House Hacking in Florida: Live in One Unit, Rent the Rest

Buy a 2-4 unit property in Florida with FHA, live in one unit for a year, and let the rent cover most of your mortgage. How it works in Orlando and Tampa.

Buy a duplex. Live in one side. Rent the other. Your tenant's rent covers most of your mortgage, and you're building equity while you sleep. FHA lets you put down as little as 3.5% on a 2-4 unit property. you've to live there for at least a year. After that, you can move out, rent both units, and repeat.

Why House Hacking Works in Florida

Florida has no state income tax. Orlando and Tampa both have strong rental demand. Duplexes exist in suburbs like Brandon, Riverview, Lake Nona, and Avalon Park. FL landlords in Orlando and Tampa should check local requirements. Florida has no state income tax. Orlando and Tampa both have strong rental demand. Duplexes exist in suburbs like Brandon, Riverview, Lake Nona, and Avalon Park. Put 3.5% down on a $350,000 duplex and the other unit rents for $1,650? That rent can cover 70-80% of your mortgage.

What Are the FHA Requirements?

In Florida, Owner occupancy. You must live in one unit for at least a year. No exceptions. Property type. 2-4 units. Down payment. 3.5% of purchase price. On a $350,000 duplex, that's $12,250. Credit. Minimum 580 for 3.5% down. MIP. You'll pay mortgage insurance until you refinance or reach 20% equity. Where Do You Find

Owner occupancy. You must live in one unit for at least a year. No exceptions.

Property type. 2-4 units.

Down payment. 3.5% of purchase price. On a $350,000 duplex, that's $12,250.

Credit. Minimum 580 for 3.5% down.

MIP. You'll pay mortgage insurance until you refinance or reach 20% equity.

Where Do You Find Duplexes in Orlando and Tampa?

Orlando. Lake Nona, Avalon Park, Winter Park, and Dr. Phillips. Prices run $300,000-$450,000. Tampa. Brandon, Riverview, Seminole Heights, and South Tampa. $320,000-$400,000 for solid areas. Our first rental property guide covers how to evaluate locations. Real Numbers: Tampa Duplex Example In Florida, $360,00

Orlando. Lake Nona, Avalon Park, Winter Park, and Dr. Phillips. Prices run $300,000-$450,000.

Tampa. Brandon, Riverview, Seminole Heights, and South Tampa. $320,000-$400,000 for solid areas. Our first rental property guide covers how to evaluate locations.

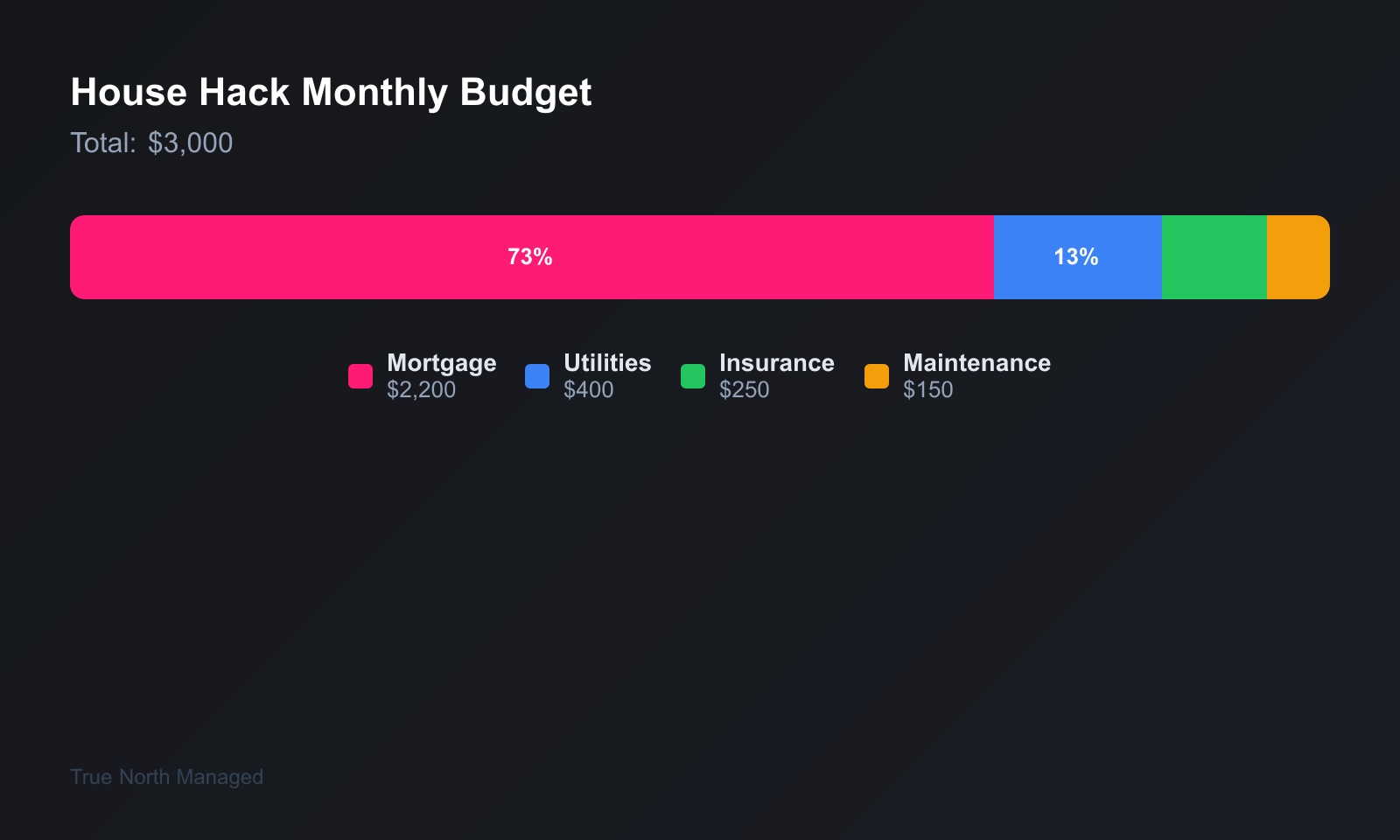

Real Numbers: Tampa Duplex Example

$360,000 duplex in Brandon. 3. 5% down = $12,600. FL landlords in Orlando and Tampa should check local requirements. $360,000 duplex in Brandon. 3.5% down = $12,600. Closing costs ~$10,000. Total cash ~$22,600. Unit 2 rents $1,600/month. Total PITI ~$2,876/month. Your out-of-pocket: $1,276/month for housing -- less than most Tampa apartments.

Screening Your First Tenant

You're living next door. In Florida, You want a good tenant. Follow tenant screening and fair housing rules from day one. FL landlords in Orlando and Tampa should check local requirements. You're living next door. You want a good tenant. Follow tenant screening and fair housing rules from day one.

3 House Hacking Mistakes to Avoid

1. Buying in a bad neighborhood to save money. You're living there. Choose somewhere you'd actually want to be. 2. Ignoring the numbers. If the rent from the other unit doesn't cover most of your mortgage, you're not really house hacking. 3. Skipping the lease. Get a proper lease, collect a security deposit, and follow FL 83.49.

Next Step: Run Your Numbers

House hacking only works if the numbers work. Our financing guide covers FHA and other options. A free rental analysis gives you market rent for Orlando or Tampa duplexes. FL landlords in Orlando and Tampa should check local requirements. House hacking only works if the numbers work. Our financing guide covers FHA and other options. A free rental analysis gives you market rent for Orlando or Tampa duplexes.

FHA and Owner-Occupancy Rules

FHA loans require you to live in the property for at least one year. In Florida, That means your primary residence must be one of the units. After a year, you can move and rent it out—or refinance to conventional and repeat. FHA loans require you to live in the property for at least one year. That means your primary residence must be one of the units. After a year, you can move and rent it out—or refinance to conventional and repeat. VA loans have similar owner-occupancy requirements. The HUD website has the full FHA guidelines.

Tax Implications

When you live in one unit and rent others, you split expenses. In Florida, The rental portion goes on Schedule E. The personal portion isn't deductible. FL landlords in Orlando and Tampa should check local requirements. When you live in one unit and rent others, you split expenses. The rental portion goes on Schedule E. The personal portion isn't deductible. If you sell, you may qualify for the capital gains exclusion on your unit ($250k single, $500k married) but not on the rented units. See our tax deductions checklist for details.

Florida House-Hack Markets

Orlando and Tampa have duplex and small multi inventory. Look near job centers: Medical City, UCF, MacDill, downtown cores. House hacking works best where rents support the mortgage. FL landlords in Orlando and Tampa should check local requirements. Orlando and Tampa have duplex and small multi inventory. Look near job centers: Medical City, UCF, MacDill, downtown cores. House hacking works best where rents support the mortgage. Run the deal analysis before you buy. For Orlando and Tampa market context, see our hubs. Bottom line: FHA and VA require one year of owner occupancy. Live in one unit, rent the rest. Split expenses for taxes. After a year, you can move and rent your unit or refinance. Orlando and Tampa have duplex and small multi inventory near job centers. Run the deal analysis first. Screen tenants for the other units as carefully as you would for a standalone rental. You're sharing walls and common areas. A bad tenant next door makes your life miserable. The same screening criteria apply—income, credit, references. Your home is still an investment. Screen your neighbors as much as your tenants. You're living there. A noisy or difficult tenant in the other unit affects your quality of life. Use the same criteria you would for a standalone rental. Income, credit, references. Don't relax standards because you're owner-occupying.

Common House-Hack Mistakes

Relaxing screening for the other units because you're owner-occupying. Screen tenants the same way you would for a standalone rental. Not splitting expenses correctly for taxes -- the rental portion goes on Schedule E; the personal portion doesn't. Relaxing screening for the other units because you're owner-occupying. Screen tenants the same way you would for a standalone rental. Not splitting expenses correctly for taxes -- the rental portion goes on Schedule E; the personal portion doesn't. Assuming FHA allows immediate rental of all units. You must live in one unit for at least one year. And not budgeting for the other units' vacancy. You still pay the full mortgage if a unit is empty. Our deal analysis guide and financing guide cover the math. Orlando and Tampa hubs have market context.

What to Watch

FHA and conventional loans have different rules for owner-occupancy. In Florida, If you're using an owner-occupied loan, you typically need to live in the property for at least a year. Moving out sooner can trigger issues with your lender. FHA and conventional loans have different rules for owner-occupancy. If you're using an owner-occupied loan, you typically need to live in the property for at least a year. Moving out sooner can trigger issues with your lender.

Common Mistakes to Avoid

One of the biggest mistakes we see: skipping the written notice. Florida law is strict about documentation. If you don't have a paper trail—or email trail that meets SB 716's requirements—you can lose an eviction or deposit dispute. Document everything. Another mistake: underbudgeting for turnover. A typical Florida turnover runs $1,500–$3,000 when you include paint,

One of the biggest mistakes we see: skipping the written notice. Florida law is strict about documentation. If you don't have a paper trail—or email trail that meets SB 716's requirements—you can lose an eviction or deposit dispute. Document everything.

Another mistake: underbudgeting for turnover. A typical Florida turnover runs $1,500–$3,000 when you include paint, carpet, cleaning, and minor repairs. If you're only setting aside 5% of rent for maintenance, you're short. Plan for 8–12% in year one until you know your property.

Third: treating every tenant the same. A military family near MacDill has different needs than a UCF grad student. Screen for fit, not just credit score. The right tenant in the right property stays longer and costs you less.

Florida-Specific Considerations

Florida Statute 83 applies to residential tenancies. Know the notice requirements: 3 days for non-payment (soon 5 under SB 716), 7 days for cure or vacate for lease violations, 15 days for month-to-month termination. Wrong notice = delayed eviction.

Insurance is another Florida reality. Wind and flood can double your premium in certain zones. Run quotes before you buy. A $200/month insurance difference changes your cash flow by $2,400/year.

Finally, property taxes. Homestead doesn't apply to rentals. You'll pay non-homestead rates. In Florida County, that's typically 1.2–1.5% of assessed value. Appeal if your assessment seems high—many landlords overpay.

When to Get Help

If you're out of state, hire a local property manager. The 8–10% fee pays for itself in faster leasing, better screening, and someone who can show up when the AC dies at 10 PM. Self-managing from another state is a recipe for deferred maintenance and tenant frustration.

For legal issues—evictions, deposit disputes, lease breaks—consult a Florida-licensed attorney. Landlord-tenant law has traps. A $500 consult can save you $5,000 in a botched eviction. We've seen it.

Finally, for complex financial decisions—1031 exchanges, LLC structuring, depreciation—talk to a CPA who works with rental owners. The tax code rewards those who plan. Don't wing it.

When to Get Help

If you're out of state, hire a local property manager. The 8–10% fee pays for itself in faster leasing, better screening, and someone who can show up when the AC dies at 10 PM. Self-managing from another state is a recipe for deferred maintenance and tenant frustration.

For legal issues—evictions, deposit disputes, lease breaks—consult a Florida-licensed attorney. Landlord-tenant law has traps. A $500 consult can save you $5,000 in a botched eviction. We've seen it.

Finally, for complex financial decisions—1031 exchanges, LLC structuring, depreciation—talk to a CPA who works with rental owners. The tax code rewards those who plan. Don't wing it.

HOAs can restrict or ban house hacking in some communities. Check the covenants before you buy. Some allow it; others don't.