Q4 2025 Market Pulse: Orlando vs. Tampa Year-End Check

Year-end 2025 market comparison: holiday slowdown, snowbird demand, new construction, and how Orlando and Tampa diverged in the fourth quarter.

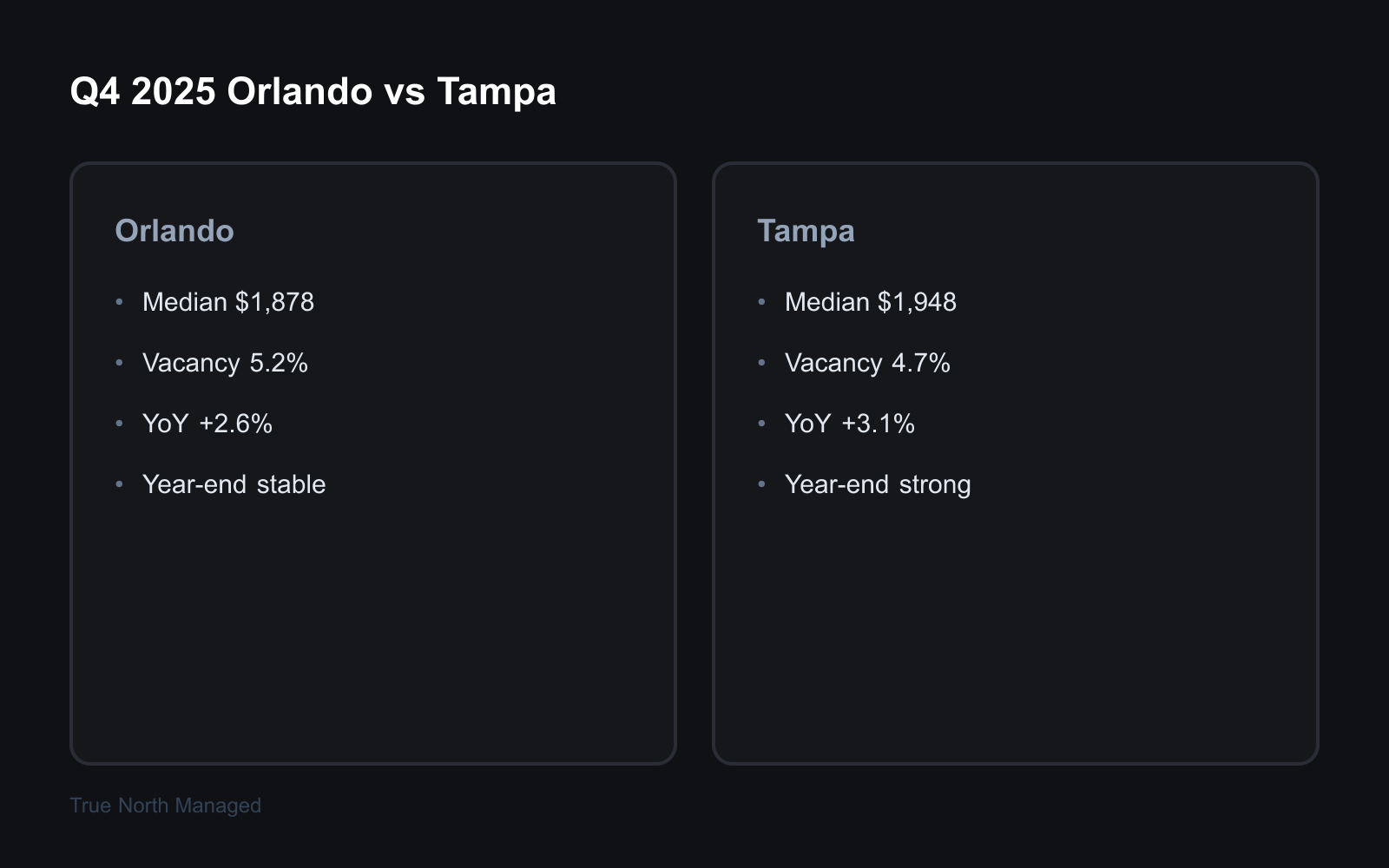

Q4 2025 brought the usual year-end dynamics to Central Florida — a holiday move-in slowdown, snowbird season in full swing, and new construction deliveries wrapping up. Orlando and Tampa both saw demand hold, but the drivers diverged: Orlando is inland and tourism-driven, Tampa is coastal and shaped more by military and medical employment. Here's how the two markets compared at year-end.

How did the holiday season affect Q4 rentals?

Both Orlando and Tampa see move-in volume dip from late November through December as families and corporate relocations pause for the holidays. That dip is a timing effect, not weak demand — vacancy rates that tick up in Q4 reflect the calendar, not a soft market.

The lull doesn't last. By January, both markets reset as new leases start and snowbird demand peaks. Landlords carrying a vacancy into Thanksgiving often had to wait until January for the next wave of serious applicants. Correctly priced properties kept drawing interest through the slow weeks; overpriced units simply sat.

What happened with year-end lease renewals?

Many Florida leases run on a calendar-year cycle or expire in late fall, so Q4 is when landlords and tenants make the renewal call — raise rent, hold steady, or part ways. In both Orlando and Tampa, conditions favored modest increases.

Vacancy stayed low enough that landlords had leverage at the renewal table. Tenants who had been sitting under market often saw renewal offers at or above prior-year levels. Our Q3 2025 Market Pulse showed rents trending up, and Q4 reinforced the pattern — landlords who deferred increases earlier in the year had room to adjust at renewal.

How did snowbird season shape Q4 demand?

Northern retirees and seasonal residents arrive in Florida in late October and November, and Q4 is when that demand lands. Tampa carries the heavier snowbird concentration — South Tampa, St. Petersburg, and beach-adjacent areas — while Orlando draws its share in 55+ communities and amenity-rich neighborhoods.

Demand for furnished and short-term winter leases picked up in both markets. Winter-term leases often command a premium over standard 12-month rates, which is real upside — but the tradeoff is the turnover when snowbirds leave in spring. Landlords pricing a seasonal lease should weigh the premium against an earlier vacancy.

How did new construction affect the Q4 market?

Central Florida's multifamily and single-family rental pipeline stayed active through the fourth quarter. Orlando saw deliveries in Lake Nona, Horizon West, and along the I-4 corridor; Tampa added inventory in Riverview, Wesley Chapel, and New Tampa.

Absorption kept pace in most submarkets, so the new supply didn't broadly soften rents. But landlords with older inventory faced sharper competition from newer units with modern finishes. Well-located properties held their pricing; the pressure showed up in pockets with concentrated new supply, where an older unit had to compete on price or condition.

What happened with Florida's insurance market in Q4?

Florida's property insurance market had been volatile for several years, and by late 2025 some stability had returned. Not every landlord saw relief, but the pace of premium increases had slowed in many cases — a meaningful shift after years of steep jumps.

Flood and windstorm remain separate concerns, especially in Tampa Bay, where flood-zone designations drive policy costs. For investors running the numbers on a 2026 acquisition or refinance, the insurance trajectory is a key input, and Q4 offered a window to reassess coverage and budgets before the new year.

How did Orlando and Tampa diverge in Q4 2025?

The two markets grew on different engines. Orlando's rental demand runs on tourism, the theme parks, UCF, and a widening tech corridor. Tampa's demand comes from the military presence at MacDill Air Force Base, healthcare employers like Tampa General and BayCare, and a growing finance sector. Both metros kept adding population and jobs through Q4.

The difference is the mix. Orlando carries more seasonal and tourism-adjacent demand, which means more Q4 holiday swing. Tampa leans on year-round professional and military demand, which is steadier through the calendar. Neither market is better in the abstract — the right one depends on your strategy and your target tenant.

What does Q4 2025 mean for your 2026 strategy?

If you're setting rent levels or weighing a lease renewal, the Q4 2025 data points the same way for both markets: conditions stayed landlord-favorable into year-end. Low vacancy, steady demand, and modest rent growth gave landlords room to push renewals up.

For a deeper look at either metro, see our Orlando and Tampa market hub pages. For a data-driven read on what your specific property could command going into 2026, get a free rental analysis — we pull comps across both markets and help you position for the year ahead.

• Orlando median rent, December 2025: ~$1,950 | Tampa: ~$2,100

• Florida statewide rental vacancy: 6.9%

• 2019–2023: Florida added roughly 240,000 multifamily units; median rent rose 39% ($1,238 → $1,719)

Sources: Florida Landlord, December 2025 report; Florida Realtors rental crunch report.