Cap Rate vs. Cash-on-Cash Return: Which Matters More in Florida?

Cap rate and cash-on-cash return measure different things. Here's when each matters for Florida rental investors, with Orlando and Tampa examples.

Run both metrics for every deal. Cap rate screens value; cash-on-cash validates your financing.

Two numbers show up in every rental investment conversation: cap rate and cash-on-cash return. They measure different things. For Florida investors, knowing when to use each prevents bad buys and clarifies good ones.

what's Cap Rate?

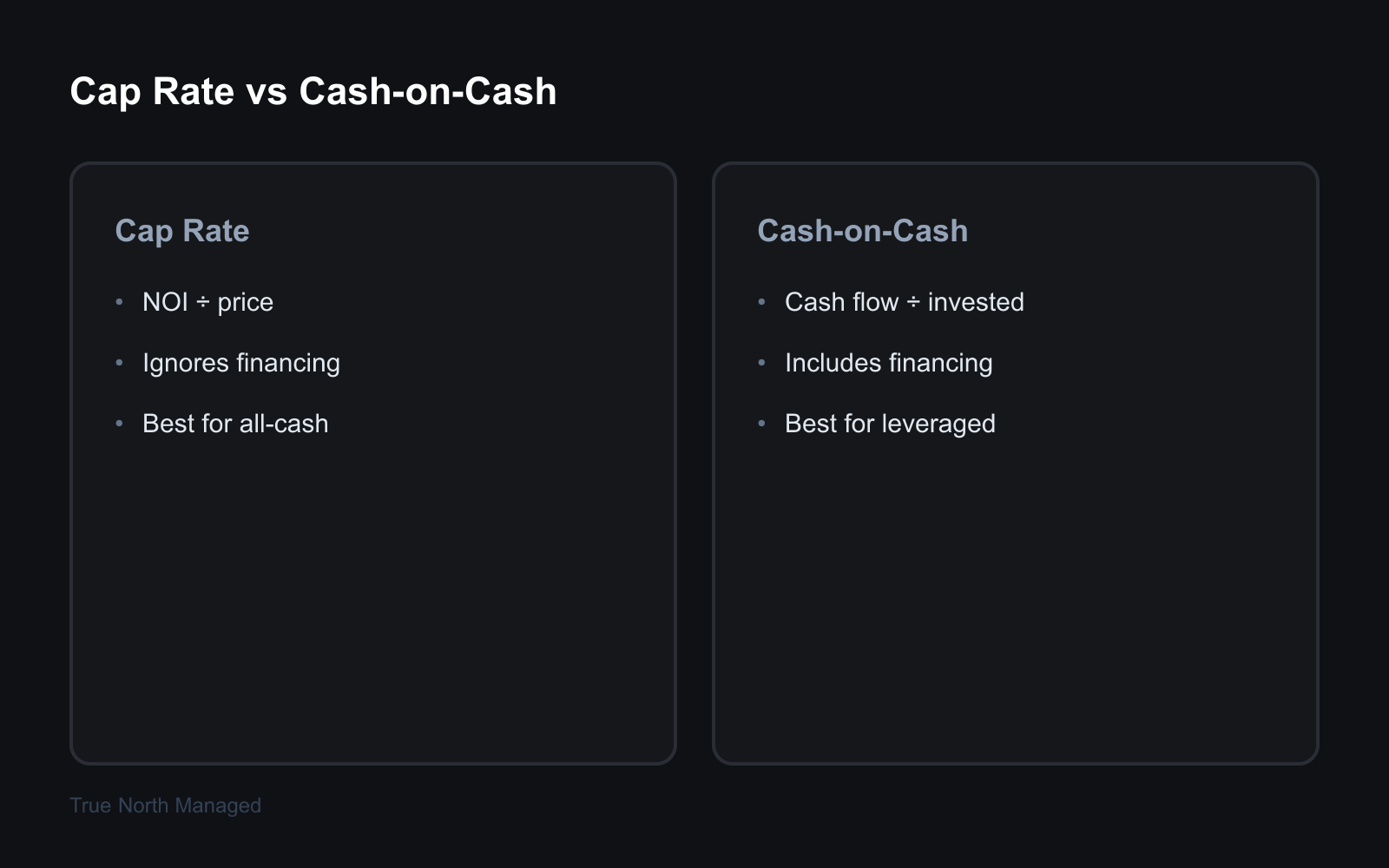

In Florida, Cap rate is the property's return if you bought all cash: NOI / Purchase Price ( formulas and comparison ). A $250K Orlando property with $12,500 NOI has a 5% cap rate. It's a market-comparison metric, not a financing metric. Cap rate (capitalization rate) = (Net Operating Income / Property Value) × 100.

Cap rate is the property's return if you bought all cash: NOI / Purchase Price (formulas and comparison). A $250K Orlando property with $12,500 NOI has a 5% cap rate. It's a market-comparison metric, not a financing metric.

Cap rate (capitalization rate) = (Net Operating Income / Property Value) × 100. It answers: what yield does this property produce if I paid all cash? NOI is gross rent minus operating expenses (taxes, insurance, maintenance, management, utilities you pay). It excludes mortgage payments and depreciation.

Example: An Orlando duplex generates $2,200/month ($26,400/year) in rent. Operating expenses run $9,500/year. NOI = $16,900. The property is worth $320,000. Cap rate = 5.3%.

Florida residential cap rates typically run 4–6%. Below 4% usually means appreciation play or premium location. Above 6% often signals higher risk: older building, rougher area, or deferred maintenance.

what's Cash-on-Cash Return?

In Florida, Cash-on-cash is your return on the money you actually put in. If you put $50K down and get $3K/year in cash flow, that's 6% CoC. It reflects use and financing. Cash-on-cash = (Annual Pre-Tax Cash Flow / Total Cash Invested) × 100. It answers: what return am I getting on the money I

Cash-on-cash is your return on the money you actually put in. If you put $50K down and get $3K/year in cash flow, that's 6% CoC. It reflects use and financing.

Cash-on-cash = (Annual Pre-Tax Cash Flow / Total Cash Invested) × 100. It answers: what return am I getting on the money I actually put in? Cash flow is NOI minus debt service. Cash invested is down payment, closing costs, and any upfront rehab.

Example: Same duplex. You put $80,000 down (25%), pay $1,400/month in principal and interest. Annual debt service = $16,800. Cash flow = $16,900 − $16,800 = $100/year. Cash-on-cash = 0.1%. Terrible. But if you put 20% down and rates were lower, cash flow is $3,000/year. Cash-on-cash = 3.75%.

When Cap Rate Matters More

In Florida, Cap rate matters more when comparing similar properties or when you're buying all cash. Orlando and Tampa investors use cap rates to screen deals and compare across markets. Cap rate is property-centric. It tells you what the asset earns regardless of financing. Use it when comparing similar properties, evaluating a seller's asking price,

Cap rate matters more when comparing similar properties or when you're buying all cash. Orlando and Tampa investors use cap rates to screen deals and compare across markets.

Cap rate is property-centric. It tells you what the asset earns regardless of financing. Use it when comparing similar properties, evaluating a seller's asking price, or sizing up a market. A 5% cap in Orlando vs. 4.5% in Tampa suggests different risk or growth expectations.

Cap rate also helps when you're modeling all-cash or planning to refinance. See our Orlando vs Tampa rental comparison for more on market-level differences.

When Cash-on-Cash Matters More

Cash-on-cash matters more when you're leveraged and care about your actual return. A 4% cap rate can become 8% CoC with 50% LTV. Florida's financing options make CoC relevant. Cash-on-cash is investor-centric. It reflects your actual return after use. If you're financing, this is the number that matters for day-to-day decisions. A 5% cap with

Cash-on-cash matters more when you're leveraged and care about your actual return. A 4% cap rate can become 8% CoC with 50% LTV. Florida's financing options make CoC relevant.

Cash-on-cash is investor-centric. It reflects your actual return after use. If you're financing, this is the number that matters for day-to-day decisions. A 5% cap with 80% LTV might produce 2% cash-on-cash; the same cap -- with 50% LTV could produce 6%.

Common Mistakes

Using pro forma rent instead of actual rent: Pro formas often inflate income. Use current leases or realistic market rent. Underestimating expenses: Florida insurance, property taxes, and maintenance add up. Budget 8–12% of rent for management, 1% of value annually for maintenance. Ignoring vacancy: Orlando and Tampa vacancy rates vary by submarket. Factor 5–8% vacancy into your NOI. Both metrics have a place. Cap rate for property and market comparison; cash-on-cash for your personal returns. For more on evaluating Florida rentals, see our Owner's Guide . If you're considering a purchase in Orlando or Tampa, get a free rental analysis and we can run the numbers with real market data.

When Cap Rate Matters More

Use cap rate for apples-to-apples comparison. Same submarket, same property type. Orlando cap rates differ from Tampa -- compare within each. Cap rate ignores financing. It's useful when comparing similar properties or when you're paying cash. A 6% cap in Orlando vs. 5% in Tampa tells you which market offers better value per dollar of NOI. Investors also use cap rates to value a property: NOI divided by cap rate equals value. A $24,000 NOI at 6% cap suggests a $400,000 value.

When Cash-on-Cash Matters More

Use CoC for your personal return. Your down payment, your rate, your cash flow. That's what hits your pocket. Cash-on-cash includes your financing. If you put 25% down and finance the rest, your return on that cash is what matters. A 5% cap rate property can deliver 12% cash-on-cash with use. Use it when comparing deals with different down payments or loan terms . See our deal analysis guide for the full math.

Florida Market Context

Florida context: Orlando and Tampa cap rates typically run 4-6% for residential. Insurance and taxes push expenses up. Run comps for your specific submarket. Orlando and Tampa cap rates typically run 5–7% for SFHs and small multis. Lower than many Midwest markets, but appreciation and rent growth have been stronger. Run both metrics. Cap rate tells you if the price is fair; cash-on-cash tells you if the deal works for your situation. For more on reading a pro forma , see our guide. Bottom line: run both. Cap rate tells you if the price is fair relative to NOI. Cash-on-cash tells you if the deal works for your financing. Orlando and Tampa typically run 5–7% caps. use can turn a 5% cap into 12% cash-on-cash. See our pro forma guide for the full picture.

Common Mistakes to Avoid

One of the biggest mistakes we see: skipping the written notice. Florida law is strict about documentation. If you don't have a paper trail—or email trail that meets SB 716's requirements—you can lose an eviction or deposit dispute. Document everything. Another mistake: underbudgeting for turnover. A typical Florida turnover runs $1,500–$3,000 when you include paint,

One of the biggest mistakes we see: skipping the written notice. Florida law is strict about documentation. If you don't have a paper trail—or email trail that meets SB 716's requirements—you can lose an eviction or deposit dispute. Document everything.

Another mistake: underbudgeting for turnover. A typical Florida turnover runs $1,500–$3,000 when you include paint, carpet, cleaning, and minor repairs. If you're only setting aside 5% of rent for maintenance, you're short. Plan for 8–12% in year one until you know your property.

Third: treating every tenant the same. A military family near MacDill has different needs than a UCF grad student. Screen for fit, not just credit score. The right tenant in the right property stays longer and costs you less.

Florida-Specific Considerations

Florida Statute 83 applies to residential tenancies. Know the notice requirements: 3 days for non-payment (soon 5 under SB 716), 7 days for cure or vacate for lease violations, 15 days for month-to-month termination. Wrong notice = delayed eviction.

Insurance is another Florida reality. Wind and flood can double your premium in certain zones. Run quotes before you buy. A $200/month insurance difference changes your cash flow by $2,400/year.

Finally, property taxes. Homestead doesn't apply to rentals. You'll pay non-homestead rates. In Florida County, that's typically 1.2–1.5% of assessed value. Appeal if your assessment seems high—many landlords overpay.

When to Get Help

If you're out of state, hire a local property manager. The 8–10% fee pays for itself in faster leasing, better screening, and someone who can show up when the AC dies at 10 PM. Self-managing from another state is a recipe for deferred maintenance and tenant frustration.

For legal issues—evictions, deposit disputes, lease breaks—consult a Florida-licensed attorney. Landlord-tenant law has traps. A $500 consult can save you $5,000 in a botched eviction. We've seen it.

Finally, for complex financial decisions—1031 exchanges, LLC structuring, depreciation—talk to a CPA who works with rental owners. The tax code rewards those who plan. Don't wing it.

When to Get Help

If you're out of state, hire a local property manager. The 8–10% fee pays for itself in faster leasing, better screening, and someone who can show up when the AC dies at 10 PM. Self-managing from another state is a recipe for deferred maintenance and tenant frustration.

For legal issues—evictions, deposit disputes, lease breaks—consult a Florida-licensed attorney. Landlord-tenant law has traps. A $500 consult can save you $5,000 in a botched eviction. We've seen it.

Finally, for complex financial decisions—1031 exchanges, LLC structuring, depreciation—talk to a CPA who works with rental owners. The tax code rewards those who plan. Don't wing it.

When to Get Help

If you're out of state, hire a local property manager. The 8–10% fee pays for itself in faster leasing, better screening, and someone who can show up when the AC dies at 10 PM. Self-managing from another state is a recipe for deferred maintenance and tenant frustration.

For legal issues—evictions, deposit disputes, lease breaks—consult a Florida-licensed attorney. Landlord-tenant law has traps. A $500 consult can save you $5,000 in a botched eviction. We've seen it.

Finally, for complex financial decisions—1031 exchanges, LLC structuring, depreciation—talk to a CPA who works with rental owners. The tax code rewards those who plan. Don't wing it.

Use cap rate to screen deals quickly. If the cap is below 4% in your target market, the price is too high. Use cash-on-cash to validate that your specific financing works. Both matter. Ignoring either can lead to a deal that looks good on -- paper but fails in practice.

Neither metric is perfect. Cap rate ignores your financing. Cash-on-cash ignores appreciation and principal paydown. Use both, plus rent-to-value and DSCR. A deal that passes all four is stronger than one that passes one. See our full deal analysis for the complete framework.

If you own a rental in Orlando or Tampa and want a clear picture of what it could earn, get a free rental analysis. No obligation—just real numbers.