Q3 2025 Market Pulse: Orlando vs. Tampa Rental Comparison

Quarterly comparison of Orlando and Tampa rental markets. Summer rental season results, vacancy trends, rent growth, and investor activity.

Summer is the peak rental season in Central Florida. Families move before school starts. Tourism drives short-term demand. By Q3, the numbers tell you how the year is shaping up. Here's how Orlando and Tampa stacked up in the third quarter of 2025.

Summer Rental Season Results

Both markets typically see strong leasing activity in July and August.Rents tend to hold or climb through the season as demand peaks. This year, Orlando's tourism and theme park employment continued to support a steady renter pool.

Both markets typically see strong leasing activity in July and August. Rents tend to hold or climb through the season as demand peaks. This year, Orlando's tourism and theme parkemploymentcontinued to support a steady renter pool. Tampa's mix of military, healthcare, and finance kept demand solid. New construction in both metros added supply, but population growth absorbed much of it. Landlords who priced correctly and marketed well generally saw shorter vacancy periods.

Vacancy and Absorption

Vacancy rates in both markets remained tight relative to historical norms.Orlando's inland position and diverse economy have historically insulated it from some of the volatility seen in coastal Florida. Tampa's growth corridors, including Wesley Chapel and Riverview, continued to attract renters.

Vacancy rates inboth marketsremained tight relative to historical norms. Orlando's inland position and diverse economy have historically insulated it from some of the volatility seen in coastal Florida. Tampa's growth corridors, including Wesley Chapel and Riverview, continued to attract renters. Absorption of new units varied by submarket. Well-located properties in established neighborhoods tended to lease faster than peripheral new builds.

Rent Growth Comparison

Rent growth in Central Florida has moderated from the peaks of earlier years, but.Orlando's Lake Nona, Dr. Phillips, and Winter Park areas maintained premium positioning. FL landlords in Orlando and Tampa should check local requirements.

Rent growth in Central Florida has moderated from the peaks of earlier years, but both Orlando and Tampa continued to see upward pressure in strong submarkets. Orlando's Lake Nona, Dr. Phillips, and Winter Park areas maintained premium positioning. Tampa's South Tampa, Westchase, and Seminole Heights drew steady interest. Landlords who renewed leases in Q3 often achieved modest increases. The gap between asking and achieved rents narrowed as markets normalized.

New Construction Impact

New multifamily and single-family rental supply entered both markets.Orlando's development pipeline remained active, particularly along the I-4 corridor and in suburban growth areas. Tampa saw similar activity in Pasco and Hillsborough. FL landlords in Orlando and Tampa should check local requirements.

New multifamily and single-family rental supply entered both markets. Orlando's development pipeline remained active, particularly along the I-4 corridor and in suburban growth areas. Tampa saw similar activity in Pasco and Hillsborough. For existing landlords, the impact depended on location. Properties in established neighborhoods with limited new supply faced less competition. Those in high-growth corridors had to sharpen pricing and presentation.

Investor Activity

Investor interest in both markets stayed strong.Florida's no state income tax, population growth, and landlord-friendly laws continued to attract out-of-state buyers. Orlando and Tampa both offered a range of entry points: from core urban to suburban.

Investor interest in both markets stayed strong. Florida's no state income tax, population growth, and landlord-friendly laws continued to attract out-of-state buyers. Orlando and Tampa both offered a range of entry points: from core urban to suburban. Cap rates and cash-on-cash returns varied by submarket. Due diligence on insurance, taxes, and HOA costs remained critical as operating expenses have risen.

For a deeper look at each market, see ourOrlando property management guideandTampa property management guide. If you're evaluating a rental in either market,get a free rental analysisand we can walk through the numbers for your property.

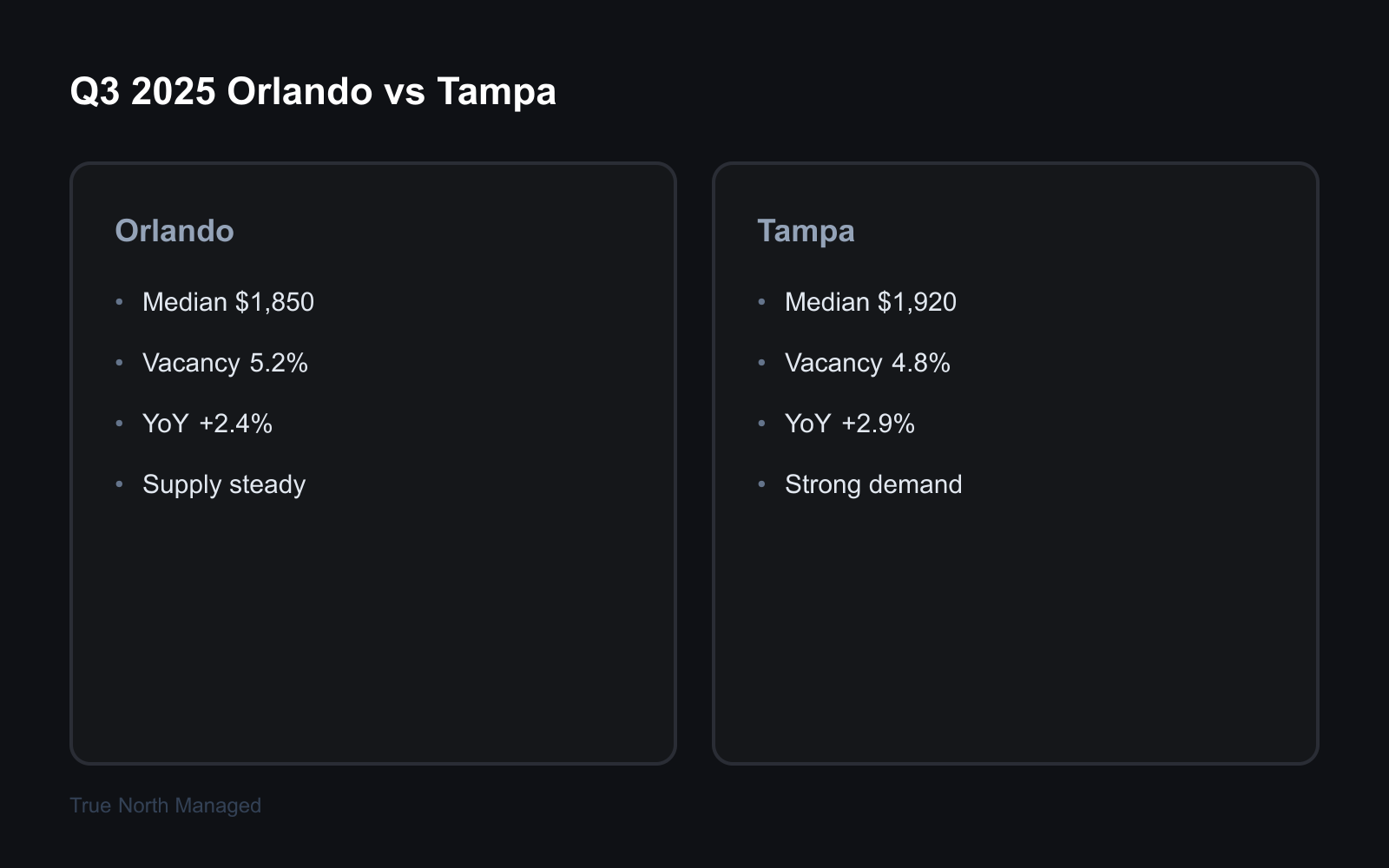

Rent and Vacancy Comparison

Orlando and Tampa both saw rent growth in Q3 2025, with Orlando's median rent slightly higher in core submarkets.Vacancy rates remained tight in both markets, though Tampa's suburban corridors had more availability. The gap between urban and suburban rents widened in Orlando, while Tampa's South Tampa -- and Westchase areas held premium pricing.

Orlando and Tampa both saw rent growth in Q3 2025, with Orlando's median rent slightly higher in core submarkets. Vacancy rates remained tight in both markets, though Tampa's suburban corridors had more availability. The gap between urban and suburban rents widened in Orlando, while Tampa's South Tampa -- and Westchase areas held premium pricing.

Supply and Demand

New multifamily deliveries added inventory in both markets.Orlando's Lake Nona and Horizon West absorbed new supply quickly. Tampa's Wesley Chapel and New Tampa saw similar absorption. FL landlords in Orlando and Tampa should check local requirements.

New multifamily deliveries added inventory in both markets. Orlando's Lake Nona and Horizon West absorbed new supply quickly. Tampa's Wesley Chapel and New Tampa saw similar absorption. Landlords in established submarkets faced less new competition than those in growth corridors. See ourOrlando market hubandTampa market hubfor neighborhood-level data.

Landlord Takeaways

Pricing held in both markets.Vacancy remained manageable. The main risk was overbuilding in specific submarkets. FL landlords in Orlando and Tampa should check local requirements.

Pricing held in both markets. Vacancy remained manageable. The main risk was overbuilding in specific submarkets. Focus on properties with strong employment and school access. OurOrlando vs Tampa investment comparisonprovides a longer-term view.

What to watch: Both markets were strong through Q3. The usual seasonal patterns -- Orlando's tourism-driven demand and Tampa's military and relocation cycles -- held. Keep an eye on new construction and how it affects vacancy in each submarket.

Verified data (March 2026):

- Orlando median: ~$1,977 | Tampa: ~$2,100

- Orlando vacancy: 6.2% | Tampa: 6.5%

- Orlando YoY: -4% | Tampa: -5%

Sources: Realtor.com rent reports, Florida Landlord Dec 2025 report