The Complete Tenant Screening Process for Florida Landlords

Florida landlords can run credit checks, background checks, income verification, and landlord references — but every step has legal guardrails. Here's the full process, from application to approval.

The Complete Tenant Screening Process for Florida Landlords

You've got a vacancy and applications are coming in. Maybe this is your first time screening tenants, or maybe you've been doing it for years but aren't sure if your process would survive a fair housing complaint. Either way, the screening process for Florida landlords has specific legal requirements that most online guides gloss over.

Here's the short version: you can check credit, criminal history, income, employment, and rental references — but you need written consent first, you have to apply the same criteria to every applicant, and you can't ask questions that touch on protected classes. Skip any of these, and you're exposed.

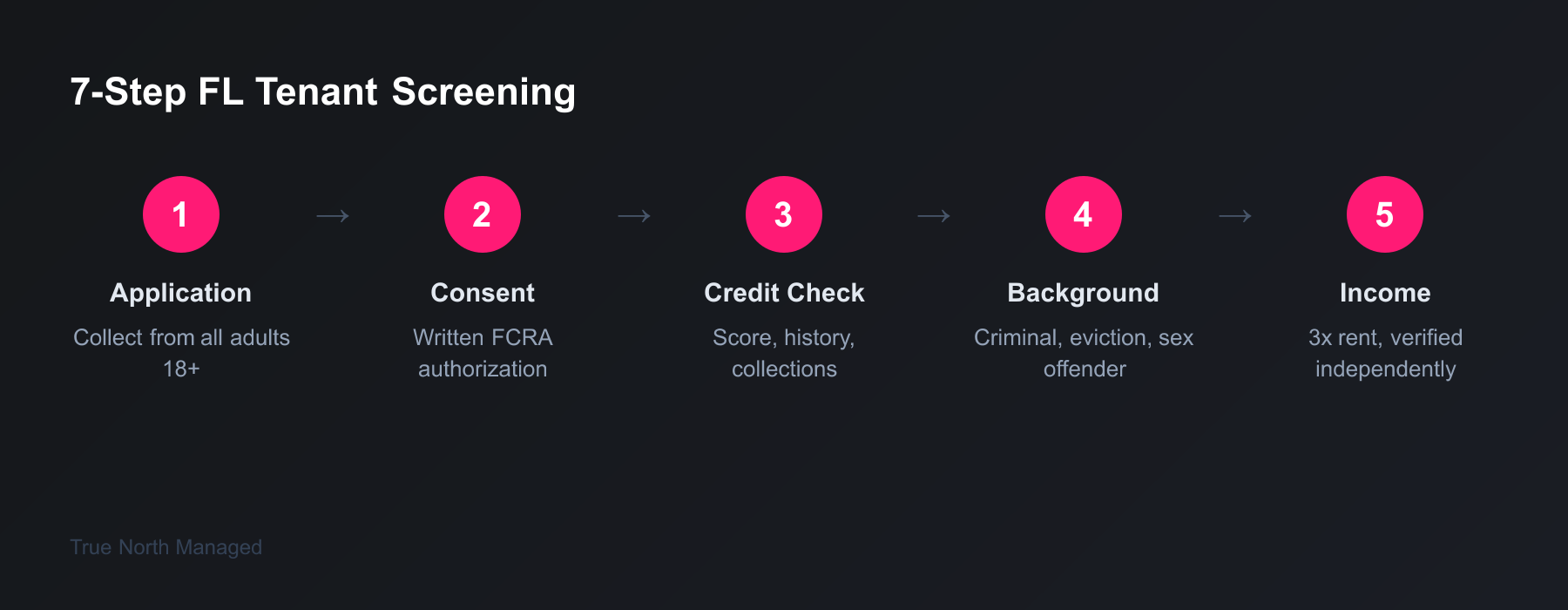

Let's walk through each step.

What Should You Require on the Application?

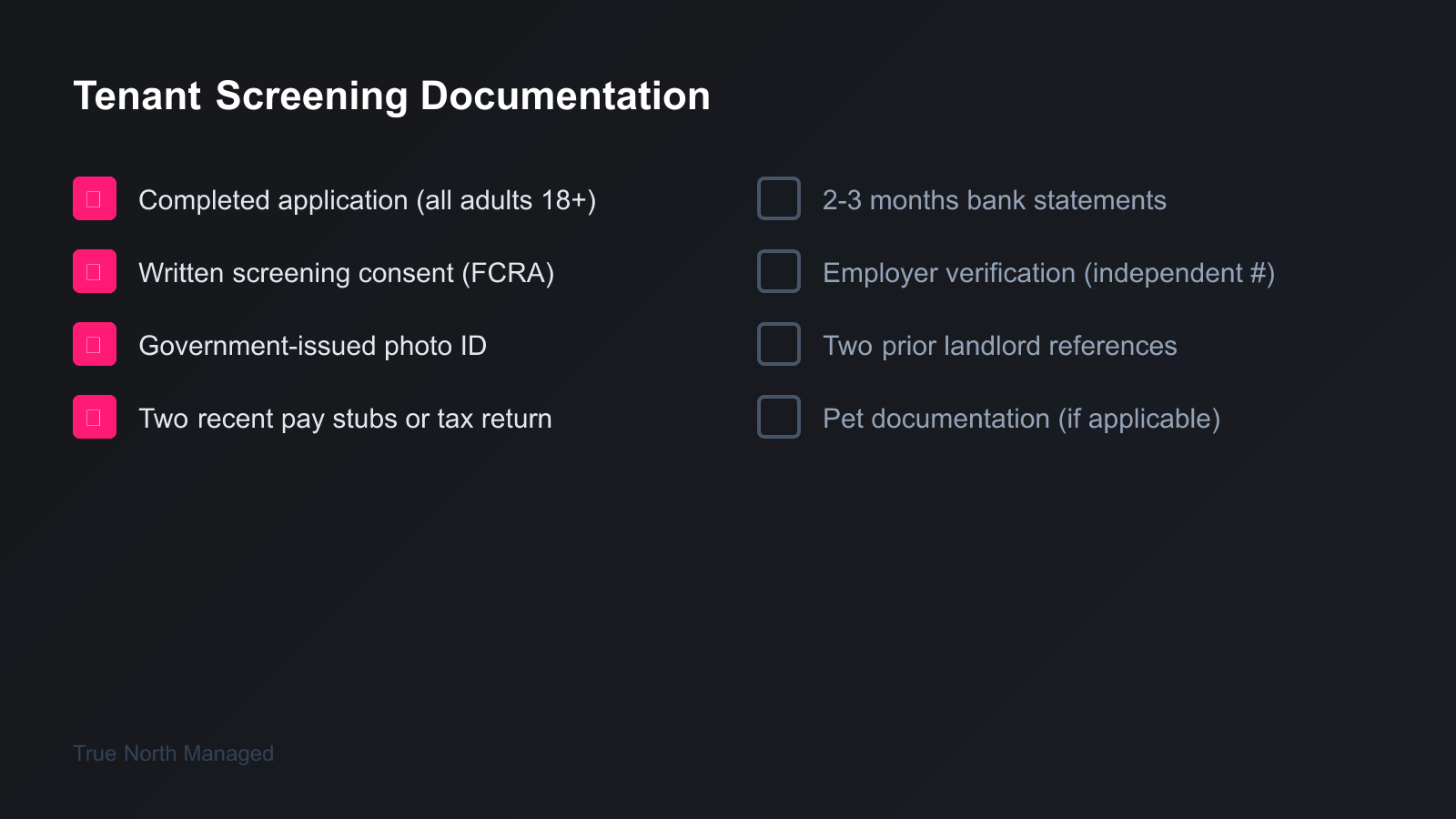

A solid rental application collects enough information to make a fair, informed decision — and nothing that could create legal exposure. Every adult (18+) who will live in the property needs to fill one out.

Your application should include:

- Full legal name, date of birth, and Social Security number (for credit/background checks)

- Current and previous addresses for the past 3–5 years

- Current employer, job title, monthly income, and employment duration

- Previous landlord contact information (at least two prior landlords)

- Emergency contact

- Pet information (number, type, breed, weight)

- Vehicle information (if applicable for parking)

- Authorization to run credit and background checks

That last item — the authorization — isn't optional. The Fair Credit Reporting Act (FCRA) requires written consent before you pull a credit report or run a background check. No signature, no screening.

Application fees. Florida has no statutory cap on application fees, but the fee should be reasonable and reflect your actual screening costs. Most landlords charge $50–$75 per applicant. Charging $200 and pocketing the difference is the kind of thing that draws complaints.

How Do Credit and Background Checks Work?

Credit and criminal background checks are the backbone of tenant screening. They're where you learn what the applicant's behavior has been — not just what they tell you on the application.

Credit checks give you a credit score, payment history, outstanding debts, collections, and any bankruptcies or judgments. You're not looking for a perfect score. You're looking for patterns.

A 680 with steady payment history tells a different story than a 720 with two recent collections and a maxed-out credit card. The score alone isn't enough — read the report.

What to watch for:

- Eviction records or landlord judgments

- Recent collections (especially utility or rent-related)

- Debt-to-income ratio above 40%

- Multiple hard inquiries in a short period (could signal financial stress)

Background checks cover criminal history, sex offender registry, and eviction records. Florida doesn't restrict criminal background screening as heavily as some states, but there are guardrails.

You cannot implement a blanket ban on all applicants with a criminal record — HUD guidance says that approach creates disparate impact and can violate the Fair Housing Act. Instead, evaluate each case based on the nature of the offense, how long ago it occurred, and whether it's relevant to tenancy.

Convictions matter. Arrests without convictions don't — you shouldn't use them as screening criteria.

Screening services. TransUnion SmartMove, RentPrep, MyRental, and AppFolio's built-in screening are the most common tools. Costs run $25–$50 per report, typically passed through to the applicant as part of the application fee.

How Do You Verify Income and Employment?

The industry standard is 3x monthly rent in gross income. On a $2,000/month rental, that means the applicant (or combined applicants on a joint lease) should earn at least $6,000/month before taxes.

What to request:

- Two most recent pay stubs

- Bank statements (last 2–3 months)

- Tax returns (for self-employed applicants)

- Employment verification letter or direct employer contact

Verification steps:

- Call the employer directly using a number you find independently — not the one on the application. Applicants with fake pay stubs will give you a buddy's phone number.

- For self-employed applicants, request Schedule C from their most recent tax return and at least 6 months of bank statements showing consistent deposits.

- For applicants relying on non-employment income (Social Security, disability, retirement, alimony), request documentation of the income source and verify amounts.

A common mistake: accepting screenshots of bank account balances. Anyone can manipulate a screenshot. Request official bank statements with the institution's header, or verify through a third-party verification service.

What Should You Ask Previous Landlords?

Landlord references are where you learn things credit reports can't tell you. But most landlords ask the wrong questions — or accept vague answers that tell them nothing.

Questions that actually reveal problems:

- Did the tenant pay rent on time? (If the answer is "usually" — dig deeper. How many times was it late? By how much?)

- Did the tenant comply with the lease terms? (This catches unauthorized occupants, pets, and noise issues.)

- Was there any property damage beyond normal wear and tear? (Ask for specifics.)

- Did the tenant give proper notice before moving out?

- Would you rent to this tenant again? (This is the killer question. Hesitation here tells you everything.)

Red flags in landlord references:

- The "landlord" turns out to be a friend or family member. Verify ownership through the county property appraiser's website.

- The current landlord gives a glowing review. They might be trying to get rid of a bad tenant. Contact the landlord before the current one for a more honest assessment.

- You can't reach any previous landlord after multiple attempts. That's not an accident.

What Can't You Ask Under Fair Housing Law?

The Fair Housing Act plus Florida's additional protections create a clear line between what you can screen for and what you cannot. Cross that line, and you're looking at a discrimination complaint — even if you didn't intend to discriminate.

Protected classes (federal + Florida):

- Race or color

- Religion

- National origin

- Sex (including sexual orientation and gender identity)

- Disability

- Familial status (children under 18, pregnant women)

Some Florida municipalities add protections. Miami-Dade covers age, marital status, and source of income. Hillsborough County has its own tenant protections. Know your local ordinances.

Questions you cannot ask — even casually:

- "Do you have kids?" or "How many children do you have?"

- "What country are you from?" or "Where's your accent from?"

- "Are you married?" or "Who will be living with you?" (you can ask how many occupants — not their relationships)

- "Do you have a disability?" or "Why do you need a first-floor unit?"

- "What church do you go to?"

- "How old are you?" (in jurisdictions with age protection)

The safe approach: establish written screening criteria before you receive any applications. Income requirement, credit score minimum, rental history standards, background check policy. Apply them identically to every applicant. Document everything.

How Do You Make the Decision?

You've got the credit report, background check, income docs, and landlord references. Now you're choosing between applicants — and this is where the documentation matters most.

Approve when the applicant meets all your published criteria. Don't add conditions you didn't advertise (like requiring a co-signer for a specific applicant but not others).

Deny when the applicant fails to meet your criteria. Under the FCRA, you must send an adverse action notice that tells the applicant:

- That they were denied

- The specific reason (credit score, insufficient income, negative rental history)

- The name of the screening company that provided the report

- Their right to obtain a free copy of the report within 60 days

Conditional approval (higher deposit, co-signer) is legal in Florida as long as the conditions are based on your screening criteria and applied consistently. Requiring a co-signer for one applicant with a 590 credit score and not for another with the same score is a fair housing problem.

Keep every application, every screening report, and every decision for at least 4 years. If a discrimination complaint surfaces, your documentation is your defense.

What Are the Biggest Screening Mistakes?

Relying on gut feeling. "They seemed like nice people" isn't a screening criterion. Nice people can have terrible credit and two prior evictions. Screen everyone the same way.

Skipping the second landlord. The current landlord has a motive to give a good reference — they want the tenant gone. Call the landlord before that one for a more honest picture.

Accepting incomplete applications. If an applicant leaves the previous landlord section blank or "can't remember" their employer's phone number, that's not forgetfulness. It's a red flag. Don't start processing incomplete applications.

Screening is the single most impactful step in rental property management. Get it right, and you avoid 80% of the problems landlords lose sleep over. Get it wrong, and you're looking at months of lost rent, property damage, and legal fees.

If you'd rather have an experienced team handle screening — including the background checks, income verification, and fair housing compliance — get a free rental analysis to see how professional management works for your property.