for program status and requirements.

What Landlords Pay

Windstorm premiums in Florida range from $1,500 to $6,000+ annually depending on value, location, and construction. Orlando and Tampa both face hurricane exposure; coastal Tampa typically costs more. See our Tampa landlord insurance guide for market-specific details. Windstorm premiums in Florida range from $1,500 to $6,000+ annually depending on value, location, and construction. Orlando and

Windstorm premiums in Florida range from $1,500 to $6,000+ annually depending on value, location, and construction. Orlando and Tampa both face hurricane exposure; coastal Tampa typically costs more. See our Tampa landlord insurance guide for market-specific details.

Windstorm premiums in Florida range from $1,500 to $6,000+ annually depending on value, location, and construction. Orlando and Tampa both face hurricane exposure; coastal Tampa typically costs more. See our Tampa landlord insurance guide for market-specific details.

Windstorm is one piece of the insurance puzzle. Combine it with flood and liability coverage. If you're managing rentals in Orlando or Tampa, get a free rental analysis and we can help you understand total insurance costs for your property.

Filing a Wind Claim: Tips

Keep your policy documents accessible. In Florida, After a storm, you may need to reference coverage limits and deductibles quickly. Review your policy at renewal -- insurers change terms and limits. FL landlords in Orlando and Tampa should check local requirements. Keep your policy documents accessible. After a storm, you may need to reference coverage limits and deductibles quickly. Review your policy at renewal -- insurers change terms and limits. Document damage with photos before making temporary repairs. Notify your carrier promptly; most policies require notice within a set period. Keep receipts for any emergency mitigation. Don't start permanent repairs until the adjuster has inspected. Loss of rent coverage pays while the unit is uninhabitable. Our landlord insurance guide covers coverage basics.

Wind Mitigation Discounts

Impact windows, reinforced garage doors, and roof shape affect your rate. In Florida, A wind mitigation inspection ($75-150) documents these features and can cut premiums 15-40%. The inspection pays for itself in year one. FL landlords in Orlando and Tampa should check local requirements. Impact windows, reinforced garage doors, and roof shape affect your rate. A wind mitigation inspection ($75-150) documents these features and can cut premiums 15-40%. The inspection pays for itself in year one. Keep the report; insurers may request it at renewal.

What Landlords Often Miss

Loss of rent coverage. If the unit is uninhabitable after a storm, you lose income. Add it to your policy. FL landlords in Orlando and Tampa should check local requirements. Loss of rent coverage. If the unit is uninhabitable after a storm, you lose income. Add it to your policy. Ordinance or law coverage. If code requires upgrades after a partial loss, standard policies may not cover the full rebuild. Finally, adequate dwelling coverage. Replacement cost has risen. Review limits annually. For more on landlord insurance in Florida , see our guide. Comparing Orlando vs. Tampa insurance? See our insurance cost comparison .

Annual Policy Review Checklist

Florida windstorm rates change every year. Review your policy 90 days before renewal. Compare Citizens rates against private market options. FL landlords in Orlando and Tampa should check local requirements. Florida windstorm rates change every year. Review your policy 90 days before renewal. Compare Citizens rates against private market options. Confirm your deductible still fits your cash reserves. And verify the dwelling coverage matches the current replacement cost -- construction material costs have climbed steadily since 2020, and an underinsured property is worse than no policy at all. Deductibles vary. A 2% wind deductible on a $300,000 dwelling means $6,000 out of pocket before insurance pays. A 5% deductible is $15,000. Lower deductibles mean higher premiums. Run the math: if you can afford the higher deductible, the premium savings may justify it over time.

Deductibles and Coverage Gaps

Windstorm policies often have a separate hurricane deductible -- usually 2% to 5% of your dwelling coverage. In Florida, On a $300,000 policy, that's $6,000 to $15,000 out of pocket before the insurer pays. Make sure you understand your deductible before a storm hits. Windstorm policies often have a separate hurricane deductible -- usually 2%

Windstorm policies often have a separate hurricane deductible -- usually 2% to 5% of your dwelling coverage. In Florida, On a $300,000 policy, that's $6,000 to $15,000 out of pocket before the insurer pays. Make sure you understand your deductible before a storm hits.

Windstorm policies often have a separate hurricane deductible -- usually 2% to 5% of your dwelling coverage. On a $300,000 policy, that's $6,000 to $15,000 out of pocket before the insurer pays. Make sure you understand your deductible before a storm hits.

Some policies exclude certain types of damage or have sublimits for things like fencing or outbuildings. Read the exclusions. If you're in a flood zone, windstorm doesn't cover flood -- you need a separate flood policy.

Shop your policy annually. Rates change, and new carriers enter the market. A few hours of comparison can save hundreds.

Wind mitigation inspections can lower your premium. They typically cost $75-$150.

What Windstorm Coverage Actually Covers

Windstorm coverage is separate from your base policy in Florida. It covers hurricane wind damage—roof, windows, siding. It doesn't cover flood. If you're in a flood zone, you need NFIP or private flood insurance on top. Citizens Property Insurance is the insurer of last resort. Premiums are usually higher than the private market, but if

Windstorm coverage is separate from your base policy in Florida. It covers hurricane wind damage—roof, windows, siding. It doesn't cover flood. If you're in a flood zone, you need NFIP or private flood insurance on top.

Citizens Property Insurance is the insurer of last resort. Premiums are usually higher than the private market, but if you can't get coverage elsewhere, you'll end up there. In Orlando and Tampa, windstorm rates can add $1,500–$3,000 per year to a typical SFH. Shop annually.

Deductibles and Coverage Limits

In Florida, Windstorm deductibles are often percentage-based—2% or 5% of the dwelling limit. On a $300,000 policy, that's $6,000 or $15,000 out of pocket before the insurer pays. Budget for it. Replacement cost vs. actual cash value—replacement cost pays to rebuild at today's prices. ACV pays depreciated value. For a rental, replacement cost is worth

Windstorm deductibles are often percentage-based—2% or 5% of the dwelling limit. On a $300,000 policy, that's $6,000 or $15,000 out of pocket before the insurer pays. Budget for it.

Replacement cost vs. actual cash value—replacement cost pays to rebuild at today's prices. ACV pays depreciated value. For a rental, replacement cost is worth the extra premium. You want to be made whole after a storm.

Bottom Line

Windstorm coverage is mandatory in Florida. Shop annually—rates change. Understand your deductible. Replacement cost beats actual cash value for rentals.

Citizens Property Insurance is the insurer of last resort. Premiums are usually higher. Shop the private market first.

When in doubt, document it. Florida landlords who follow the process and keep a paper trail protect themselves when disputes arise. A few minutes of documentation can save months of headaches.

Florida's landlord-tenant statutes—particularly Chapter 83—govern most of what you'll encounter. Familiarize yourself with the notice requirements, timelines, and documentation rules. A well-documented process protects you when disputes arise. In Orlando and Tampa, local ordinances can add layers; check your county and city rules before you act.

True North Managed helps Orlando and Tampa landlords handle these issues every day. When you need local expertise, we're here.

Shop around. Rates vary by carrier.

If you own a rental in Orlando or Tampa and want a clear picture of what it could earn, get a free rental analysis. No obligation—just real numbers.