How to Read a Rental Property Pro Forma (and Spot the Lies)

A line-by-line pro forma breakdown for Florida rentals: common inflated assumptions, realistic numbers, and red flags when buying.

Red Flag Summary

Request a T-12 (trailing 12 months) and compare the pro forma to actuals after you buy. In Florida, Track variance. Your own data becomes more valuable than generic assumptions for the next deal. FL landlords in Orlando and Tampa should check local requirements. Compare the pro forma to actuals after you buy. Track variance. Your

Request a T-12 (trailing 12 months) and compare the pro forma to actuals after you buy. In Florida, Track variance. Your own data becomes more valuable than generic assumptions for the next deal. FL landlords in Orlando and Tampa should check local requirements.

Compare the pro forma to actuals after you buy. Track variance. Your own data becomes more valuable than generic assumptions for the next deal.

Walk away from pro formas with rent at or above market with no comps, vacancy below 5% in an 8% market, expense ratios under 35%, or no cap ex reserve. Always ask for the source of every number. See our deal analysis guide for the full framework.

A pro forma is a projected income and expense statement for a rental property. Sellers and agents use them to justify asking prices. Savvy buyers know they're often optimistic. Here's how to read one and spot the lies.

Income: The First Place to Look

In Florida, Gross rent: Is it current lease rent or "market" rent? If the unit is vacant or leased below market, the pro forma may show what it "could" rent for. Verify with comps. Orlando and Tampa rents vary by submarket; a Lake Nona number doesn't apply to Dr. Phillips. Other income: Laundry, parking, pet

Gross rent: Is it current lease rent or "market" rent? If the unit is vacant or leased below market, the pro forma may show what it "could" rent for. Verify with comps. Orlando and Tampa rents vary by submarket; a Lake Nona number doesn't apply to Dr. Phillips.

Other income: Laundry, parking, pet rent. Only include what's actually in place or easily achievable. Don't assume you'll add $50 pet rent if the current lease doesn't allow it.

Vacancy: Pro formas often use 5% or less. Florida multifamily vacancy runs 6–10% depending on submarket. Use 8% for a conservative model.

Expenses: Where Assumptions Hide

Property management: Budget 8–10% of gross rent. Pro formas sometimes use 6% or omit it. If you'll self-manage, that's fine, but don't compare your pro forma to one that includes management. Maintenance and repairs: 1% of property value annually is a floor. Older properties need more. Pro formas often use 0.5% or a flat number that doesn't scale. Insurance: Use Florida numbers. Landlord insurance plus wind and flood can add up. Get quotes from an agent, not a national average. Property tax: Verify the current assessed value. Florida reassessments can jump after a sale.

Red Flags

Rent at or above the top of the market range. In Florida, Expense ratios below 35% of gross income. No vacancy allowance. FL landlords in Orlando and Tampa should check local requirements. Rent at or above the top of the market range. Expense ratios below 35% of gross income. No vacancy allowance. No capital reserve for roof, HVAC, or major systems. Cap rate above 7% for a turnkey property in a decent area. If it looks too good, it usually is. See our hidden costs of rental ownership for a full list of what sellers often omit.

Realistic Florida Numbers

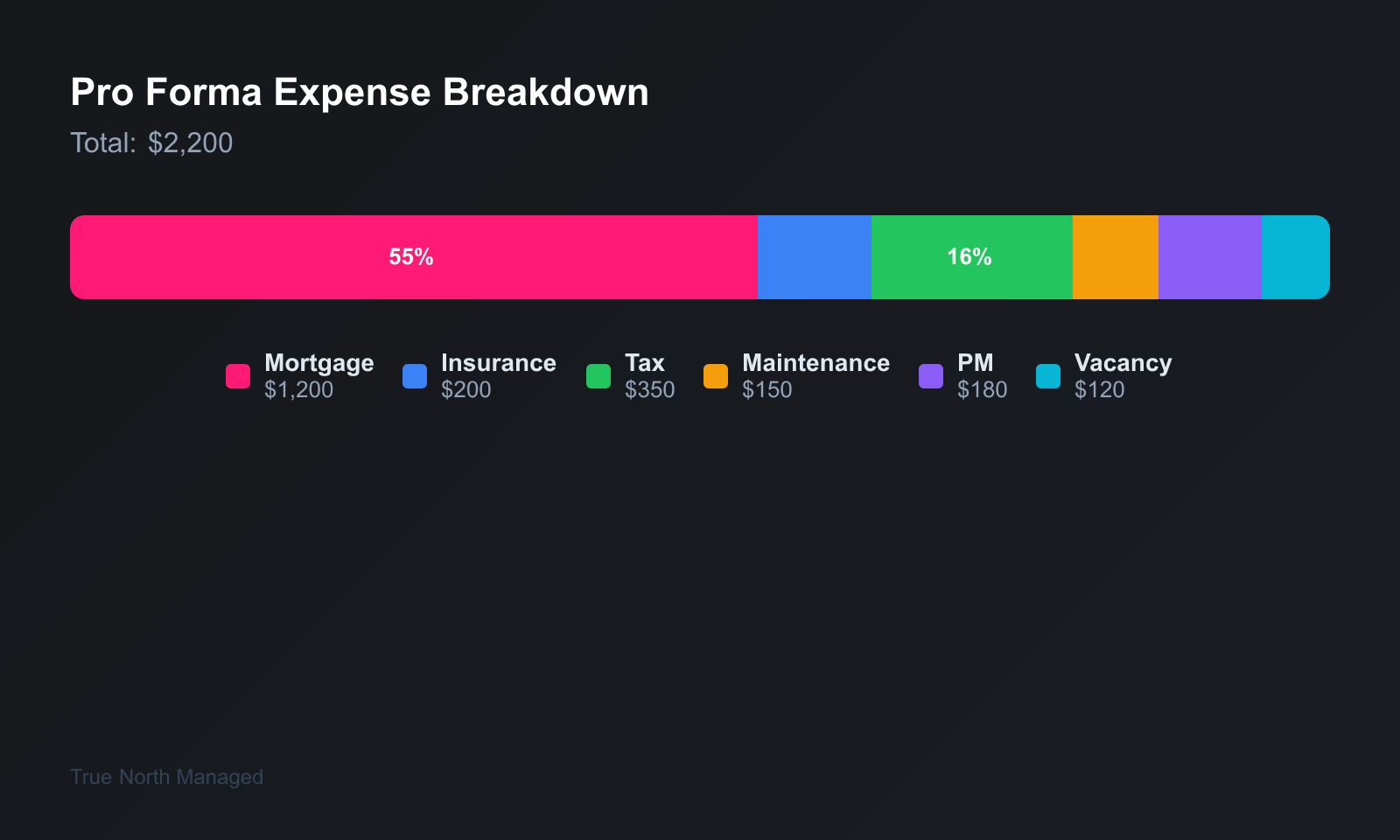

In Florida, For a $300,000 Orlando duplex renting for $2,400/month: gross income $28,800, vacancy at 8% = $2,304, effective gross $26,496. Expenses: taxes ~$4,500, insurance ~$3,500, maintenance ~$3,000, management ~$2,400, reserves ~$1,500. Total expenses ~$14,900. FL landlords in Orlando and Tampa should check local requirements. For a $300,000 Orlando duplex renting for $2,400/month: gross income

For a $300,000 Orlando duplex renting for $2,400/month: gross income $28,800, vacancy at 8% = $2,304, effective gross $26,496. Expenses: taxes ~$4,500, insurance ~$3,500, maintenance ~$3,000, management ~$2,400, reserves ~$1,500. Total expenses ~$14,900. FL landlords in Orlando and Tampa should check local requirements.

For a $300,000 Orlando duplex renting for $2,400/month: gross income $28,800, vacancy at 8% = $2,304, effective gross $26,496. Expenses: taxes ~$4,500, insurance ~$3,500, maintenance ~$3,000, management ~$2,400, reserves ~$1,500. Total expenses ~$14,900. NOI ~$11,600. Cap rate ~3.9%. That's tight for an appreciation play; adjust your assumptions and see how it breaks.

Run your own numbers. Use the Owner's Guide for more on investment analysis. If you're evaluating a purchase in Orlando or Tampa, get a free rental analysis and we can build a realistic pro forma with current market data.

Red Flags in Pro Formas

Rent at or above market with no supporting data. In Florida, Vacancy below 5% in a market where 8% is typical. Expense ratios under 35% when similar properties run 45--50%. FL landlords in Orlando and Tampa should check local requirements. Rent at or above market with no supporting data. Vacancy below 5% in a market where 8% is typical. Expense ratios under 35% when similar properties run 45–50%. No cap ex reserve. Repairs and replacements are real. Pro formas that ignore them inflate returns. Always ask for the source of every number.

How to Stress-Test a Pro Forma

Bump vacancy to 8--10%. In Florida, Add 0. 5% of value for cap ex. FL landlords in Orlando and Tampa should check local requirements. Bump vacancy to 8–10%. Add 0.5% of value for cap ex. Use actual insurance and tax numbers from the county and recent quotes. If the deal still works, it's solid. If it falls apart, walk away. See our deal analysis guide for the full framework.

Florida-Specific Adjustments

Insurance costs more in Florida than most states. Orlando and Tampa landlords should follow FL statutes and local ordinances. FL landlords in Orlando and Tampa should check local requirements. Insurance costs more in Florida than most states. Budget 1.5–2.5% of value annually. Hurricane deductibles is 2–5% of dwelling value. HOA fees in condos often include wind and flood. Factor in hidden costs before you buy. For Orlando and Tampa market context, see our hub pages. Bottom line: stress-test every number. Bump vacancy, add cap ex, use actual insurance and tax. If the deal dies, walk away. Florida insurance and hurricane deductibles make pro formas optimistic—adjust for reality. Always ask for the source of every assumption. Ask the seller for 12 months of actual expenses. Utility bills, insurance invoices, tax statements. If they won't provide them, that's a red flag. Verify every number you can. Pro formas are marketing documents. Your job is to turn them into realistic projections.

When the Numbers Say No

Not every deal pencils out -- and that's the whole point of running a pro forma. If projected cash flow falls below 6% cash-on-cash return after conservative expense estimates, most experienced Florida investors walk away. The discipline to say no to a mediocre deal protects your portfolio more than any single property can grow it.

Common Mistakes to Avoid

One of the biggest mistakes we see: skipping the written notice. Florida law is strict about documentation. If you don't have a paper trail—or email trail that meets SB 716's requirements—you can lose an eviction or deposit dispute. Document everything. Another mistake: underbudgeting for turnover. A typical Florida turnover runs $1,500–$3,000 when you include paint,

One of the biggest mistakes we see: skipping the written notice. Florida law is strict about documentation. If you don't have a paper trail—or email trail that meets SB 716's requirements—you can lose an eviction or deposit dispute. Document everything.

Another mistake: underbudgeting for turnover. A typical Florida turnover runs $1,500–$3,000 when you include paint, carpet, cleaning, and minor repairs. If you're only setting aside 5% of rent for maintenance, you're short. Plan for 8–12% in year one until you know your property.

Third: treating every tenant the same. A military family near MacDill has different needs than a UCF grad student. Screen for fit, not just credit score. The right tenant in the right property stays longer and costs you less.

Florida-Specific Considerations

Florida Statute 83 applies to residential tenancies. Know the notice requirements: 3 days for non-payment (soon 5 under SB 716), 7 days for cure or vacate for lease violations, 15 days for month-to-month termination. Wrong notice = delayed eviction.

Insurance is another Florida reality. Wind and flood can double your premium in certain zones. Run quotes before you buy. A $200/month insurance difference changes your cash flow by $2,400/year.

Finally, property taxes. Homestead doesn't apply to rentals. You'll pay non-homestead rates. In Florida County, that's typically 1.2–1.5% of assessed value. Appeal if your assessment seems high—many landlords overpay.

When to Get Help

If you're out of state, hire a local property manager. The 8–10% fee pays for itself in faster leasing, better screening, and someone who can show up when the AC dies at 10 PM. Self-managing from another state is a recipe for deferred maintenance and tenant frustration.

For legal issues—evictions, deposit disputes, lease breaks—consult a Florida-licensed attorney. Landlord-tenant law has traps. A $500 consult can save you $5,000 in a botched eviction. We've seen it.

Finally, for complex financial decisions—1031 exchanges, LLC structuring, depreciation—talk to a CPA who works with rental owners. The tax code rewards those who plan. Don't wing it.

When to Get Help

If you're out of state, hire a local property manager. The 8–10% fee pays for itself in faster leasing, better screening, and someone who can show up when the AC dies at 10 PM. Self-managing from another state is a recipe for deferred maintenance and tenant frustration.

For legal issues—evictions, deposit disputes, lease breaks—consult a Florida-licensed attorney. Landlord-tenant law has traps. A $500 consult can save you $5,000 in a botched eviction. We've seen it.

Finally, for complex financial decisions—1031 exchanges, LLC structuring, depreciation—talk to a CPA who works with rental owners. The tax code rewards those who plan. Don't wing it.

Not every deal pencils out -- and that's the whole point of running a pro forma. If projected cash flow falls below 6% cash-on-cash return after conservative expense estimates, most experienced Florida investors walk away. The discipline to say no to a mediocre deal protects your portfolio more than any single property can grow it.

Compare the pro forma to actuals after you buy. Track variance. If expenses run 10% higher than projected, adjust your model for the next deal. Your own data becomes more valuable than generic assumptions. First-year actuals are the best education for underwriting the next property.

If you own a rental in Orlando or Tampa and want a clear picture of what it could earn, get a free rental analysis. No obligation—just real numbers.