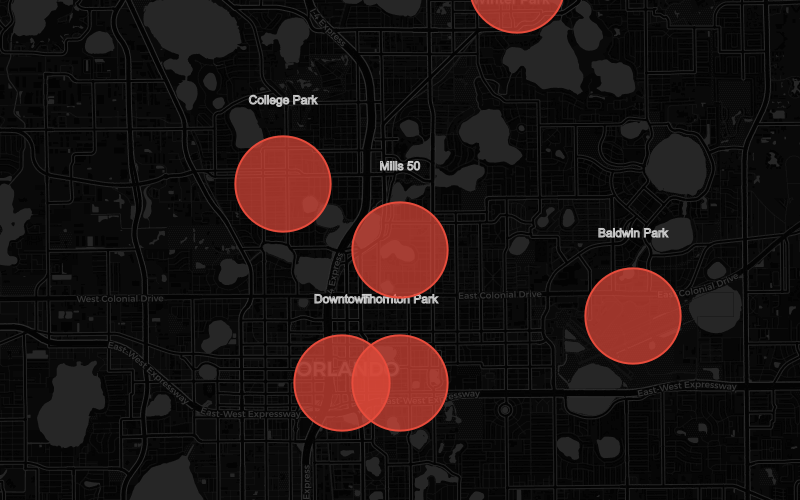

Central Orlando Snapshot

Investment snapshot: Central Orlando

| Entry price range | $300K–$800K |

| Median rent (3BR) | $2,600–$3,300 |

| Cap rate range | 2–5% |

| Gross yield range | 4–7% |

Central Orlando is an appreciation play, not a cash-flow market. Investors here buy for long-term equity growth, low vacancy, and premium tenant quality. The corridor commands the highest rents in the metro, but entry prices reflect that premium. Downtown condos offer the most accessible entry ($300K–$400K) with the highest cap rates (3–5%), while Winter Park and Baldwin Park require more capital but attract the most stable tenants.

Central Orlando is the metro's urban core — the corridor stretching from Winter Park south through College Park and Baldwin Park to the Lake Eola / Thornton Park district and Downtown's high-rises. Over 60% of housing in this corridor is renter-occupied, well above the national average, and the tenant pool skews professional: young professionals, dual-income couples, medical workers, and empty-nesters drawn to walkable neighborhoods with restaurants and cultural amenities.

Walk Scores range from 44 (Winter Park overall) to 96 (Downtown), and that walkability drives measurable rent premiums of 15–20% compared to suburban Orlando. Entry prices are the highest in the metro ($350K–$800K depending on neighborhood), making this an appreciation play rather than a cash-flow market. Cap rates run 3–5%, but vacancy stays below 5% and 5-year appreciation has averaged 5–8% annually.

The construction pipeline is concentrated in Downtown, where 500+ new apartments will deliver in 2026–2027. Winter Park, College Park, Baldwin Park, and Thornton Park face minimal new supply — their rents are insulated from the Downtown cycle. If your investment thesis is long-term equity growth with high tenant quality and low turnover, Central Orlando delivers.

What to know before investing in Central Orlando

- New supply concentrated in Downtown. Creative Village and Baldwin East deliver 800+ apartments in 2026–2027. Winter Park, College Park, and Thornton Park face minimal new supply—their rents are insulated.

- Historic district restrictions. Winter Park and College Park have historic overlay districts. Exterior renovations require board approval—factor compliance delays into rehab timelines.

- STR rules limit competition. City of Orlando prohibits entire-home short-term rentals in most single-family zones, protecting long-term rental demand.

- Higher entry costs than metro average. Median home prices run $350K–$800K, well above Orlando metro’s ~$392K.

- Condo product requires extra due diligence. Downtown and Baldwin Park have significant condo inventory with HOA fees ($400–$600/month), rental caps, and special assessment risk.

Neighborhoods

Key neighborhoods driving rental returns in the Central Orlando core.

Winter Park

Park Avenue premium, Rollins College, $2,675/mo median rent

Park Avenue · Rollins College · SunRailCollege Park

Historic bungalows, restaurant corridor, $3,100/mo median rent

Edgewater Dr · Historic homes · WalkableDowntown Orlando

Urban core, high-rise condos, 3–5% cap rates

Lake Eola · High-rise · Urban livingThornton Park

Walkable dining district, limited inventory, $2,600/mo median

Eola district · Brick streets · Boutique diningBaldwin Park

Master-planned, highest walkability, $3,300/mo median rent

Village center · Planned community · Parks